Après Macron, Le Déluge?

THE WEEK THAT IT WAS...

The third quarter of 2024 started with a shortened holiday week in the US, but the US Independence Week was not short of macroeconomic data, with the focus being on PMI data in China and the US, as well as the latest health check of the US job market. On the front of central bank news flow, the FOMC chairman delivered a speech in a panel discussion with ECB President Lagarde, and the latest FOMC meeting minutes were released. The French and Brits also cast their votes in general elections, which will have significant implications for investors.

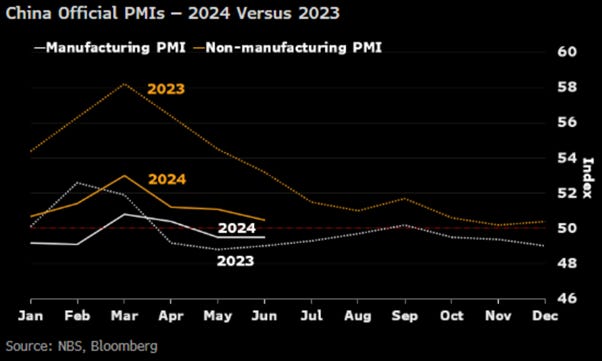

In China, the marginal rise in the manufacturing PMI did little to counter the narrative that the recovery continues to struggle to gather momentum as weak confidence hurts demand. The most troubling signal was the sharp slowdown in construction, suggesting that government-backed infrastructure spending, a key support for the economic recovery, is also losing steam. The non-manufacturing sector also showed persistent weakness in domestic consumption.

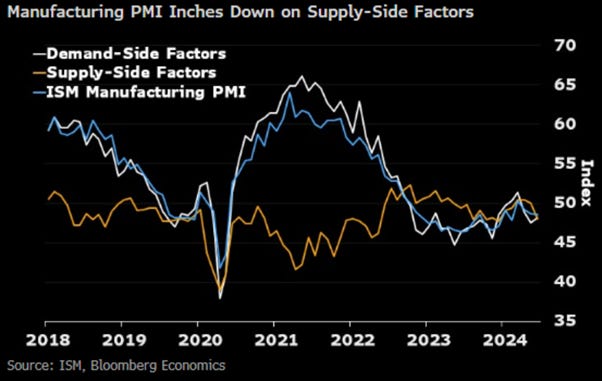

In the US, while the manufacturing PMI rose to 51.6, the ISM manufacturing index dropped to 48.5, well below the expected 49.1. S&P Global noted higher supplier charges in June, and alongside rising labour costs, this resulted in a marked increase in input prices. However, the ISM saw Prices Paid plunge from 57.0 to 52.1, well below the expected 55.8. Bottom line, the manufacturing PMIs spread further Forward Confusion, and some might interpret them as indicating that the return of the inflation boomerang could be losing momentum. However, this could be temporary as supply chain disruptions continue to push freight costs higher for much longer than expected.

The broad decline in the ISM services PMI, despite the start of the summer travel season, is another sign that the US economy is faltering. The headline ISM services PMI fell into contractionary territory at 48.8, down from 53.8 in the previous month. Business activity and new orders are also pointing to more weakness ahead, marking the first time since 2020 that both leading indicators were contractionary.

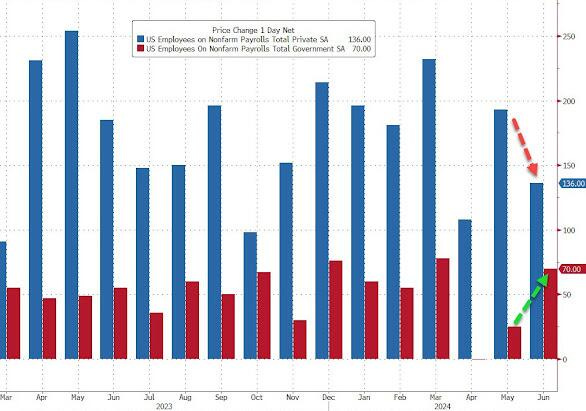

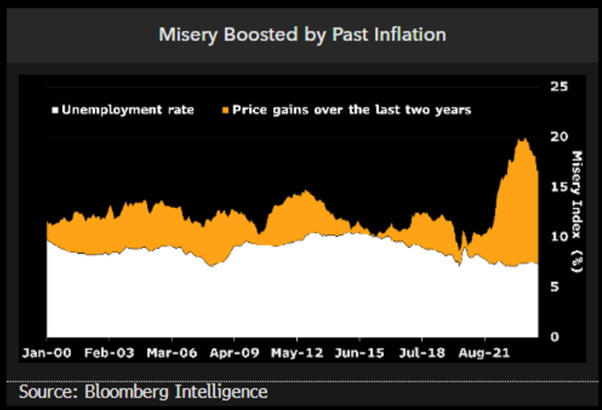

From afar, the June Non-Farm Payrolls report looks like another set of Goldilocks data with the US economy creating 206k jobs, above the consensus of 190k. However, as usual, May’s headline figure was revised down to 218k from 272k. Predictably, in a communist economy like the US under President Biden, ahead of the November election, government payrolls increased by 70k, compared to a 25k increase in May. Conversely, economically productive jobs created by the private sector came in at 136k, below the 160k expected and down from 229k in May.

The unemployment rate rose to 4.05% from 3.96% in the prior month, exceeding the consensus of 4.0%. This increase reflected growth in the labour force and the number of unemployed workers. Interestingly, the unemployment rate has been above the 24-month moving average since the start of the year. Historically, this has been the best indicator that the US economy has entered into a recession, which this time will be stagflationary as supply-driven shortages drive inflation substantially higher, regardless of the government-sponsored ‘Forward Confusion’ trying to convince voters and investors otherwise.

US Unemployment Rate (blue line); US Unemployment Rate 24 months moving average (green line) & US Recessions.

In a nutshell, June’s payroll report confirmed that unproductive government-related jobs keep increasing while layoffs in the private sector pushed the unemployment rate higher.

For those who still think that the US economy is healthy, rather than looking at government bond yields and corporate spreads, which are impacted by the rising understanding that the real problems lie within the government, the recent outperformance of Walmart compared to S&P global luxury retailers has historically been a better indicator of an upcoming recession. Recessions typically impact lower-income groups before wealthier consumers. Indeed, as the 'Walmart Recession Signal' has been rising since the end of 2023, it shows that consumers have been tightening their belts, as in stagflation they have to pay more to get less.

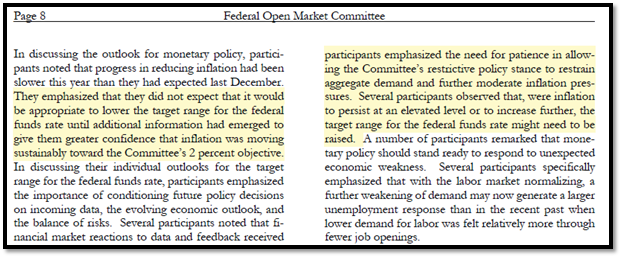

After the hawkish shift in the DOTs at the June FOMC meeting, the minutes confirmed that most FOMC members prefer to wait longer before initiating the FED pivot. The 'vast majority' assessed that economic growth is 'gradually cooling' and believe that the FED and AI will prevent an inflationary bust. They cited various factors such as demand-supply pressures, lagged effects of past monetary tightening, and delayed shelter price responses as contributing to the supposed 'continued disinflation.' Despite Jerome Powell's claims of unanimity, the FED appears divided on data response, with some officials advocating patience and others suggesting that rates might need to rise if inflation stays elevated or increases.

https://www.scribd.com/document/747656888/Fomc-Minutes-20240612#download&from_embed

Surrounded by the serenity of the Portuguese countryside of Sintra, Jerome Powell and the even more politically correct ECB President Lagarde continued their litany that both central banks need to gather more data before acting further on interest rates. As usual, Powell and Lagarde entertained markets with the possibility of starting or resuming the cutting cycle if data permits, of course. Regarding the US fiscal deficit, using his usual politically correct language, Powell stated that ‘We'll have to do something sooner or later, and sooner will be better than later’.

As the US heads into stagflation, the risk is that the FED will indeed raise rates in 2025 once the political circus is over, and the mask of politically correct verbiage from the FED chairman will no longer be necessary.

US Stagflation proxy indicator (blue histogram); FED Fund Rate (red line) & Correlation.

In the meantime, the FED still finds itself caught between a rock and a paradox as it entertains the phantasmagorical FED pivot amid Wall Street banksters.

At the end of the day, we all know that Wall Street and the Biden Administration need to continue luring donkey investors and voters into the supposed Goldilocks nirvana, while the FED has become impotent to solve economic issues driven by communist Keynesian policies.

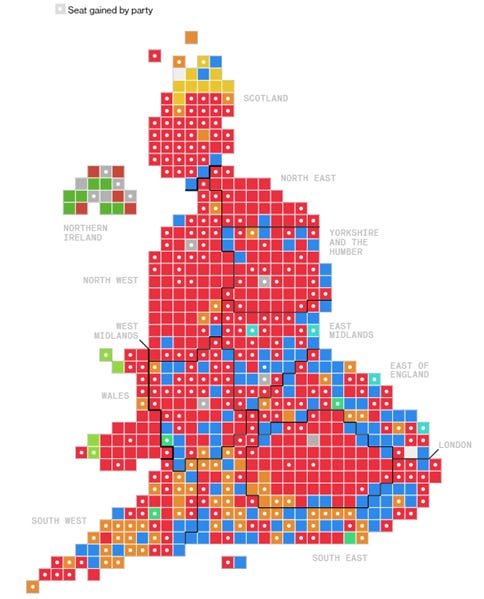

While Americans were celebrating their renamed ‘Dependence Day,’ on the other side of the pond, the Brits went to the polls and handed what looks like a landslide victory to the Labour Party, which won 412 seats, ending 14 years of Conservative government. Diving deeper, we see that Keir Starmer’s Labour Party only increased its vote share by a few percentage points from its dismal 2019 performance. From this perspective, it was not a landslide. Even though it may end up with almost twice as many seats, there are cracks in the foundation of Labour’s platform. Starmer won a smaller vote share than his predecessor, Jeremy Corbyn, did in 2017, an election that Labour had previously lost, illustrating that this was not the landslide the LEFT seeks to portray.

For those who believe this will substantially change the Keynesian and warmonger narrative implemented under the Sunak government, a quick look at Keir Starmer's statements at the latest Davos summit should make them more worried. Not only is Starmer advocating for more communist Keynesian regulations, financed by rising taxes of course, but he is also a proponent of the globalist climate change scam. In short, while a change was inevitable given the Sunak government's disastrous track record, what lies ahead for Britain may not be what those hoping to Make Britain Great Again were expecting but more Malthusian policies to spread fears and impoverish the people. The problem with Labour, like other Keynesians, is that they are never interested in reforming spending; they always insist on taxing the upper class to redistribute to others to keep their power.

Unless you lived under a rock over the past month, you must already know that June 2024 will most likely be remembered in political history books as the month when European investors cast their votes for the usually uneventful European Parliament elections, which turned out to be consequential for European politics. Indeed, in France, this vote triggered Macron to call a snap election, as his wounded ego of the "golden boy" president has likely started to spread chaos.

As the results of the first round French elections show, and as was widely expected, Ms. Le Pen's Rassemblement National (RN) was the main winner. The RN (and its dissenting LR allies) secured 33% of the votes and placed first in 298 out of 577 districts. The Nouveau Front Populaire (NFP) – comprising La France Insoumise (LFI) led by Mélenchon, the French Communist Party (PCF), Les Écologistes/EELV, and the Socialist Party of France (Parti Socialiste, PS) – won 28% of the votes. President Macron's centrist coalition, Ensemble (ENS) – Renaissance (RE), the Democratic Movement (MoDem), Horizons, En Commun, and the Progressive Federation – obtained 21%, and the center-right Republicans 10%.

Ahead of the second round, the prospect of an outright majority (289 seats out of 577) for RN remains uncertain, as it also depends on whether any candidate from the left or the president’s coalition will drop out in three-way races and how an alliance between NFP and ENS will end up benefiting the opposition to RN.

As the year of political hell unfolds, investors must understand that elections have consequences, with some elections having more significant impacts than others. Like everywhere in the world, the French banked their votes with their wallets in mind. Ahead of the first round of the election, the top three voter concerns were the economy, security, and immigration.

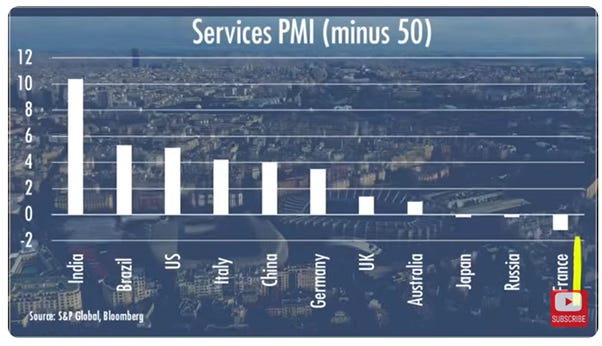

The French economy has barely grown over the past five years. This year, the IMF forecasts France to grow by a mere 0.7%. As a result, per capita GDP in real terms is barely above the pre-COVID level. In layman’s terms, this means no improvement in the standard of living. To illustrate the stagnation of the French economy, despite the expected tourism boom linked to the upcoming Summer Olympics in Paris, the service sector in France is performing worse than in Russia.

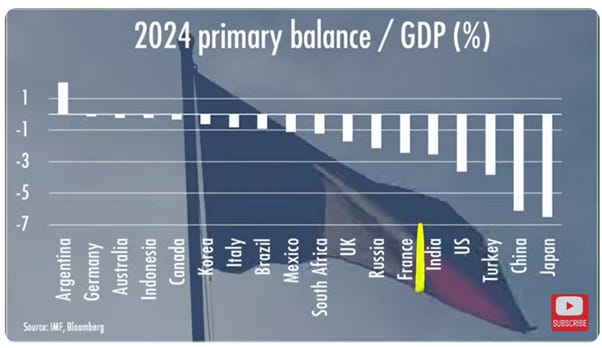

The French fiscal situation is in a bad shape with French Primary deficit (before interest payments) to GDP at 2.4%, again worse than supposed weakened by the war Russia.

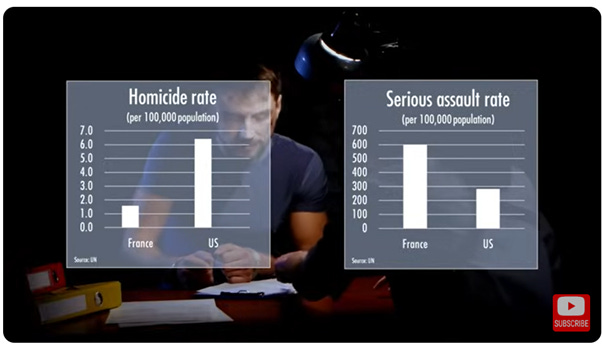

It is undeniable that the French are right to hold Macron responsible for the poor state of the economy. On top of that, looking at security, the second preoccupation of French voters, the serious assault rate is the highest among major European countries. Moreover, violent assaults have increased by 60% over the past 10 years. While the US still has a higher murder rate than France, there are many more violent assaults in France than in the US.

Immigration which has been stimulated by Macron’s globalist agenda has been cited as one of the reasons for the rising crime rate. While 10% of the total French population is Muslim, yet an estimated 70% of the French prison population is Muslim.

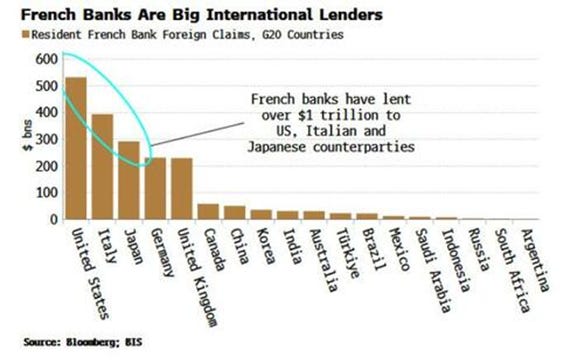

While many investors may think that what is happening in France is irrelevant for their portfolios, turmoil in France has the potential to spread globally through its banks, a key vector of financial contagion during crises. French banks are the fourth largest international lenders, with $2.4 trillion in foreign loans. The biggest borrowers from French banks are the US, Italy, and Japan, while UK, US, and Japanese banks have lent the most to France.

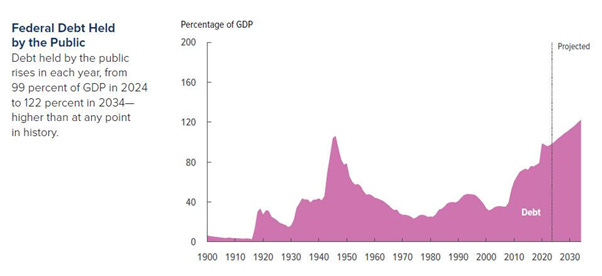

With France's political instability now in the spotlight, there is a risk of reappraisal of its assets relative to its deteriorating fundamentals. The risks are arguably greater for France than for the UK, given that 48% of French local and central government debt is owned by non-residents compared to 31% of UK gilts. France's public finances have worsened, with its debt-to-GDP ratio now at 111%, or approximately EUR3 trillion. While peripheral countries like Portugal and Greece have seen their debt ratios fall over the past five years, France's debt has risen more than that of any other major eurozone economy.

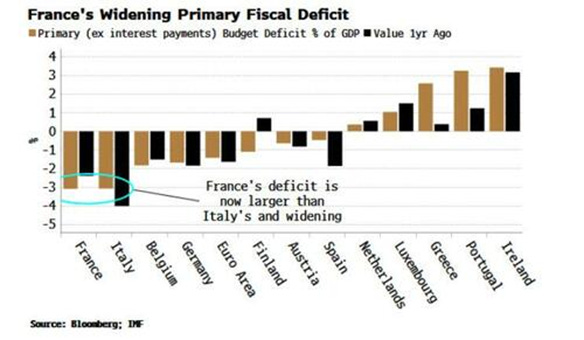

Debt is a stock problem, but it's less concerning if the flow is positive. In France, it isn't. The budget deficit stands at 5.5% of GDP, only worse than Italy's among major eurozone countries. However, Italy's deficit is burdened by legacy debt from the 1990s, and its primary budget balance (excluding interest payments) has been significantly better, indicating a more sustainable debt repayment path. In contrast, France's primary deficit is now worse than Italy's and rising. This highlights a structural issue affecting France's ability to repay its debt, while peripheral countries like Greece, Portugal, and Ireland are running significant primary budget surpluses.

There is little sign of any structural change ahead. France continues to be one of the most dirigiste countries in the world, and the largest in Europe, with government expenditures totaling 58% of GDP. France’s state is so large that the public sector employs 5.3 million people (21.1% of the active population), a ratio of civil servants to inhabitants of 70.9/1,000, according to Eurostat.

It’s not just public debt that’s rising in France; private debt is also on the rise. Among the main euro-zone countries, only Luxembourg and the Netherlands have higher private debt relative to GDP. Luxembourg's debt is primarily due to its status as an international finance centre, while in the Netherlands, it's largely driven by mortgage debt. Although the Dutch private debt-to-GDP ratio is declining, France's has increased more than any other country's over the last decade. At 228%, it ranks sixth highest among major emerging market and developed countries worldwide.

Furthermore, France’s debt service ratio, which measures the ratio of servicing private, non-financial debt repayments to disposable income, is approaching the critical 20% threshold observed in other countries before financial crises. To sustain the rapid increase in both public and private debt, France requires domestic capital. However, its current account deficit is among the highest of the major euro-zone countries, surpassed only by Greece. Similar to the periphery countries during the euro-zone crisis, which faced significant current-account deficits, there is no quick solution for France. It cannot devalue the euro to enhance export competitiveness or boost domestic savings, leaving asset adjustment as the primary mechanism for rebalancing.

Once again, things are heading in the wrong direction for France. The sum of its public deficits equals its public debt, while its current account deficit mirrors its negative net international investment position (NIIP). France's NIIP, already negative, ranks among the lowest compared to other euro-zone countries. Unlike peripheral countries improving their NIIPs, France's continues to deteriorate.

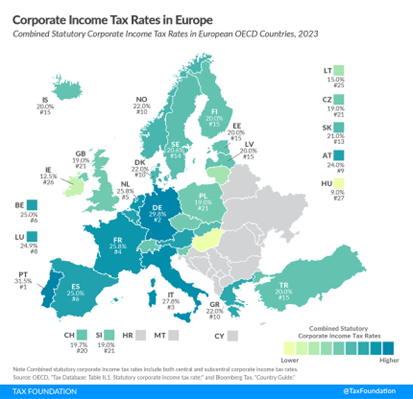

France has one of the highest tax systems in the OECD. Income tax and employer social security contributions account for 82% of the total tax wedge. Corporate tax rates are also high at 26.5%, and companies with profits over EUR500,000 pay 27.5%. Labor market regulations are so restrictive that the number of companies with 49 employees is 2.4 times higher than those with 50, due to significant burdens at the fifty-employee threshold. A 50-employee company must create three worker councils, introduce profit sharing, and submit restructuring plans to these councils if they fire workers for economic reasons.

These characteristics highlight a society with a large state, high progressive taxes, and an extensive social network. In essence, France exemplifies how communist Keynesian policies can lead to stagnation and ultimately stagflation, making everyone poorer as they have to spend more to get less to finance a plutocratic government.

Investors will have to wait until the night of July 7th to learn who will lead France's new government. The two main political groups, Rassemblement National (RN) and Nouveau Front Populaire (NFP) are on opposite sides of the spectrum. RN, mislabelled as far-right by mainstream media, may implement more progressive economic policies that clash with the EU's globalist agenda. NFP, a socialist-communist party venerating Simon Bolivar and Pol Pot, will push for increased social benefits, rising taxes as France would easily become the ‘Peronist Argentina’ under such an additional round of Keynesian regulations. Ultimately, similar to the US, both parties are looking to increase government deficits, which could endanger French banks and all holders of French government debt.

French history and literature abound with memorable statements that have endured through time. Louis XV, sensing the signs of the approaching Revolution, is famously remembered for saying ‘Après moi, le déluge’ ('After me, the flood'). In 2024, this statement could easily be rephrased as ‘Après Macron, le déluge’, (‘After Macron, the flood’) as whoever secures the majority of seats in the National Assembly on June 7th, the repercussions for financial markets and the French economy are likely to resemble a flood.

https://en.wikipedia.org/wiki/Apr%C3%A8s_moi,_le_d%C3%A9luge

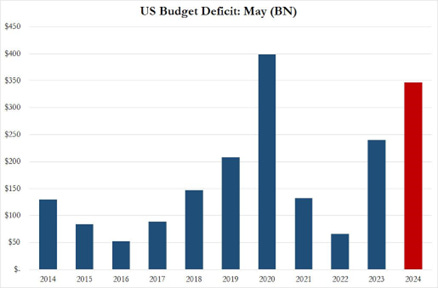

Back in the US, while investors were focused on ‘Jensanity’ at the end of last month, the US Treasury reported that in May, the US government collected $323.6 billion in tax receipts but spent more than double that amount, totalling around $670 billion.

This resulted in a May budget deficit of $347 billion, which was about $100 billion more than consensus expected. It marks the second biggest May deficit on record, with only the peak during the Covid crisis in May 2020 being higher.

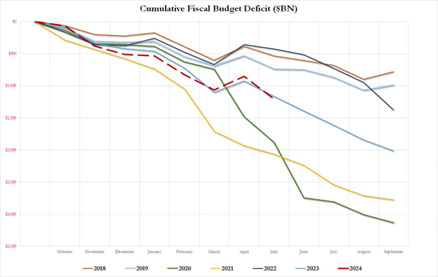

As a result of the blowout May deficit, the cumulative fiscal 2024 shortfall once again surpassed the total for 2023, bringing the year-to-date deficit to just over $1.2 trillion. This amount exceeds the $1.16 trillion cumulative deficit through May 2023, with four more months left in the fiscal year.

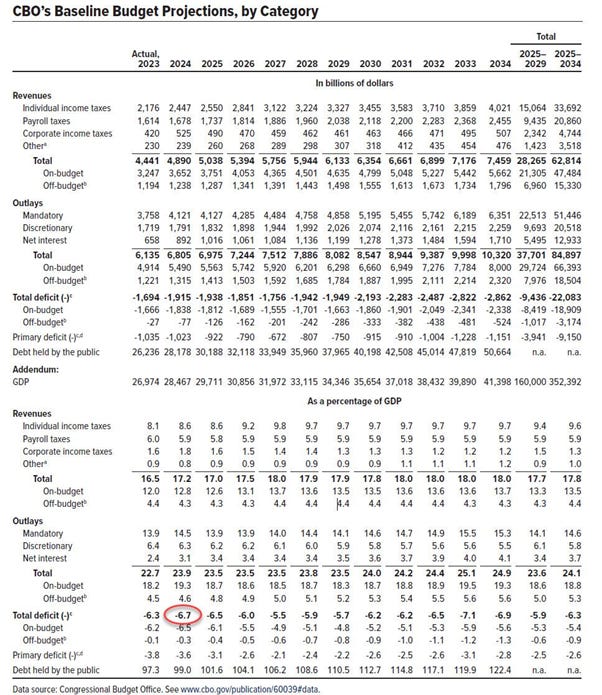

Now, at this point, someone at the CBO with a functioning brain looked at the numbers and realized that their current forecast of ‘only’ $1.5 trillion for the 2024 deficit seemed at best unrealistic and at worst, like total propaganda adding to the Forward Confusion narrative. Indeed, with just 4 months left in fiscal 2024, the CBO revised its forecast, raising the 2024 budget deficit projection from $1.5 trillion to $1.9 trillion. This revision confirms that there will be effectively no improvement in the fiscal picture between 2023 and 2024. In its latest projections, the Congressional Budget Office (CBO) predicted that government spending would continue to rise as there is a bipartisan agreement on that point.

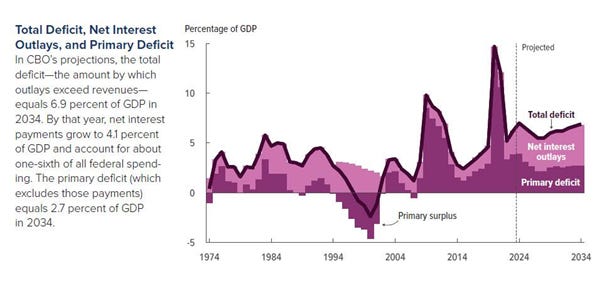

The office attributed the 27% spike in the deficit to several key drivers. These include foreign military aid (allegedly related to ongoing support in Ukraine), actions by the Biden administration on student loans, slower recovery of payments by the Federal Deposit Insurance Corporation following bank failures, higher Medicaid outlays, and increases in government discretionary spending. Additionally, the $1.2 trillion in interest expense on federal debt exacerbates the situation, leading the CBO to revise its 2024 deficit-to-GDP ratio forecast from a previous prediction of 5.3% to 6.7%.

Meanwhile, the cumulative deficit from 2025 to 2034 is projected to reach $22.1 trillion, which is 10% higher than the office previously projected in February, marking a $2.1 trillion increase.

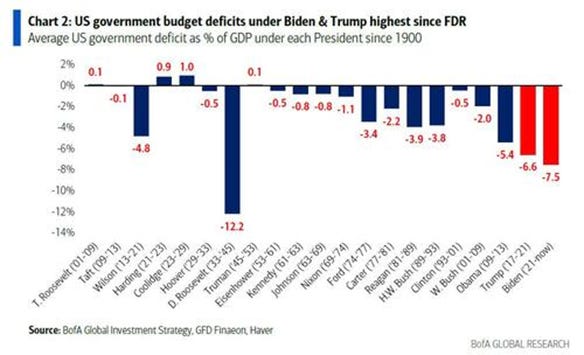

Of course, by the time 2034 rolls around, not only none of the current president candidates will still be around but the actual deficit will likely be significantly higher, meaning that for both of them, these financial metrics may seem inconsequential. Investors and voters should note that under both Trump and Biden, U.S. government deficits have been the highest since Franklin Delano Roosevelt's presidency during World War II. This suggests that the ultimate goal of the plutocrats in power, regardless of party affiliation, is to push the world into another war to divert attention from the inevitable default of the US government on its sovereign debt.

According to the CBO, the largest factor behind the increased cumulative deficit was recent legislation adding $1.6 trillion to projected deficits. This included $95 billion in emergency appropriations for aid to Ukraine, Israel, and Indo-Pacific countries, with ongoing funding adjusted for inflation expected to increase discretionary outlays by $0.9 trillion through 2034. Additionally, the CBO highlighted that deficits over the next decade are about 70% higher than their historical average relative to economic output. This suggests the US has passed the ‘Minsky Moment,’ facing potential consequences when the USD loses its reserve currency status. With rising interest costs and expenditures on programs like Medicare and Social Security, federal outlays are projected to peak at 24.9% of GDP in 2034, up from 24.2% in 2024. The CBO admits there's no scenario where future deficits will decline to zero, indicating a tough fiscal road ahead.

As the year of political hell will culminate on November 5th when American citizens go to the polls to elect their president and renew half of the Congress and Senate, everyone will agree that it takes a lot of gumption to go on television and repeatedly lie to over 300 million Americans, who undoubtedly have higher cognitive capabilities than the first among them. Investors and consumers will remember that while the current president can cherry-pick a few numbers to try to present himself favourably, these are facts that he doesn’t want US citizens to know:

In this context, the Western world is about to understand the meaning of the old saying ‘Weak men create hard times’…

In the meantime, nearly every aspect of American life is influenced by unelected government agencies that can implement regulations without consistent adherence to a uniform rule of law. This is how the ‘Deep State’ exerts control in what the Western mass media portrays as an exemplary democracy, but which resembles more of a plutocratic gerontocracy.

Politics have never been as divided as they are today. While politics has always been divisive, America has never been less united. Even during Barack Obama's presidential campaigns, despite the left vs. right divide, there was still a sense of shared identity as Americans first and foremost.

Tiktok failed to load.

Tiktok failed to load.Enable 3rd party cookies or use another browser

Today’s political debates have devolved into outright battles, with each side believing the other doesn't deserve to share the same land. This echoes the sentiment from the movie ‘Civil War,’ where a separatist soldier asked, ‘What kind of American are you?’ This mindset is prevalent today, reflecting the deep divisions in society. This will ultimately lead to a massive rise in civil unrest that will explode by the beginning of September. The 2024 US Presidential Election features two fundamentally different visions for America's future, not just a typical Republicans vs. Democrats contest. Widespread economic dissatisfaction, fuelled by years of strain, a pandemic, mass migration, and woke politics, has created deep animosity. Many fear a civil war is inevitable as both sides seek to reclaim their version of America. By 2028, there may not be a US Presidential election at all.

Once the majority realizes that their vote will not make much difference, as the fiscal deficit will continue to rise regardless of who is the next tenant of the White House, the US empire is likely to implode from within rather than being defeated on the battlefield despite the Washington warmongers attempting to spread conflict globally to divert attention from the harsh realities faced by average Americans.

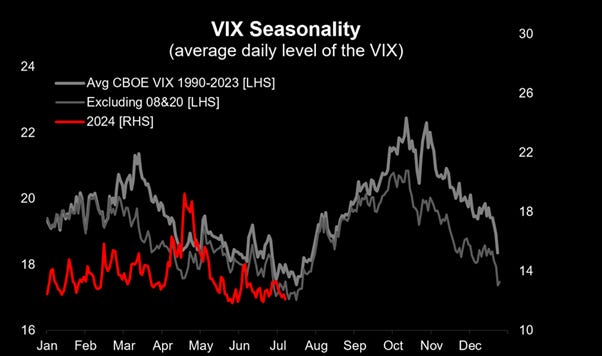

Coming back to financial markets, historically, option markets begin pricing in the US elections around 3 months before the event. While we are not there yet, volatilities are expected to start reflecting anticipation of the elections soon.

As a reminder, over the past 20 years, the VIX has typically bottomed out later in July due to seasonality.

Goldman Sachs recently surveyed 800 global investors, summarizing their views as follows: Investors fear a unified government that gives the executive branch more spending power, which is seen as even more negative for bonds (yields up).

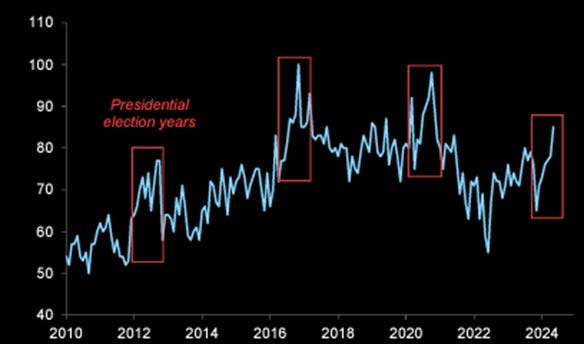

In election years, there is historically uncertainty among small business owners, who are reluctant to proceed with significant decisions ahead of potential changes in fiscal regulations following the inauguration of a new president and administration.

In this context, economic surprises are expected to deteriorate further, while the return of inflation is likely to accelerate as the base effect becomes less favourable. This challenges the narrative of a "Goldilocks" scenario for the US economy. Instead, rising uncertainties domestically and internationally suggest a scenario of consumer-driven stagflation, where people buy less for more.

Citi US Inflation Surprise Index (blue line); Citi US Economic Surprise Index (red line) & US Recessions.

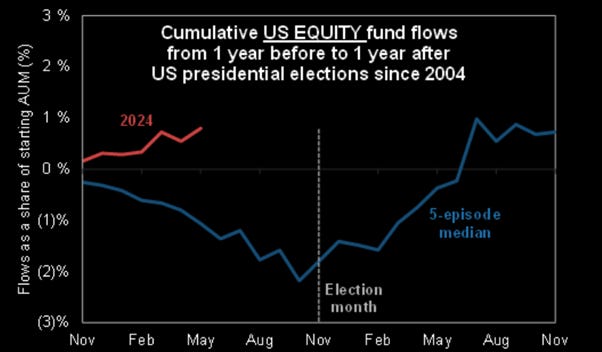

Based on historical seasonality over the past 20 years, US equity markets typically experience outflows as we approach Election Day.

For the equity market, the consensus has increasingly priced in a scenario where Trump wins the election and Republicans control both Congress and the Senate (i.e., a Republican sweep), seen as the most likely outcome if the election proceeds without irregularities given the disastrous state of the US economy which has been managed over the past 4 years for the Democrat’ plutocrats.

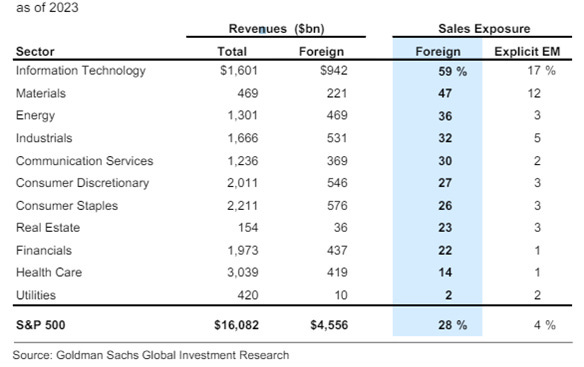

The impact on asset classes is expected to result in a strengthening of the US Dollar regardless of who wins the White House, given the developing political and geopolitical challenges globally. Trump's potential tariff policies, such as a proposed 10% across-the-board tariff on imports and a 60% tariff on imports from China, could significantly increase inflation. These tariffs would likely pose a challenge to stocks with high international revenue exposure due to the risk of retaliatory tariffs and heightened geopolitical tensions. It may surprise some that the tech sector has the highest international sales exposure with 59% of total revenues (including 17% from emerging markets), while cyclicals follow closely behind.

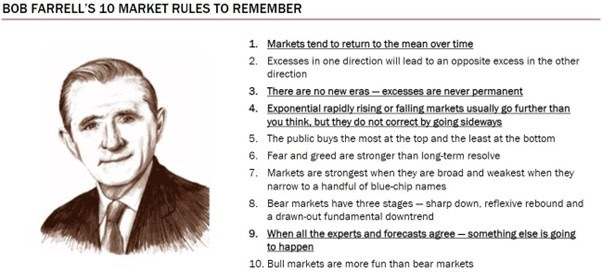

As mentioned over the previous weeks, seasoned investors know that profits are not realized until a position is sold. They also understand that there are times to buy and times to sell.

As Bob Farrell's rule number 1 and 5 highlight, ‘Markets tend to return to the mean’ and ‘The public buys the most at the top and the least at the bottom.’

The deterioration of the political environment not only in Europe but also in the US increases uncertainty in financial markets and is broadly risk negative in the short-term. As the collapse of the establishment unfolds in major Western countries, it suggests that the future will look markedly different from the past decades. These rising uncertainties are likely to translate into increased volatility for global risk assets. Moreover, rather than central banks, which have shown their inability to solve economic problems, the biggest market drivers are now likely to be political developments. After all, economies and financial markets are downstream from politics, as governments set the rules and play a major role in economic activities. In this context, investors with common sense should consider that now is the time to avoid the Fear of Missing Out (FOMO) syndrome, as elections, rather than central bank policies, will drive markets as the second half of the year of political hell unfolds.

WHAT’S ON THE AGENDA NEXT WEEK?

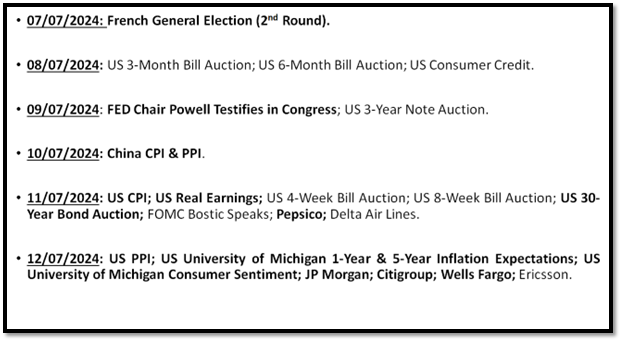

In the second week of the third quarter, investors will focus on inflation data from China on Wednesday and the US on Thursday. Attention will also be on Chairman Powell's testimony before Congress on Wednesday, followed by another round of consumer sentiment and inflation expectations data on Friday. The week also marks the official launch of the second quarter earnings season, with PepsiCo reporting on Thursday and JP Morgan, Citigroup, and Wells Fargo among other US banks reporting on Friday.

KEY TAKEWAYS.

As the summer season unfolds, here are the key takeaways:

China's PMIs confirmed that more time is needed to Make China Great Again, as the PBOC and the government choose the hard way to rebuild the economy in the post-COVID world.

The US PMIs confirmed that the US economy is edging closer to an inflationary bust.

The US Non-farm Payroll report was another indicator that the US economy is increasingly driven by government spending, with borrowed money being used to hire bureaucrats to implement uneconomical regulations.

The FOMC minutes and the latest speech by FED Chairman Powell confirmed that the now impotent Fed still needs more data before embarking on the phantasmagorical pivot sought after by Wall Street.

Whichever party wins the second round of the French general election, France is heading into significant financial and economic troubles.

Turmoil in France has the potential to spread globally through its banks, a key vector of financial contagion during crises.

As the US government keeps spending like a drunken sailor, whoever the next tenant of the White House is, the US deficit will continue to rise, and inflation will remain stickier for much longer.

Outflows and rising volatility are expected to be the hot topics du jour for financial markets as we get closer to the US election.

Rather than central banks, which have proven impotent to solve economic problems, political developments are now likely to be the biggest market drivers.

With continued decline in trust in public institutions, particularly in the Western world, investors are expected to move even more into assets with no counterparty risk which are non-confiscatable, like physical gold.

US Treasuries are now not only a 'return-less' asset class but, given their high correlation with equities, have also lost their rationale for being part of a diversified portfolio.

For income investors, rather than chasing long-dated government bonds, they should focus on USD investment-grade US corporate bonds with a duration not longer than 12 months to manage their cash.

In a stagflation, the best way to protect wealth is still to own the equity barbell portfolio made of Tech and Energy and Physical Gold and avoid long dated bonds.

As stagflation rather than recession materializes as the economy is increasingly weaponized, investors should prepare their portfolios for HIGHER volatility.

In this context, investors should also remain prepared for dull inflation-adjusted returns in the foreseeable future.

HOW TO TRADE IT?

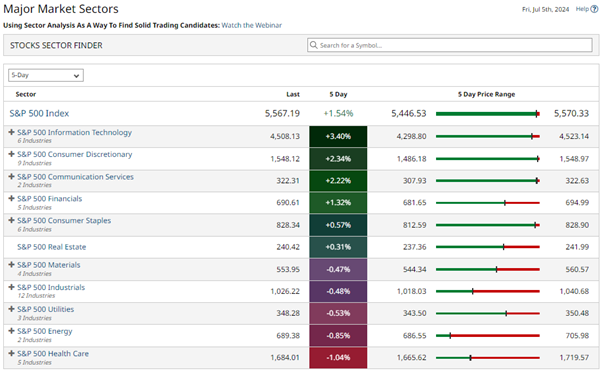

The second half of the year started with a wild, holiday-shortened, and illiquid week marked by dismal macro data. This led to renewed dovish expectations of a phantasmagorical FED pivot, pushing the Nasdaq to its best week since late April and the second-best week since early November. The S&P 500 also ended at a new all-time high, but unsurprisingly, the equal-weight S&P is still massively underperforming the market cap-weighted index.

In this context, it should be no surprise that growth sectors like IT, Consumer Discretionary, and Communication Services moved higher, while Energy and Healthcare lagged behind.

As signs of consumer-led stagflation in the US economy increase and political risks take centre stage, investors must prioritize risk management over the fear of missing out to navigate rising market volatility. Given these considerations, investors should hedge their portfolios with decentralized assets free of counterparty risk, focusing on the return OF capital rather than the return ON capital. The ultimate asset with no counterparty risk remains physical gold. In a stagflationary environment, it is crucial for all investors, whether institutional, high net worth, or retail, to allocate 20% to 40% of their assets to physical gold stored outside the traditional banking system.

US Stagflation proxy index (blue histogram); Inflation adjusted performance of Bloomberg US Treasury Total Return Index (red line) & Gold price (green line).

If this report has inspired you to invest in gold, consider Hard Assets Alliance to buy your physical gold: https://www.hardassetsalliance.com/?aff=TMB

For investors looking to stay invested in equities while acknowledging the rising risks of stagflation in the next 6 to 12 months, many indicators suggest a major rotation from the Tech sector into the Energy sector.

US Stagflation proxy index (blue histogram); Relative performance of S&P 500 Energy to S&P IT sector (red line) & correlation.

Those looking to capitalize on this trend using an option strategy can benefit from the rotation within the barbell equity portfolio from Tech into Energy. They can buy a 5% Out of the Money Put on the VanEck Semiconductor ETF (SMH US) and finance this put by selling an At the Money Put on the SPDR Energy ETF (XLE US). This strategy is an almost free lunch until the end of the year (i.e., December 20th) and at the end of the day the main risk is to add to the Energy sector at the current attractive level of valuation as we move ahead in the war cycle.

For fixed-income investors, owning government bonds in developed or emerging markets has become risky. In the current environment it is reckless to own government bonds with maturities over six months. That’s why investors should focus on investment-grade bonds issued by US corporations with an average maturity of less than 12 months.

At The Macro Butler, our mission is to leverage our macro views to provide actionable and investable recommendations to all types of investors. In this regard, we offer two types of portfolios to our paid clients.

The Macro Butler Long/Short Portfolio is a dynamic and trading portfolio designed to invest in individual securities, aligning with our strategic and tactical investment recommendations.

The Macro Butler Strategic Portfolio consists of 20 ETFs (long only) and serves as the foundation for a multi-asset portfolio that reflects our long-term macro views.

Investors interested in obtaining more information about the Macro Butler Long/Short and Strategic portfolios can contact us at info@themacrobutler.com.

Unlock Your Financial Success with the Macro Butler!

If this report has inspired you to invest in gold, consider Hard Assets Alliance to buy your physical gold: https://www.hardassetsalliance.com/?aff=TMB

Disclaimer

The content provided in this newsletter is for general information purposes only. No information, materials, services, and other content provided in this post constitute solicitation, recommendation, endorsement or any financial, investment, or other advice.

Seek independent professional consultation in the form of legal, financial, and fiscal advice before making any investment decisions.

Always perform your own due diligence.

Of course they lie when things are really bad (see jean claude juncker)... so one has to wonder if the money supposedly going to Ukraine ... is really going to Ukraine ...

I smell a rat https://fasteddynz.substack.com/p/the-ukraine-war-is-fake/

Britain is producing the smallest amount of energy on record as a plunge in North Sea fossil fuels leaves the country more reliant than ever on imports. https://finance.yahoo.com/news/british-energy-production-plunges-record-060000775.html

https://ichef.bbci.co.uk/news/946/cpsprodpb/10F88/production/_124721596_nsta-oil-production-nc.jpg

The only reason the UK did not collapse in the 70's... was north sea oil.... and that is mostly burned up now