A World on Borrowed Time

America — like much of the world — is drowning in debt just as rising rates, stagflation, and AI job losses hit the economy all at once.

The Week That It Was…

The third week of Q2’s second month delivered another “calm” stretches for macro investors, with markets focusing on the latest FOMC minutes, Flash PMI data, China retail sales, and Japan CPI. Meanwhile, with only 18 S&P 500 companies reporting earnings, investor attention remained heavily concentrated on Home Depot, Walmart, and especially NVIDIA, whose results once again carried much of the market’s AI-driven optimism.

Freshly returned from his diplomatic excursion to the Middle Kingdom, Donald Copperfield immediately resumed his favourite form of international relations: Truth Social megaphone diplomacy. Barely hours later, he was already warning that the clock is ticking for Season 2 of the war that was never officially called a war and was supposedly “totally won” sometime around hour one of day one. Nothing says lasting peace quite like announcing the sequel before the credits of the first episode have even finished rolling.

The great American “blockade of the blockade” is starting to look remarkably selective, as ships continue crossing the Strait of Hormuz after politely coordinating with Iranian authorities, paying generous bitcoin “navigation fees,” and then requesting permission from the U.S. blockade further offshore — because nothing says “rules-based order” quite like two competing toll booths in the same waterway. While Viceroy Rubio warned that Iran’s shipping toll system is “unacceptable,” Tehran appears to be proving that in modern geopolitics, whoever controls the chokepoint eventually discovers the ancient and highly profitable art of monetizing panic.

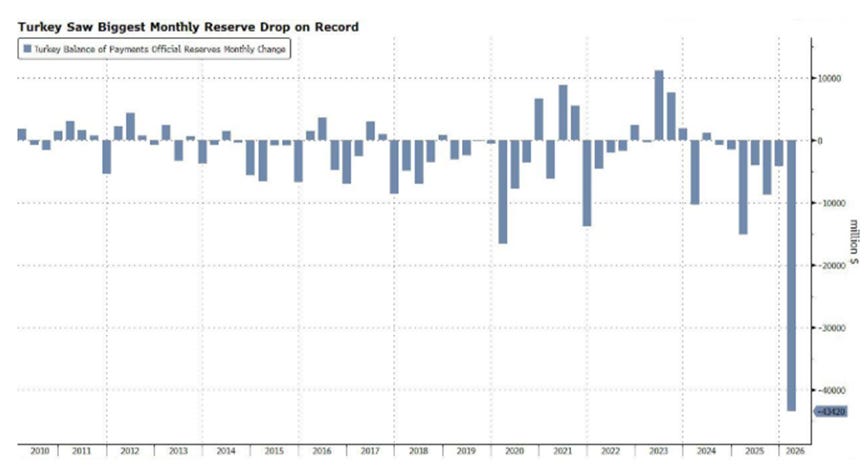

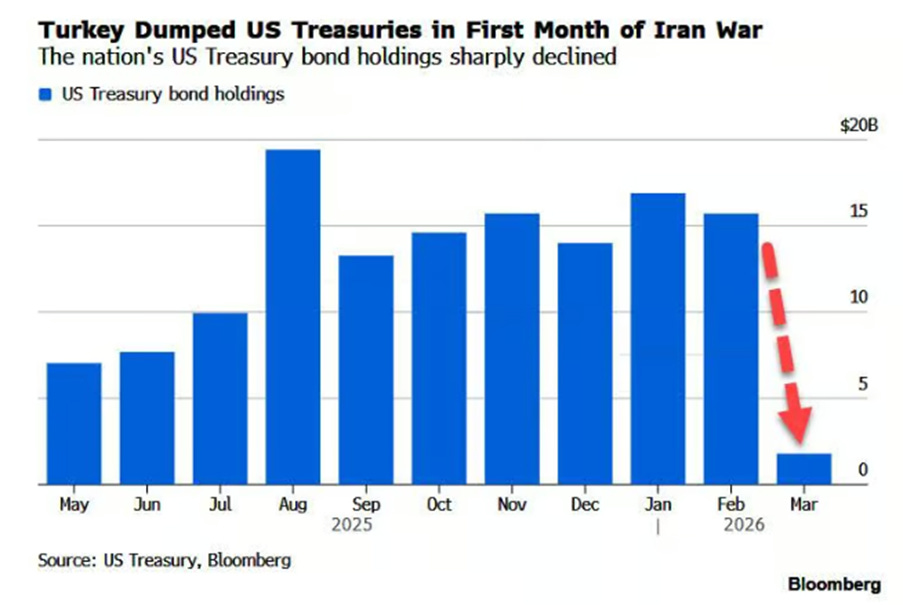

After aggressively dumping gold at the start of the great Middle East “stabilization mission,” Turkey eventually discovered that defending a collapsing currency requires sacrificing whatever remains liquid — including U.S. Treasuries. As the Iran conflict triggered another classic emerging-market liquidation spree, Turkey’s foreign reserves suffered their largest monthly collapse on record in March, falling by $43.4 billion while the current-account deficit widened sharply under the weight of soaring commodity prices. Apparently, in modern central banking, “reserve management” increasingly means deciding which asset to sell first before the next crisis arrives.

Turkey’s economic “stabilization strategy” is now looking increasingly similar to a garage sale of national reserves. Hammered by soaring oil prices following the effective closure of the Strait of Hormuz, Ankara first dumped gold, then quietly liquidated nearly all of its U.S. Treasury holdings — collapsing from $16 billion to just $1.8 billion in a single month — in a desperate attempt to slow the lira’s decline. Despite aggressive interventions, inflation continues accelerating, bond yields are exploding, and the lira keeps sinking, proving once again that defending a currency with dwindling reserves is a bit like trying to stop a flood by selling the furniture.

In another reminder that the Empire of Washington increasingly resembles a competing theocracy wrapped in Wall Street branding, officials are now openly calling for leaders and citizens alike to “get on their knees before the Supreme Lord.” Apparently, the difference between modern geopolitics and medieval theology is mostly just better public relations and more expensive military contractors.

After spending months being quietly transformed from Director of National Intelligence into Director of “Do Not Invite,” Tulsi officially resigned under the noble banner of caring for her husband’s illness — conveniently ending one of Washington’s more awkward relationships between an anti-war intelligence chief and an administration enthusiastically expanding military operations from Iran to Venezuela. While the White House praised her “incredible job,” Tulsi increasingly found herself excluded from key decisions, gently reminded that questioning permanent war strategies in modern Washington is roughly as career friendly as criticizing inflation statistics at the Federal Reserve.

While once again warning the world that Season 2 of the “Epic F**k Up” could begin at any moment, Donald Copperfield met with Syria’s newly repackaged leadership — yesterday’s battlefield revolutionary now rebranded as a statesman in a tailored Hugo Boss suit. In a region where the rule of law has historically been about as common as ice cubes in the Sahara, Washington apparently concluded that the best path toward influence was not stability, institutions, or reconstruction, but the timeless diplomatic strategy of branding, optics, and perhaps a light spray of “Trump Victory” cologne over the geopolitical rubble.

In the Caribbean, the Cuban crisis is quietly evolving from a regional dispute into another glorious chapter of the global “rules-based order,” where every major power now politely conducts geopolitical brinkmanship directly in each other’s backyard. Moscow is once again backing Havana, Washington is rediscovering its deep spiritual attachment to sanctions and regime pressure, and everyone is suddenly shocked that Russia might enjoy placing strategic assets near Florida after NATO spent decades expanding toward Russia’s borders. Meanwhile, Cuba itself remains trapped between blackouts, shortages, and economic collapse while global powers transform the island into another chessboard square in the accelerating 2026–2027 war cycle — proving once again that in the modern age, “de-escalation” has become little more than an archived diplomatic tradition.

https://www.bbc.com/news/articles/clype0x7pkgo

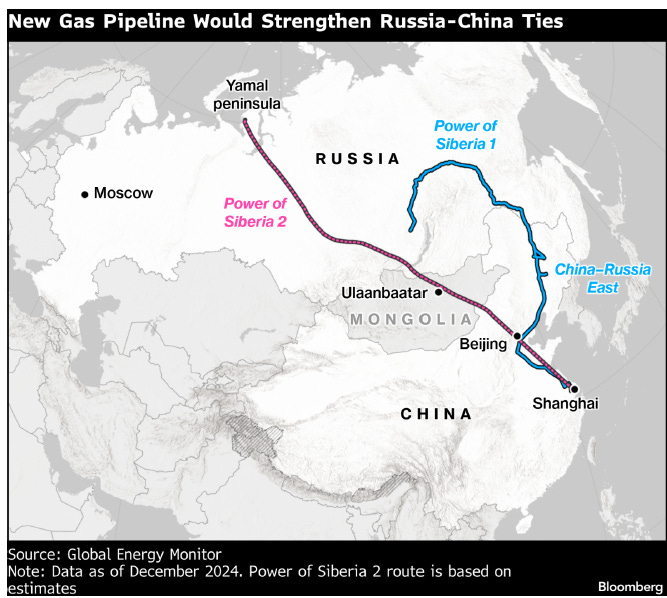

As Confucius almost certainly never said, “When the Eagle visits the Dragon, the Bear soon arrives for tea.” Less than a week after Donald Copperfield’s grand diplomatic pilgrimage to Beijing, Tsar Vladimir arrived to reaffirm the ever-deepening friendship between Moscow and the Middle Kingdom, with both leaders once again promoting their vision of a “multipolar world” — loosely translated as “less Washington, more us.” Xi and Putin signed dozens of agreements covering trade, technology, and strategic cooperation while politely reminding the world that sanctions, wars, and global instability have become excellent networking opportunities. Meanwhile, the long-discussed Power of Siberia 2 pipeline remained mysteriously absent from official remarks, proving that in geopolitics, as in ancient philosophy, the most important subject is often the one nobody mentions out loud.

.

“When the Strait closes, the pipeline suddenly becomes negotiable.” Russia is now quietly hoping that chaos in Middle East energy markets and the effective closure of the Strait of Hormuz will make Beijing more flexible on the long-delayed Power of Siberia 2 gas deal. While Xi and Putin continue celebrating their “multipolar friendship,” the reality is that Moscow increasingly depends on China for everything from trade to sanctioned technology imports, while Beijing carefully balances supporting Russia without becoming too visibly attached to the Ukraine war. In ancient strategic wisdom, this is known as “standing close enough to the Bear to benefit from the hunt, but not close enough to get covered in blood.”

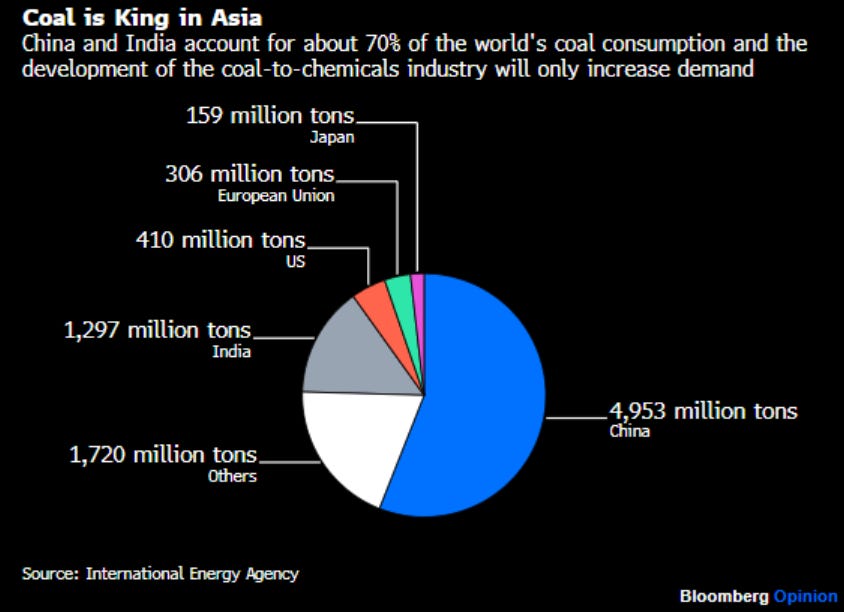

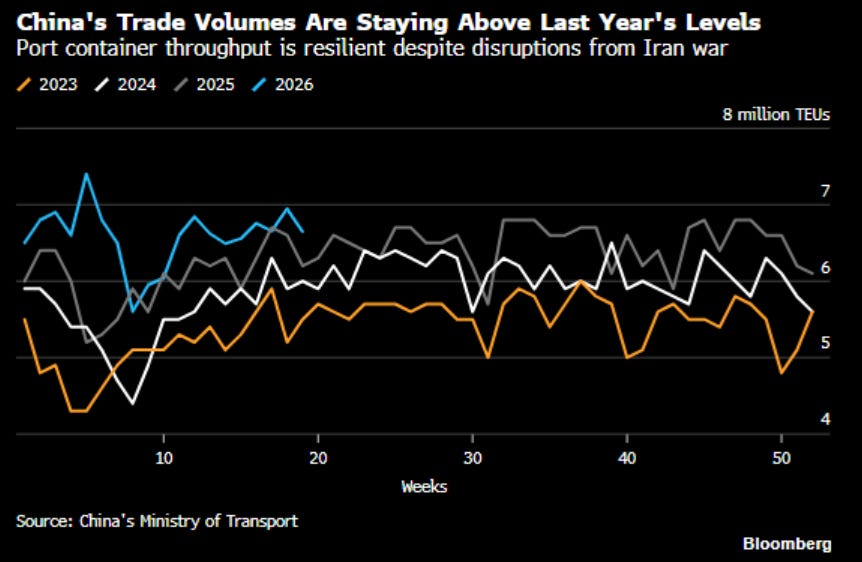

The reality is that “When the Strait closes, the coal shovel becomes strategic.” The shutdown of the Strait of Hormuz has thrown Asia’s chemical industry into chaos as fertilizer and plastics plants struggle without Middle Eastern oil and gas — everywhere except China, which quietly built a parallel coal-based chemical empire while the rest of the world was busy writing climate pledges. Now India and others want to copy Beijing’s coal-to-chemicals model, proving once again that when energy security collides with green ideology, governments suddenly rediscover their deep philosophical love for coal.

India is now trying to replicate China’s coal-to-chemicals strategy to strengthen energy, food, and economic security as the Hormuz shock exposes the dangers of relying on imported oil and gas. The logic is simple: domestic coal means fewer energy imports, lower pressure on foreign reserves, and millions of jobs preserved. The problem is that India lacks both China’s advanced coal-conversion technology and its decades of industrial knowhow — proving once again that copying the Middle Kingdom is easier said than synthesized. Ironically, the very crisis meant to accelerate the green transition may end up extending the life of coal for another generation, just as the oil shocks of the 1970s once did.

In another inspiring demonstration that the Empire remains fully stable and absolutely not devouring itself from within, the United States Department of Justice unveiled a perfectly symbolic $1.776 billion “Anti-Weaponization Fund” to compensate alleged victims of political “lawfare.” The number, of course, is entirely coincidental — much like all government symbolism in late-stage republics. More importantly, the announcement quietly acknowledges what officials spent years denying: the growing perception that the justice system itself has become politicized. History tends to treat this phase poorly. Once institutions are viewed as partisan weapons rather than neutral arbiters, political retaliation becomes normalized, public trust deteriorates, and every election starts resembling a hostile corporate takeover with better flags and worse accounting. Meanwhile, taxpayers are once again invited to finance the entire spectacle, reassured that adding another multi-billion-dollar program to an already unpayable debt pile is simply the price of defending democracy, stability, and whatever the slogan happens to be this quarter.

In another spectacular victory for sanctions policy, North Korea reportedly earned nearly $14 billion from the Ukraine war — roughly half the size of its entire economy. While the West keeps insisting the conflict is “weakening” its adversaries, Russia, Iran, China, and North Korea have instead turned Ukraine into the world’s most expensive military training program. Pyongyang didn’t join the war out of ideology; it joined because NATO accidentally created the greatest business and battlefield modernization opportunity North Korea has seen since the Cold War. While Europe was busy dismantling its industrial base in pursuit of climate virtue, North Korea was cashing artillery checks and learning drone warfare, electronic warfare, AI-assisted targeting, and modern battlefield tactics in real time. The irony is remarkable: the war designed to isolate America’s adversaries may ultimately end up training and hardening them instead.

https://www.pravda.com.ua/eng/news/2026/05/11/8034153/

In another heartwarming effort to build the digital gulag “for public safety and efficiency,” Britain’s NHS is reportedly giving Palantir contractors broad access to identifiable patient records through its new data platform. Citizens are once again being reassured that this is only about “improving healthcare” — much like mass surveillance was supposedly only about stopping terrorists before quietly expanding to monitor everyone with a smartphone and a bank account. After all, nothing says freedom quite like intelligence-linked contractors potentially accessing your medical history, prescriptions, psychological records, and personal data inside one giant centralized database. In modern Orwellian governance, privacy is apparently just another inefficient legacy system waiting to be optimized.

https://www.digitalhealth.net/2026/05/palantir-to-be-granted-unlimited-access-to-nhs-patient-data/

What Britain is building is no longer healthcare reform — it is surveillance wrapped in the comforting language of efficiency. Governments throughout history always promised that surrendering privacy was necessary for safety, stability, or the public good, right before quietly expanding control over everything else. From Roman census records to the Stasi’s personal files and Soviet internal passports, every empire eventually discovers the same truth: centralized data is power, and no government voluntarily gives power back once it has tasted it.

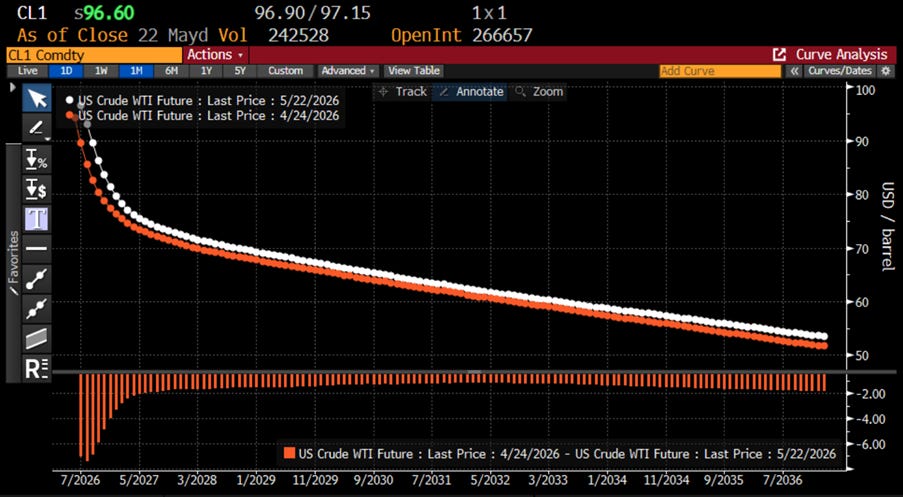

While oil shortages are increasingly becoming a question of “when” rather than “if,” the oil curve has continued its impressive ascent, with year-end crude expectations rising roughly $12 over the past month. Apparently, markets have finally discovered that geopolitical disruptions, strained supply chains, and shrinking inventories may not be the ideal ingredients for “transitory” inflation after all.

WTI Curve Live (while line); 1-month ago (orange line)

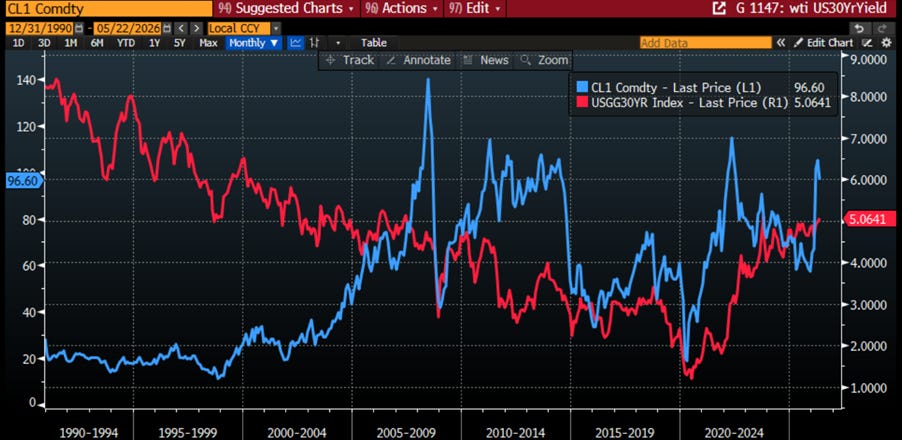

U.S. Treasury yields surged higher as markets suddenly remembered that disrupting traffic through the Strait of Hormuz might have consequences for inflation, energy prices, and debt markets. The resulting selloff pushed the 30-year Treasury yield to its highest level since 2007, as investors slowly came to terms with the radical possibility that endless deficits, geopolitical chaos, and structurally higher inflation may not be entirely “well anchored” after all.

WTI Price (blue line); US 30-Year Yield (red line).

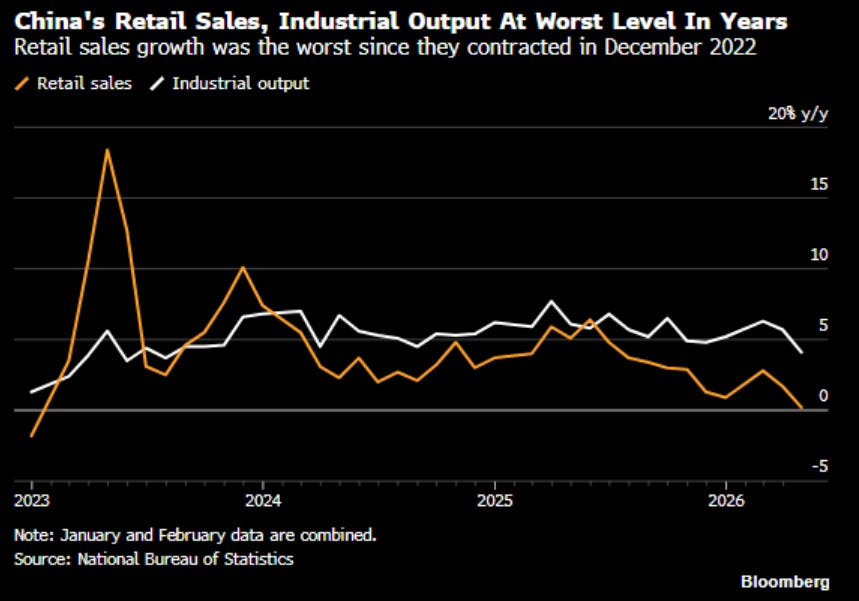

As another glorious side effect of the holy wars in the Middle East, the Middle Kingdom’s economy slowed sharply in April, with retail sales barely growing, industrial production missing expectations, and investment quietly slipping back into contraction. Apparently, AI-fuelled exports and semiconductor euphoria are no longer enough to hide the tiny inconvenience of collapsing domestic demand and soaring energy costs. Beijing still insists the economy is “stabilizing and improving” — which in modern central bank dialect roughly translates to: “please stop looking at the actual data.”

The economic activity was weaker than expected in April,” politely admitted economists, in what may be the financial equivalent of saying the Titanic experienced “minor navigation challenges. Exports still surged thanks to the global AI frenzy and improving trade ties with the U.S. following Donald Copperfield’s latest diplomatic tour of the Middle Kingdom, but even booming semiconductor shipments are no longer enough to fully offset collapsing domestic demand. Meanwhile, household loans slumped, consumer confidence remained stuck in a post-Covid coma, and youth unemployment quietly climbed to its highest level in more than two years — proving that even in the age of artificial intelligence, someone still has to buy things.

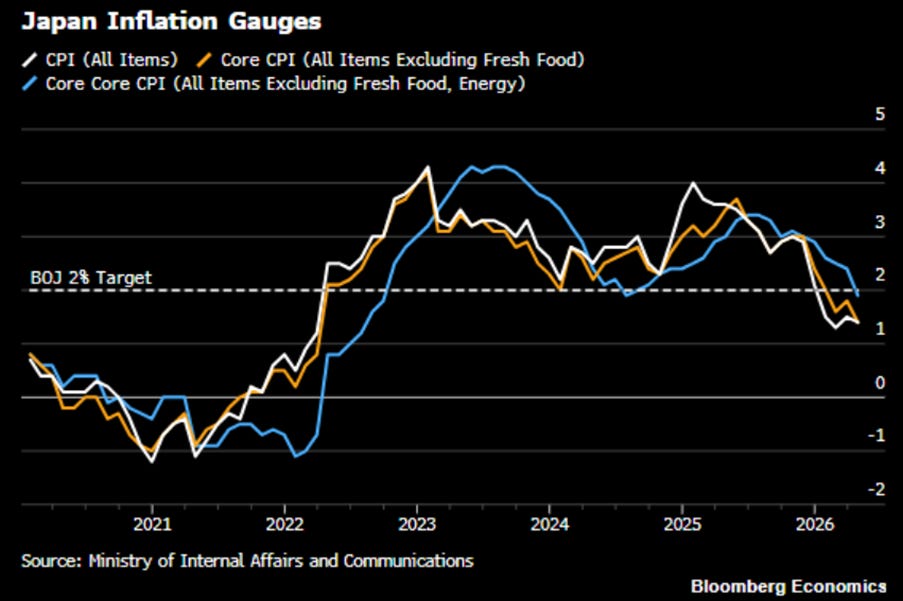

As another glorious episode of CP-Lie Z, Japan’s softer April inflation print was largely powered by base effects, cheaper government subsidised school lunches, and statistical ninja techniques rather than any real victory over inflation. Beneath the anime smoke screen, price pressures remain alive and well, with rising oil prices preparing their inevitable “final boss” return across the economy. The Bank of Japan now looks increasingly likely to unleash its next rate hike attack toward 1% in June.

In a rare moment of honesty from the Brussels bureaucracy, European officials are now openly admitting the continent faces a stagflation shock — as if Europe’s industrial collapse, exploding energy costs, and economic stagnation only appeared once missiles started flying in the Middle East. Apparently, destroying your own energy security, drowning businesses in regulation, and worshipping climate ideology for a decade was supposed to end differently. Now, with oil above $110 and growth evaporating, Europe has finally rediscovered the ancient economic principle that you cannot run an industrial economy on press conferences, subsidies, and moral superiority alone.

https://www.cnbc.com/2026/05/18/eu-stagflation-shock-iran-war-oil-prices.html

Welcome to the next phase of inflation, where prices are no longer only determined by supply and demand, but by how much the algorithm believes you can emotionally tolerate paying. Thanks to digital shelf labels, loyalty programs, in-store cameras, and AI-driven pricing systems, two people standing in the same grocery aisle may soon pay different prices for the exact same product — all in the name of “customer optimization.”

Retailers insist the technology is about convenience, efficiency, and improving the shopping experience, which in modern Orwellian translates roughly to: “the machine now knows your salary, your spending habits, your stress level, and how badly you need oat milk.” Your loyalty card, shopping app, and browsing history have quietly transformed you from customer into monetizable inventory.

In the future, inflation may not be universal at all. It may become fully personalized — a dynamic subscription service where the better the system knows you, the more efficiently it extracts your purchasing power while politely thanking you for your loyalty.

Tiktok failed to load.

Tiktok failed to load.Enable 3rd party cookies or use another browser

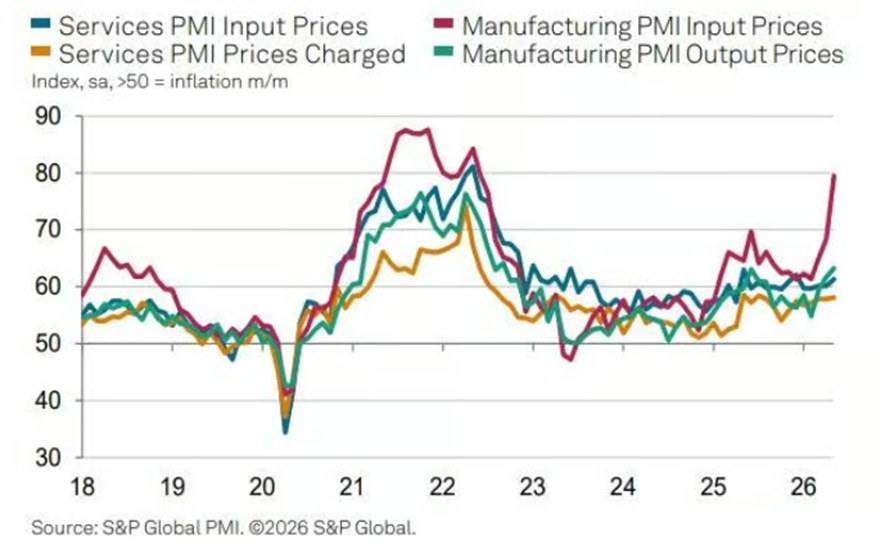

US manufacturing activity surged in May to its strongest level in four years as companies rushed to front-run the inflation shock triggered by the Middle East excursion — because nothing says “healthy economy” like panic-buying raw materials before the next oil tanker disappears from the Strait of Hormuz. Factory activity hit a 48-month high while input prices posted their biggest jump since 2022, supply chains slowed again, and businesses quietly started cutting jobs as costs exploded. In short, manufacturers are still producing, consumers are still paying more, and economists are once again discovering that “temporary inflation” has a remarkable talent for overstaying its welcome.

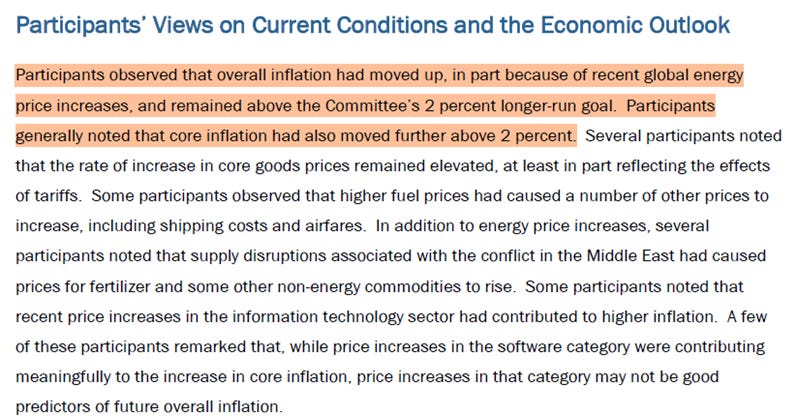

When a central bank speaks with many voices, markets should prepare for turbulence beneath the surface of apparent harmony. The latest FOMC minutes under Chairman “Too Late Jerome” revealed a Federal Reserve increasingly divided between officials fearing persistent inflation and others still dreaming of eventual rate cuts. A growing number of policymakers favoured removing the Fed’s easing bias altogether, while several officials acknowledged that renewed inflationary pressures tied to war and energy markets could justify keeping rates higher for longer — or even tightening further if inflation refuses to obey official forecasts. Meanwhile, stronger labour market data briefly restored confidence that the economy remains stable, proving once again that in modern monetary philosophy, one resilient payroll report can erase many inconvenient concerns.

https://www.scribd.com/document/1041425699/Fomc-Minutes-20260429

The deeper message from the minutes is that the Fed no longer speaks with unified conviction. Like an empire debating the weather while the river quietly rises, policymakers remain divided over whether the next move should be a cut, a hike, or simply another meeting explaining why certainty remains “data dependent.”

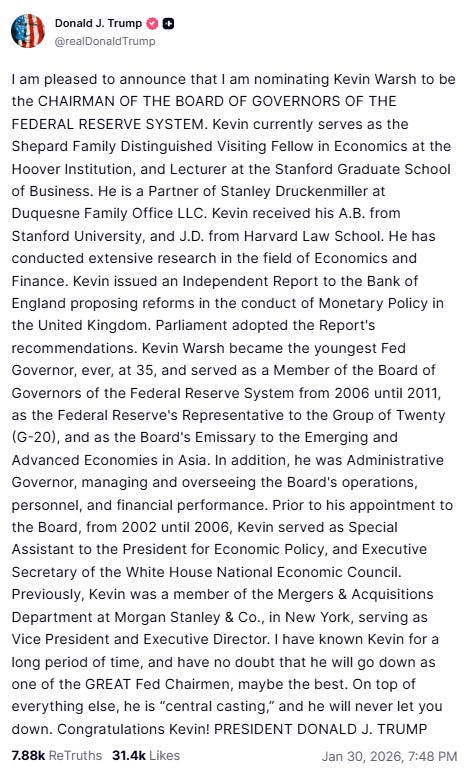

Although the new Chairman ‘Kevin The Wash’ has long favoured lower rates, he may soon discover that an increasingly hawkish Federal Reserve is not exactly in a rate-cutting mood. Kevin also supports a tighter balance sheet, even as everyone knows that shrinking liquidity too aggressively could destabilize the financial system — because apparently the post-2023 banking stress experience was not sufficiently educational. Meanwhile, Donald Copperfield delivered surprisingly calm remarks about ‘Kevin The Wash’, suggesting the future Fed chair may initially avoid the traditional “Too Late” public criticism package even if markets continue pricing a more hawkish policy path.

https://truthsocial.com/@realDonaldTrump/posts/115983891481988557

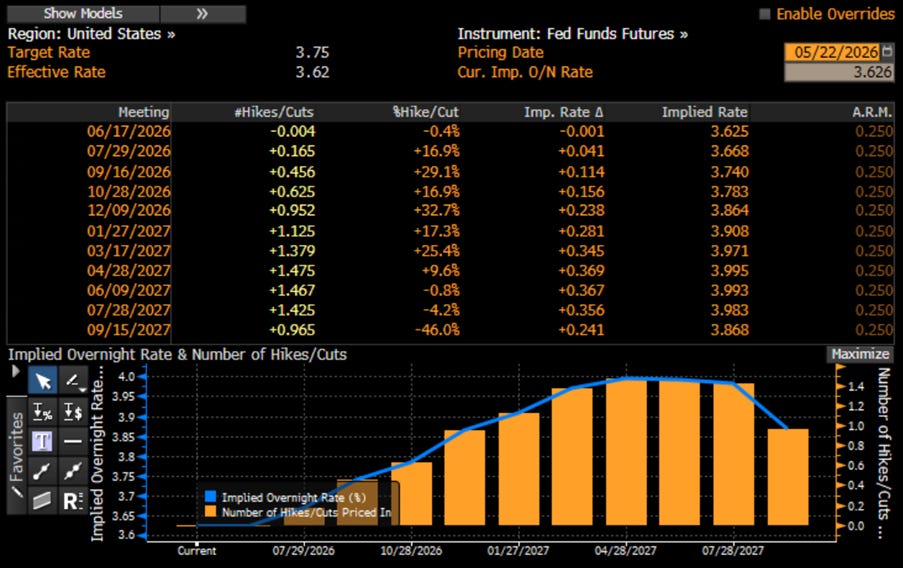

As the new Fed Chair was officially sworn in as Central Banker-in-Chief, Wall Street’s endlessly imaginative EYIs are increasingly awakening from their enchanted “rate cuts and a soft landing” fairy tale and are now pricing in a 25bps hike by December with a delightful 95% probability. Meanwhile, Trump Stagflation continues to evolve rapidly from a “baseless conspiracy theory” into what increasingly resembles the Empire’s official economic doctrine, while the Manipulator-in-Chief reassures the population that the Persian “little excursion” remains merely a minor inconvenience required to continue exporting democracy, inflation, and regime change all at once. At this stage, like most public institutions of the Empire, the Fed resembles less a central bank and more a nervous airline passenger politely handing the cockpit over to the bond market, while its credibility continues a graceful descent somewhere above the Strait of Hormuz — still technically a soft landing, just missing the runway, the engines, and possibly the plane itself.

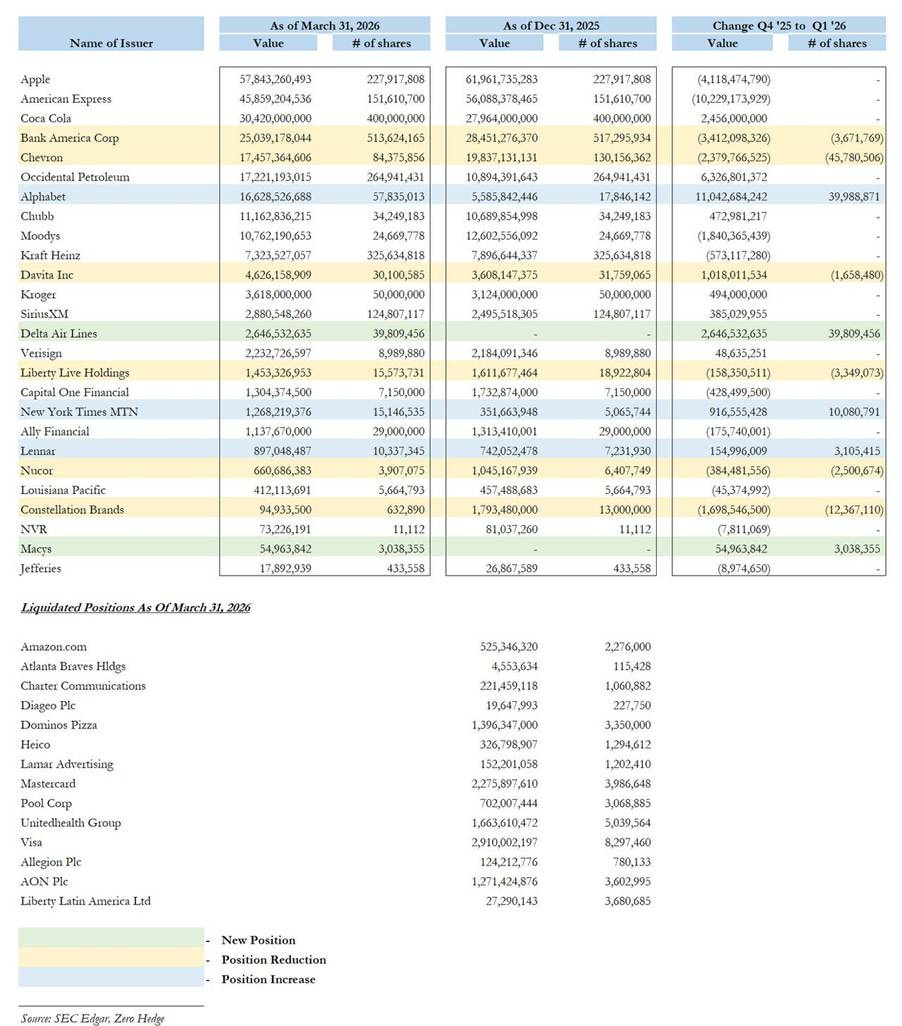

As Confucius almost certainly never said, “When the old master leaves the temple, the new monk redecorates aggressively.” Berkshire’s first full quarter under Greg Abel revealed a rare burst of activity, with the conglomerate taking a machete to 14 positions while simultaneously rediscovering its love affair with airlines through a new $2.6 billion stake in Delta — proving that in Omaha, even broken airline vows are apparently cyclical. Berkshire also added to Alphabet and opened a small Macy’s position, while quietly dumping Amazon, Visa, Mastercard, UnitedHealth, and a long list of other holdings. In the ancient art of portfolio management, this is known as “sweeping the courtyard before the new emperor arrives.”

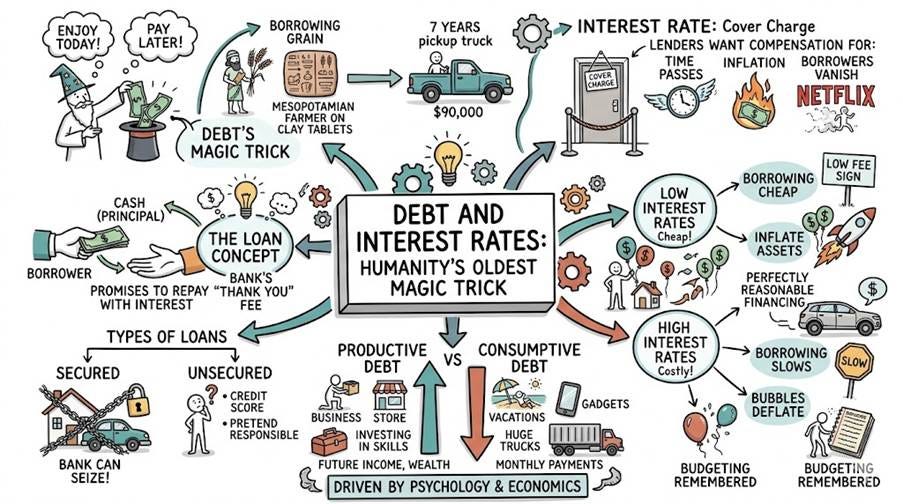

Debt is basically humanity’s oldest magic trick: enjoying money today and praying your future self-figures it out later. From ancient Mesopotamian farmers borrowing grain on clay tablets to modern consumers financing a $90,000 pickup truck over seven years, the principle has not changed much. A loan is simply the official contract behind this beautiful act of financial optimism. The lender hands over the cash — called the principal — while the borrower promises to repay it with interest, otherwise known as the bank’s “thank you for the risk” fee. Some loans are secured, meaning the bank can seize your house or car if things go badly, while unsecured loans rely entirely on your credit score and your ability to convincingly pretend you are financially responsible.

Interest Rate is basically the financial system’s cover charge. Lenders want compensation because time passes, inflation destroys purchasing power, and borrowers occasionally vanish like Netflix passwords after a breakup. Low interest rates make borrowing cheap, inflate asset prices, and convince consumers that financing a luxury SUV for seven years is perfectly reasonable. High rates do the opposite: borrowing slows, bubbles deflate, and suddenly everyone remembers what a budget is.

Not all debt is created equal. Investment debt is the kind that at least has the decency to try making you richer in the future — borrowing money to build a business, buy productive assets that can generate future income. Consumption debt, on the other hand, is financial time travel: enjoying tomorrow’s paycheck today on things that will probably lose value faster than your New Year’s resolutions. A loan used to expand a factory and build a bridge may create jobs and cash flow; a credit card used to finance a luxury vacation mostly creates Instagram stories and monthly payments. One debt plants a tree. The other buys a very expensive cocktail under a palm tree.

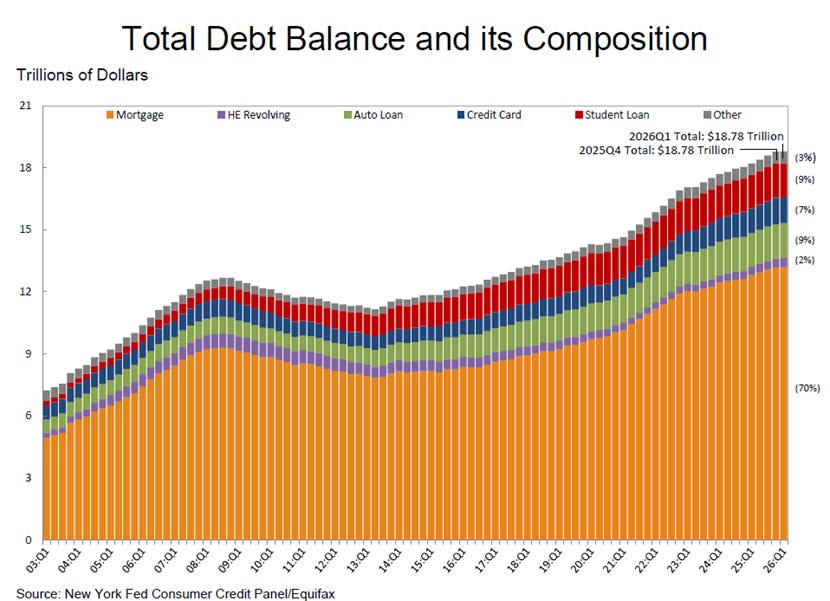

Mortgage debt is America’s favorite long-term relationship with a bank. It allows households to buy a home today and spend the next 30 years convincing themselves they are “building equity” rather than paying mostly interest for three decades. With roughly $12 trillion in outstanding balances, mortgages are the largest form of consumer debt in the US economy. The housing boom of 2020–2022, fuelled by ultra-low rates below 3%, turned millions of Americans into amateur real estate speculators overnight. Then rates jumped above 7%, creating the famous “lock-in effect”: homeowners with cheap mortgages are now financially glued to their houses because moving would mean replacing a bargain mortgage with monthly payments that resemble luxury car leases for a medium-sized suburban home.

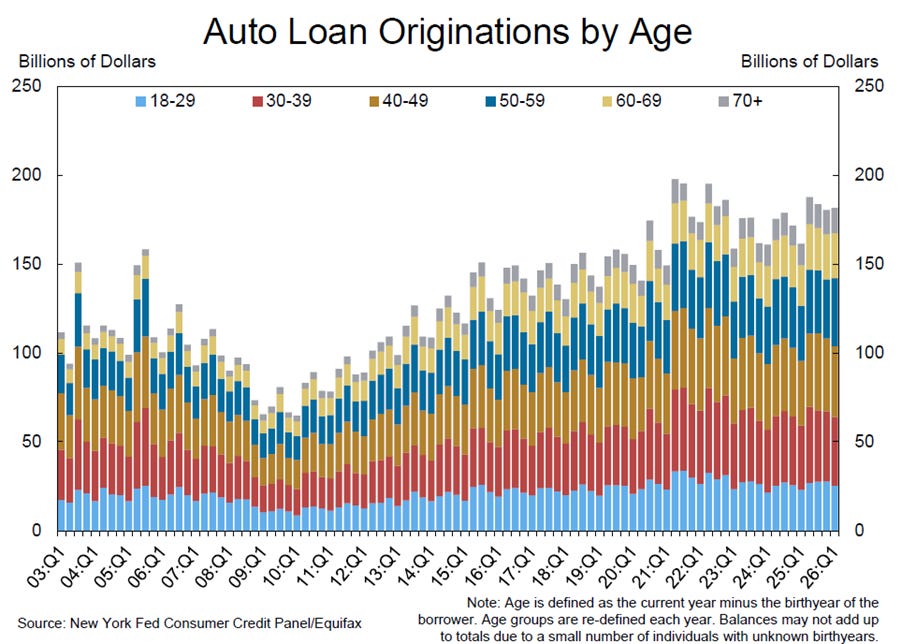

Auto loans are America’s preferred method of turning a depreciating asset into a long-term financial commitment. Consumers now routinely borrow over $40,000 to buy vehicles that lose value faster than politicians lose campaign promises. Thanks to rising car prices and seven-year financing terms, cars have evolved from transportation tools into rolling monthly payment subscriptions. Even better, many borrowers end up paying nearly luxury-vacation money in interest for a vehicle worth half its price by the time the loan is finally paid off. Meanwhile, the rapid growth of subprime auto lending means the industry has quietly recreated the same “what could possibly go wrong?” energy that once fuelled the housing bubble.

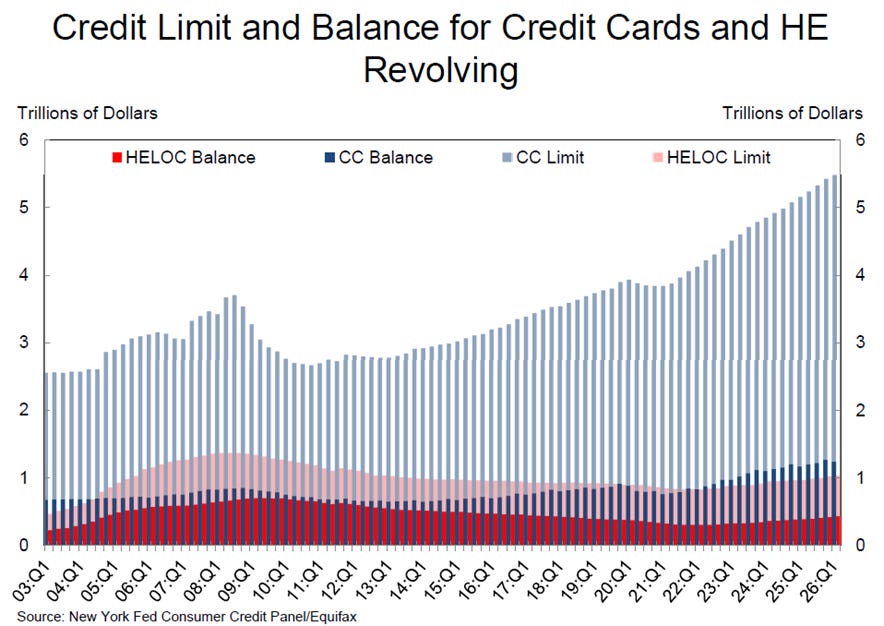

Credit card debt is the financial equivalent of setting your wallet on fire very slowly. Americans now carry over $1 trillion in revolving credit card balances, often at interest rates above 20% — high enough to make loan sharks look competitively priced. The system is beautifully designed for banks: minimum payments are so small that borrowers can spend decades paying interest on restaurant meals, groceries, and gadgets already forgotten or broken. The recent surge in balances is less a sign of consumer confidence than a national distress signal: when households start financing eggs and gasoline with credit cards, the economy is no longer booming — it is over drafting.

Student loan debt is the uniquely modern experience of paying university prices for a degree and then discovering the real major was compound interest. Americans now owe nearly $2 trillion in student loans, often borrowed without much consideration for whether the future salary can actually repay the debt. Universities happily raised tuition for decades knowing federal loans would keep flowing, while millions of graduates entered adulthood carrying debt large enough to delay buying homes, starting families, or occasionally even ordering guacamole without financial anxiety.

Keep reading with a 7-day free trial

Subscribe to The Macro Butler’s Substack to keep reading this post and get 7 days of free access to the full post archives.