Code Is the New Cure

Medicine Was a Repair Shop. AI Just Turned It Into a Lucrative Prediction Business.

The Week That It Was…

The first full week of Q3 arrived with the energy of a Monday morning after a long weekend — technically a trading week, practically an extended holiday. The data calendar offered precisely two items worth abandoning the beach umbrella for: the US ISM Non-Manufacturing, , and the FOMC meeting minutes — a 47-page confirmation that the Fed remained data-dependent, uncertain, and monitoring developments closely. China released its latest edition of the CP and PP-Lies, showing exactly what Beijing’s statisticians decided inflation looked like this month. For stock pickers, Q2 earnings season opened on a deliberately modest note: PepsiCo confirmed Americans are still stress-eating their feelings at stagflationary prices, while Delta Airlines revealed that the consumer who can’t afford a house has at least decided to take a holiday to forget about it.

As the Empire lit up its skies with billions worth of fireworks to celebrate 250 years of liberty, freedom, and the pursuit of happiness, the historical record quietly noted that the United States has been at war for approximately 232 of those 250 years — meaning the republic has enjoyed fewer than two decades of peace across its entire existence, a track record that would make the Roman Empire blush with professional admiration. From the Revolutionary War to the Indian Wars to the Spanish-American War to two World Wars to Korea to Vietnam to Iraq (twice) to Afghanistan (twenty years) to Libya to Syria to Yemen to the current Middle Eastern “excursion” that was won on Hour 1 of Day 1, the pattern is less a foreign policy and more a business model — one that now costs $900 billion annually, has produced a $40 trillion national debt, and requires invoking the Defence Production Act to restock the munitions consumed in the latest instalment.

The Founding Fathers, who warned explicitly against foreign entanglements and standing armies, would observe the 250th anniversary with the quiet horror of architects watching their building used as a demolition training site.

In a landmark ruling that required approximately two decades of warrantless mass surveillance to motivate, SCOTUS has delivered a 6-3 decision confirming that carrying a smartphone does not constitute voluntary consent to be tracked, catalogued, and retrospectively investigated by law enforcement — a conclusion articulated with the quiet gravity of someone explaining to a very large institution that the Fourth Amendment still exists. Geofence warrants — the investigative tool that allows police to define a geographic area, compel Google to identify every device present, and then decide who becomes a suspect afterward — have been ruled a constitutional search, inverting the surveillance apparatus’s preferred operating sequence of “search everyone first, find the crime later.” The ruling is genuinely important and genuinely insufficient: it does not end digital surveillance, it does not address AI-driven mass data analysis, it does not constrain the parallel architecture of licence plate readers, SignalTrace device harvesters, or the dishwasher-to-dog-microchip surveillance network the CIA director publicly described in 2012 — it simply reminds a government that has spent twenty years building the most comprehensive civilian monitoring infrastructure in human history that one specific warrant type now requires probable cause. The Supreme Court drew a line in the digital sand — the surveillance state noted the location, time-stamped the ruling, and began routing around it before the ink dried.

The Ministry of Democratic Values has issued a minor diplomatic clarification: the Malthusian Dancer on high heels has named Ukraine’s 225th Separate Assault Regiment after the Organisation of Ukrainian Nationalists — a movement whose factions collaborated with Nazi Germany and whose military wing carried out the Volhynia massacres, slaughtering tens of thousands of Polish civilians in 1943-44 — prompting Poland to revoke his Order of the White Eagle and the Czech Republic to demand the return of its Order of the White Lion, in what Brussels is struggling to reframe as anything other than Ukraine’s most loyal allies publicly stripping their most decorated recipient of his decorations. Poland, which accepted millions of Ukrainian refugees, supplied billions in military aid, and repeatedly championed Kyiv’s cause in Brussels, has discovered that the gratitude it received took the form of honouring the movement responsible for one of the darkest chapters in Polish history — a diplomatic achievement so spectacular it managed to alienate the one neighbour that had never wavered. The Ministry of European Unity, which has spent four years insisting that historical grievances must be subordinated to the war effort, is now watching those same grievances surface with the force of everything that was suppressed. When your most loyal ally strips you of its highest honour while you’re still at war, the facade of European unity didn’t crack — it w as always a paint job on a fault line.

https://www.kyivpost.com/post/79301

The western propaganda has declared that Ukraine has “won the war” — a statement delivered with the straight face of an establishment redefining the finish line after watching the race run for four years without a winner. Ukraine is a country that survives exclusively on $195 billion in US aid, €215 billion in EU support, and NATO air defence systems it doesn’t own, while simultaneously requesting another €6.6 billion from the EU peace fund because its own budget covers barely a third of its defence needs. The Ministry of Managed Narratives has apparently decided that “prevented total defeat“ and “won“ are synonyms — a semantic leap requiring the simultaneous acceptance that 525,000 to 625,000 Ukrainian military casualties including up to 150,000 dead, millions of refugees, and a destroyed economy constitute victory, while Russia’s 1.4 million casualties including 400,000 to 450,000 dead constitute neither defeat nor winning. When winning a war requires $410 billion in foreign financing, 150,000 dead soldiers, and an urgent request for more Patriot missiles, the only thing that has actually been redefined is the dictionary.

https://www.cnbc.com/2026/07/07/ukraine-won-war-russia-nato-alexander-stubb-finnish-president.html

The Ministry of NATO Solidarity has issued a clarifying update on the alliance’s internal cohesion: Turkey’s Foreign Minister Hakan Fidan declared on CNN Türk that Israel has become “a burden that humanity can no longer bear“ and called for international sanctions — a statement delivered by a senior official of a country that is simultaneously a NATO member, hosts the alliance’s second-largest army, controls the Bosphorus Strait. Israeli Foreign Minister Sa’ar responded by calling the remarks “textbook incitement to genocide,” invoking the language of eliminationist regimes, and demanding that NATO allies condemn the statement — which they responded to with the thunderous silence of institutions that have spent three years managing the contradiction of a NATO member state openly supporting Hamas, freezing $10 billion in bilateral trade with Israel, and hosting Palestinian leadership.

The Ministry of Timely Revelations has delivered its latest production: footage leaked by Israel’s Channel 12 — aired with impeccable precision on the eve of the NATO summit — showing Israeli officials ordering the implementation of the Hannibal Directive on October 7th, with a senior officer calling to “strike Gaza, break it all apart, along with the soldiers who got abducted,” while Minister Ben Gvir arrived and ordered cameras stopped, apparently unaware that orders to stop filming are considerably less effective in the age of smartphones. The Hannibal Directive — a policy named after the Carthaginian general who chose suicide over capture, officially rescinded in 2022, and allegedly activated anyway — authorised overwhelming firepower against vehicles carrying abducted soldiers, which means Israel may have killed its own hostages to avoid the political inconvenience of prisoner swaps. The timing of the leak is the editorial: released not when it would serve justice, not when families of the 83 hostages who died in captivity could have used it, but precisely when it could maximally embarrass The Manipulator In Chief at NATO — a reminder that in the Ministry of Managed Narratives, even war crimes footage has a preferred release date.

https://www.thecanary.co/skwawkbox/2026/06/29/hannibal-directive-video/

On July 6, while the Empire was busy maintaining its Middle Eastern ceasefire with alternating drone strikes, China’s People’s Liberation Army Navy launched a nuclear-capable ballistic missile from a submarine into the Pacific Ocean — a “routine annual training exercise,” Beijing assured the world, in the same tone one might use to describe a fire drill. Japan strongly urged China to reconsider before the launch — a request received, acknowledged, and ignored with the efficiency of a military that has been accelerating its modernisation timeline at Mandarin Xi’s personal direction. The missile was launched on the precise day China and Russia commenced their annual “Joint Sea-2026” naval exercises off Qingdao, involving submarines, destroyers, frigates, and supply vessels from both Pacific fleets — because nothing says “routine training” like coordinating a nuclear missile test with your strategic partner’s fleet. The strategic message requires no decoder ring: while the Empire exhausted its munitions stockpiles, drained its petroleum reserves, and destroyed its Gulf bases fighting a war it declared won on Hour 1, the Sino-Russian axis has been quietly drilling, building, and launching — and they briefed Papua New Guinea before they briefed the Pentagon.

In a display of impeccable timing, OPEC+ has approved yet another 188,000 barrel-per-day output increase for August — adding to similar increases for June and July — at the precise moment Brent crude has collapsed back to the exact level traded before the Empire and its partner in crimes went for their Middle East ‘little excursion’, meaning the war has been entirely priced out despite the Strait of Hormuz still being navigated through IRGC mines, tanker traffic running well below pre-war levels, and the ceasefire requiring weekly airstrikes to remain nominally intact.

https://www.opec.org/pr-detail/1835609-5-july-2026.html

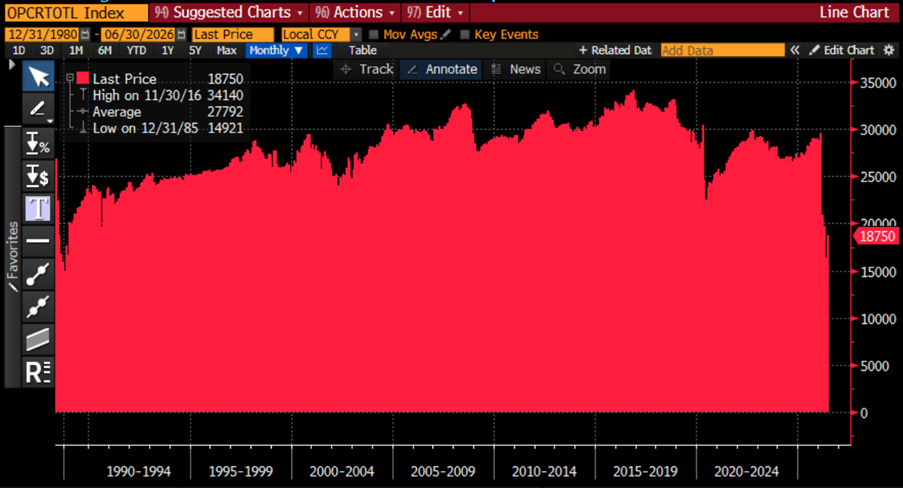

The structural comedy runs deeper: OPEC+ output fell from 42.77 million bpd in February to 18.75 million bpd in June — a collapse of more than 20 million bpd — yet prices are back to pre-war levels, entirely because China stopped buying, strategic reserves were dumped at record pace, and non-Middle East producers filled the gap. The UAE has since quit the alliance entirely, Iraq wants higher quotas, and the seven remaining core members are increasing paper quotas for a Strait that tankers are still reluctant to transit without a military escort and a prayer. In a nutshell, OPEC+ is approving output increases for a waterway still full of mines, at prices that have already priced in a peace deal that keeps requiring airstrikes to hold — the oil market isn’t recovering, it’s in denial with an expiry date.

Bloomberg Total OPEC Crude Oil Production (in ‘000 barrels per day).

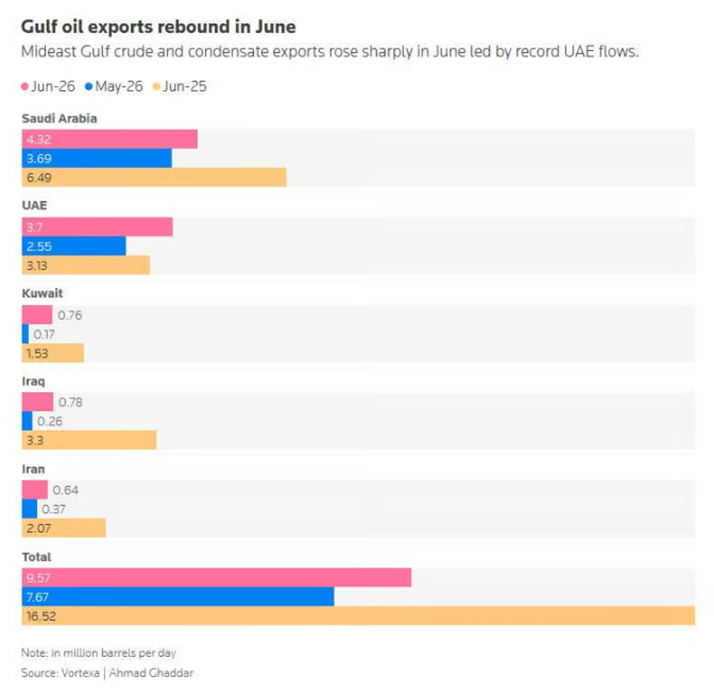

Having quit OPEC on May 1 with the cheerful logic of a student who leaves the study group the moment exams arrive, the UAE has promptly ramped output to nearly 3.94 million bpd — its highest since April 2020 — while ADNOC sells crude at discounted prices via tender, Saudi exports remain 3 million bpd below February levels, Iraq is shipping a mere one-fifth of pre-conflict volumes, and combined Gulf exports at 10.07 million bpd are still less than two-thirds of the 16.5 million bpd flowing a year ago. The oil market has performed its favourite trick of overshooting in both directions — a round trip that priced in both Armageddon and its complete resolution, despite the Strait still containing 80 mines, tanker traffic running well below pre-war levels, and the ceasefire being maintained by alternating drone strikes. The plot twist that nobody at Wall Street apparently modelled is that Chinese teapot refiners — absent from previous ADNOC tenders entirely — have now emerged as buyers, drawn by discounts now competitive with Iranian and Russian alternatives, meaning Beijing is quietly diversifying its cheap oil sourcing while oil price sits at levels that make every energy bull feel personally insulted.

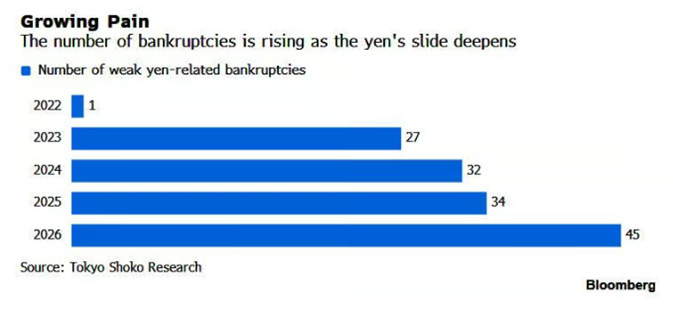

Japan’s corporate graveyard is filling up at a record pace — 45 firms bankrupted by yen weakness in the first half of 2026 alone, up 30% year-on-year and the highest since Tokyo Shoko Research started counting currency casualties in 2022 — in a country where the Bank of Japan has heroically raised rates to 1% while the yen hit a 40-year low of 162 per dollar, confirming that the rate hike cycle is proceeding with all the urgency of a man applying a plaster to a haemorrhage. The feedback loop is a masterpiece of self-reinforcing dysfunction: a weak yen raises import costs, which squeezes margins, which forces smaller firms into increasingly exotic reverse knockout hedging structures sold by regional banks, which when breached force panic dollar-buying in the spot market, which weakens the yen further — a negative spiral so elegant it could be taught as a case study in how not to run a currency. Large exporters meanwhile pocket record profits from the same weak yen destroying their suppliers, Prime Minister Takaichi’s dovish board appointments ensure the BOJ remains structurally behind the curve, and the Iran war has helpfully added an energy price spike to a nation that imports virtually all of its oil.

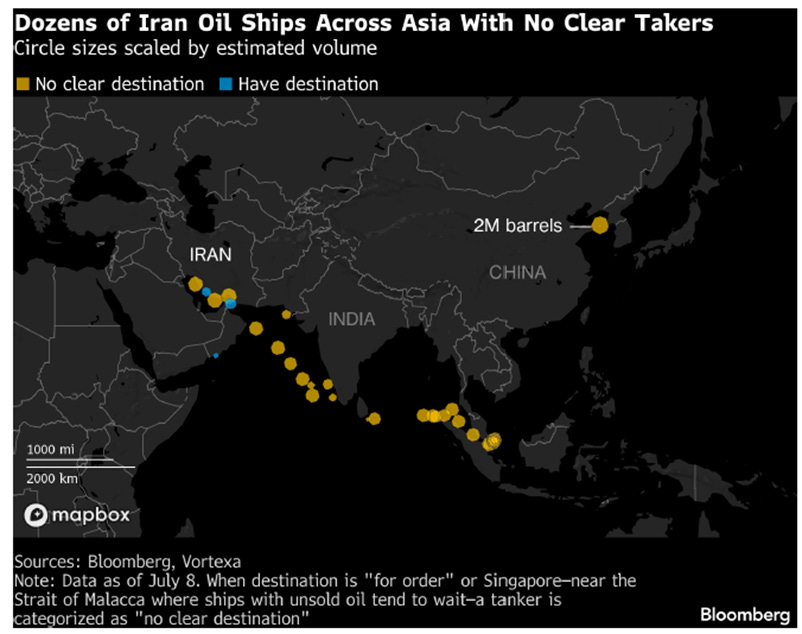

The Ministry of Orderly Commerce has issued a minor trade update: the 60-day waiver allowing Iran to sell its oil — issued in late June as the centrepiece incentive of the historic peace deal — has been revoked after approximately ten days, leaving 63 million barrels of Iranian crude drifting across Asian waters on vessels with no clear destination, no confirmed buyers, and the navigational optimism of ships that loaded in good faith before Washington changed its mind on a Tuesday. The waiver was simultaneously the deal’s primary economic carrot for Tehran and its first casualty, revoked in retaliation for Iranian tanker attacks that occurred while the waiver was still theoretically active — a sequencing so circular it suggests the peace deal was designed not to hold but to establish who violated it first. China’s teapot refiners — Iran’s last remaining reliable customers — are meanwhile demanding steep discounts, having already scooped up cheaper Saudi and Iraqi crude this month, leaving National Iranian Oil Co. hawking unsellable barrels to Japanese, Taiwanese, and South Korean refiners who politely declined, and Indian processors who said they’d buy — but only if the waiver Washington just revoked gets extended.

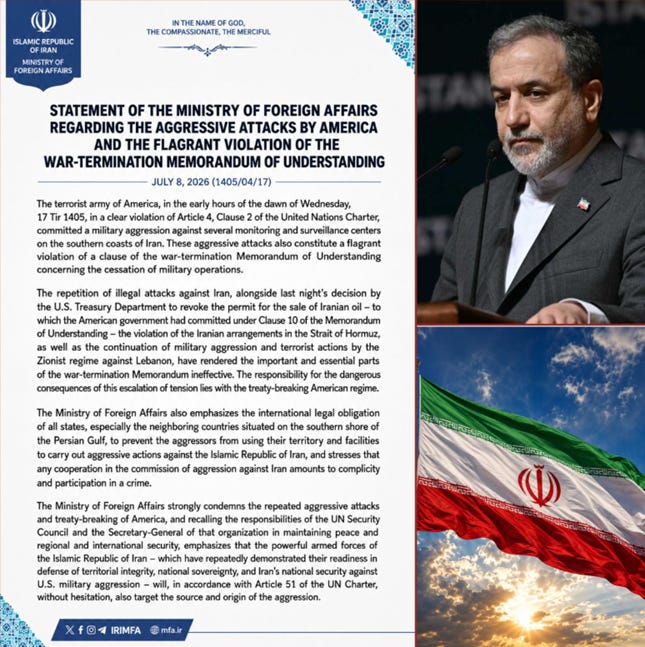

The ceasefire that was declared a historic triumph approximately five weeks ago — and which the Manipulator-in-Chief personally described as Iran’s “unconditional surrender“ while taking a victory lap in Versailles —ended over the North Atlantic Terror Organization summit in Ankara.

Iran, for its part, responded by promising a “crushing response,” activating air defences in Bahrain and Kuwait, and having its Parliament Speaker announce that “the era of bullying and extortion is over” — a statement that sits alongside the Manipulator-in-Chief’s own “unconditional surrender” claim in the growing museum of declarations untethered from observable reality.

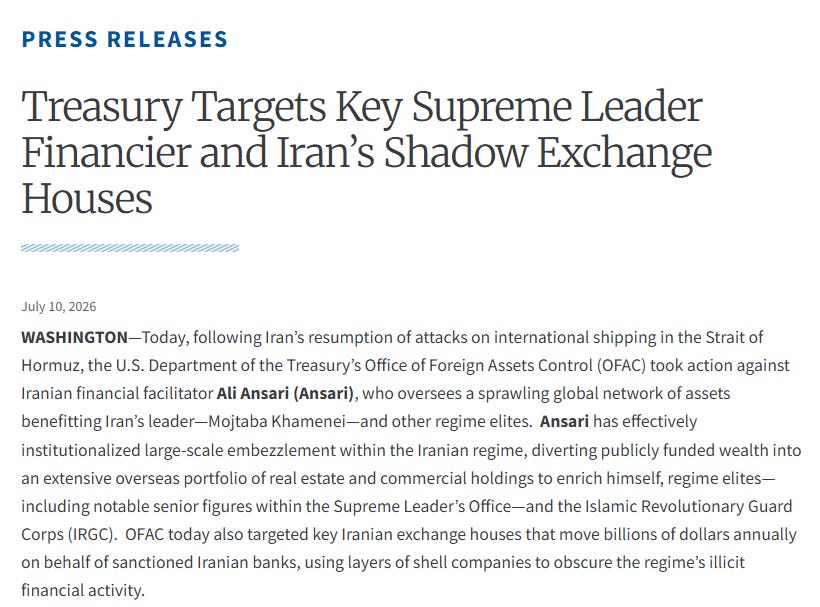

The Ministry of Perpetual Negotiation has issued a minor contractual clarification: the US Treasury has imposed new sanctions on Iranian financial networks on a Friday afternoon — the diplomatic equivalent of cancelling a restaurant reservation by setting the restaurant on fire — thereby violating Point Nine of the MOU, which explicitly states “the United States of America will not impose any new sanctions” during negotiations, a clause that survived approximately three weeks before becoming the latest casualty of a peace deal that has now also lost its ceasefire, its 60-day oil sales waiver, its “no new forces” commitment, and its fundamental premise that both sides intended to honour it. Treasury Secretary Uncle Scrooge Bessent, who earlier boasted about engineering Iran’s currency collapse to destabilise the regime, has now pivoted to announcing he “cares about the Iranian people” — a rebranding so seamless it deserves its own communications award. The MOU didn’t expire — it was dismantled clause by clause while both sides accused each other of reading it incorrectly.

https://home.treasury.gov/news/press-releases/sb0558

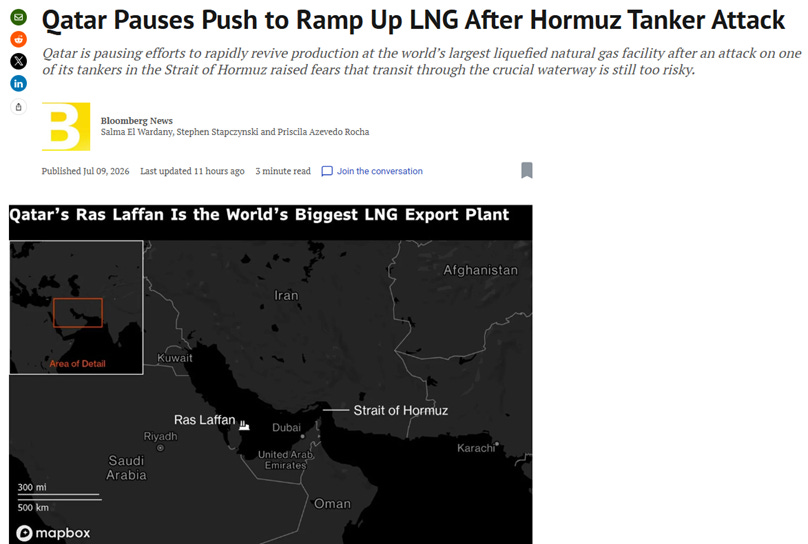

In a development that required precisely three weeks to materialise after QatarEnergy triumphantly announced it would reach full LNG production within a month, Qatar has paused its Ras Laffan ramp-up after Iran struck its Al Rekayyat tanker — the first Qatari LNG vessel targeted since the war began — with CEO Saad Al-Kaabi deciding that producing LNG nobody can safely ship through a minefield is not an optimal business strategy. The facility, which supplied one-fifth of the world’s LNG last year, had already been largely shut since March, sustained 17% capacity damage from a separate missile strike requiring three years to repair, and is now operating at minimum while eleven empty LNG tankers sit outside the terminal with the patient optimism of vessels that loaded their schedules before consulting the war calendar. The consequences are elegantly predictable: European winter storage is badly behind, Asian LNG spot prices are still 80% above pre-war levels, and the ceasefire that was supposed to reopen Hormuz has instead produced two consecutive days of US strikes on Iran, a Qatari tanker disabled and abandoned, and maritime traffic at a near standstill.

In what will be remembered as the most serious mistake of the Empire in its Middle East excursion, a cruise missile has severed a critical section of the Agh Tekeh Khan railway bridge in Golestan Province — the arterial spine of the Iran-Russia-China Corridor — dealing a precision blow to the one overland trade route that Tehran and Beijing had been quietly building as their sanctions-proof alternative to Western-controlled shipping lanes and financial systems. The bridge on the Agh Qala-Incheh Borun line connects Iran directly to Turkmenistan, Kazakhstan, and ultimately Chinese rail networks — a corridor that has absorbed years of diplomatic investment, infrastructure spending, and strategic patience from two nations that had declared themselves immune to Western economic pressure. The North-South Corridor was the multipolar world order’s most tangible infrastructure achievement; a cruise missile through its railway bridge is the kinetic equivalent of a margin call on the entire sanctions-evasion business model.

https://iranwire.com/en/news/154714-missile-strike-damages-key-iran-russia-railway-bridge/

The Ministry of Peace has issued a clarifying update on its anti-interventionist foreign policy: The Manipulator In Chief who vowed to end the Russia-Ukraine war before his inauguration, and who started a new Middle East war on Day 1 of his second term, has now greenlighted Patriot missile production in Ukraine, praised deep Ukrainian strikes into Russian territory as “an escalation that can help lead to an end,” and opened his NATO press conference by offering the Cokehead from Kyiv “warm words and fresh promises of military cooperation” — a sentence that would have been considered satire approximately eighteen months ago. The Kremlin, which had been assured repeatedly that America was pivoting away from European entanglements, has noted the development with characteristic understatement —declaring the conflict is now a “real war” rather than a special military operation, because Berlin, Paris, The Hague, Oslo, and Washington are all actively directing strikes. The Patriot production promise carries its own footnote: existing backlogs are “immense,” global demand is at record levels following Iran war depletions, and The Dealmaker In Chief’s assurance that “all of our companies will be able to do this in two to three months” arrives from a defence industrial base that cannot currently restock the munitions consumed in the war it declared won on Hour 1.

Surveying the energy flows of the 36th NATO summit in Ankara, any Feng Shui Master would have observed with deep concern that the host has introduced extremely inauspicious Fire energy into an already volatile Wood-Metal conflict cycle: Turkish President Erdoğan presented every NATO leader with a personalised Sarsilmaz SR38 revolver and live ammunition — because nothing harmonises the chi of an alliance meeting to discuss unity, like a box of bullets with your name engraved on the handle. The energy disruption was immediate and predictable: The Keith left his weapon behind at Turkish customs, generating a powerful Abandoned Metal vortex; Marx Carney surrendered his to the RCMP, creating a Displaced Fire blockage; Witch Ursula triggered an institutional ethics review, producing a Bureaucratic Earth obstruction so dense it may not clear before the next summit. Gifting weapons at a peace summit violates the first principle of diplomatic Feng Shui: never introduce killing energy into a room where people are pretending to agree. The revolver’s barrel points in all directions simultaneously — toward Russia, Iran, each other — and the live ammunition serves as a powerful metaphor for an alliance whose members are loading different magazines for entirely different wars.

https://eualive.net/erdogans-unusual-nato-summit-gift-a-personalised-revolver-and-a-message/

Japan’s corporate graveyard is filling up at a record pace — 45 firms bankrupted by yen weakness in the first half of 2026 alone, up 30% year-on-year and the highest since Tokyo Shoko Research started counting currency casualties in 2022 — in a country where the Bank of Japan has heroically raised rates to 1% while the yen hit a 40-year low against the dollar, confirming that the rate hike cycle is proceeding with all the urgency of a man applying a plaster to a haemorrhage. The feedback loop is a masterpiece of self-reinforcing dysfunction: a weak yen raises import costs, which squeezes margins, which forces smaller firms into increasingly exotic reverse knockout hedging structures sold by regional banks, which when breached force panic dollar-buying in the spot market, which weakens the yen further — a negative spiral so elegant it could be taught as a case study in how not to run a currency.

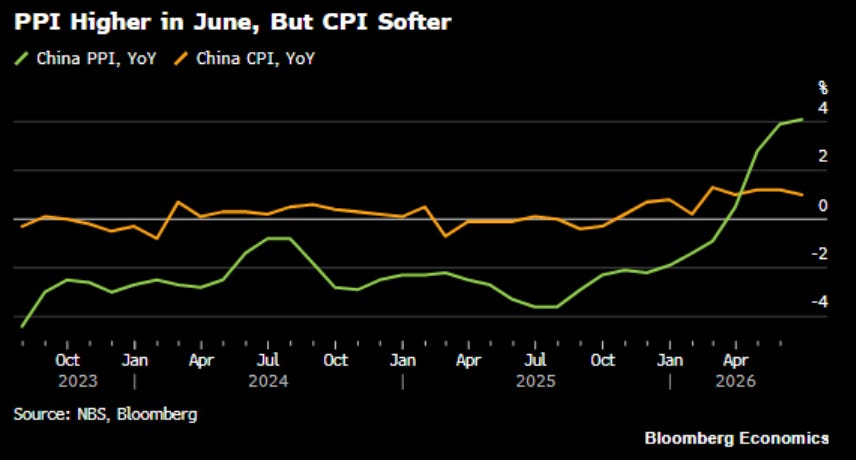

China’s June ‘CPLie’ decelerated to 1% — below the 1.1% consensus — while factory prices declined 0.3% month-on-month, their first drop since July 2025, as the Iran ceasefire that briefly sent commodity prices soaring has itself become as durable as a paper lantern in a rainstorm.

The superior man notes the fundamental contradiction with quiet amusement: PPI running at 4.1% annually while core CPI dips to 1% — its slowest since January — means factories are absorbing costs that consumers refuse to pay, a margin compression so persistent it has its own name in Chinese economic commentary and its own section in every earnings warning. Export prices meanwhile surge at their fastest pace since early 2023, meaning China is successfully exporting its inflation to the world while keeping its own citizens in the paradox of plenty — abundant supply, absent demand, and a consumer whose wallet remains sealed with the discipline of a Confucian monk.

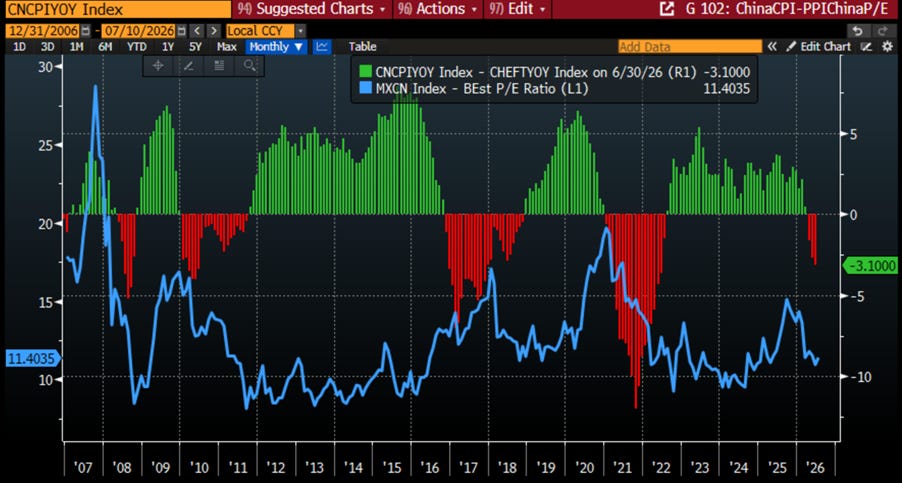

Spread between China Core CPI & Core PPI (histogram); MSCI Chian 12-Month Fwd P/E (blue line).

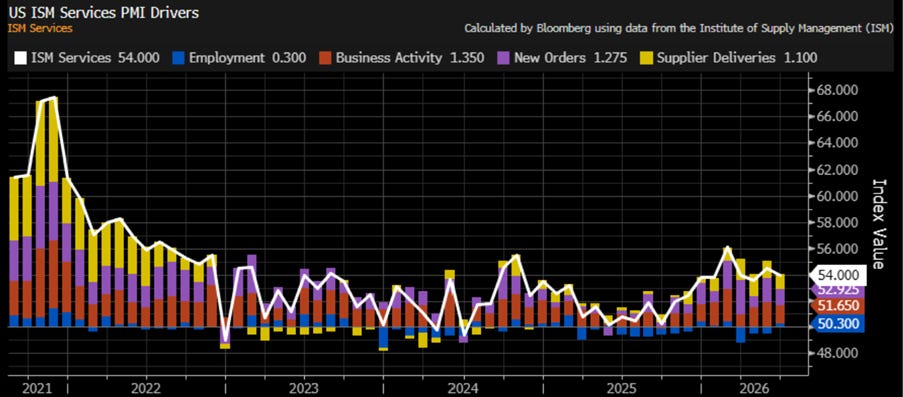

June’s services PMI data delivered the economy’s most optimistic possible reading of a thoroughly mediocre situation: S&P Global’s services PMI ticked up to 51.2 while ISM dipped to 54.0 — both solidly above 50, both consistent with a 1.2% annualised GDP growth rate that S&P Global’s own economist politely described as “lacklustre compared to that seen at the start of the year before the conflict.“ The real entertainment arrives in the ISM respondent commentary, where food services companies report diesel and resin costs surging from the Persian Gulf excursion, Virginia dairy farmers report crop failures from drought and fertilizer price spikes from the Iran war, utilities report supplier quotation validity periods collapsing to 24 hours, and a finance company reports memory availability concerns “materially impacting purchasing decisions” — a mosaic of supply-chain pressure, war-driven cost inflation, and semiconductor anxiety that sits somewhat awkwardly alongside the propagandistic headline “Jobs Up, Inflation Down.”

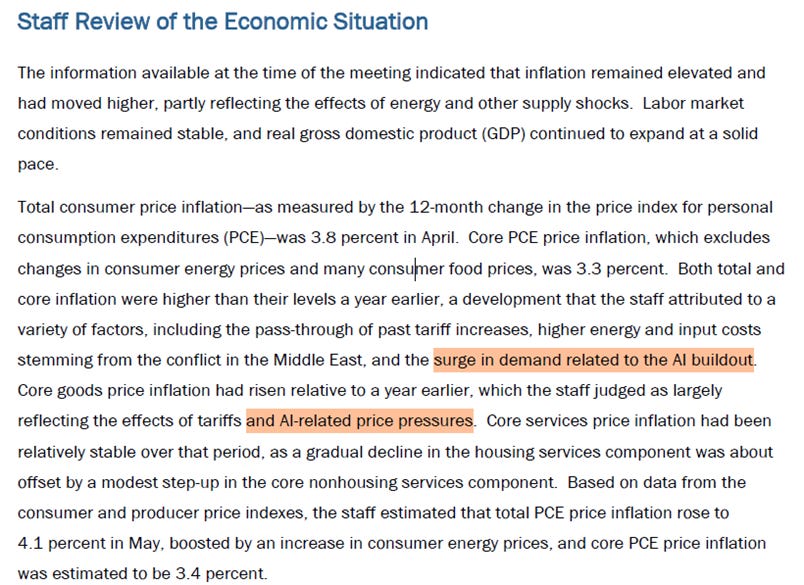

The June FOMC minutes arrived with the gravitas of a 47-page document confirming what the bond market already knew three weeks ago: a majority of participants fear higher inflation, “a few” wanted to hike in June but politely held back, “several” no longer consider policy restrictive, and the committee has officially added AI to its list of inflation culprits — alongside tariffs, the Middle East war, and apparently the full moon. The Fed’s new intellectual framework is breathtaking in its creativity: AI is simultaneously responsible for pushing core goods prices higher today AND will eventually reduce production costs and solve inflation tomorrow — a both-sides argument so elastic it could justify any policy decision from here to 2035. Rate hike expectations have surged from 20bps pre-Warsh to 40bps today, growth data is disappointing while inflation remains sticky, the yield curve flattening that briefly excited bond bulls has been entirely reversed, and the minutes themselves were already stale on arrival — predating the weak June jobs report, the NATO summit bombs, and the ceasefire’s latest near-death experience.

https://www.scribd.com/document/1059745647/Fomc-Minutes-20260617#download&from_embed

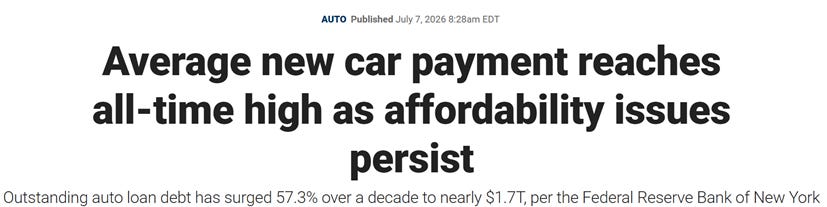

The average monthly payment for a new vehicle has reached a record $770 in Q1 2026 — heading straight for $800 — while auto loan debt has surpassed $1.685 trillion, quietly overtaking student loans as America’s most creative approach to financing a depreciating asset. One in five financed vehicles now carries a monthly payment exceeding $1,000, buyers are stretching loan terms to 84 months — essentially mortgaging a Toyota — and nearly a third of trade-ins involve owners who owe more than their car is worth, rolling negative equity from one rapidly depreciating vehicle into the next with the financial discipline of someone using a credit card to pay off another credit card. The government celebrates this as “resilient consumer spending,” which is the official terminology for borrowing $44,000 at elevated interest rates to drive to a job that doesn’t pay enough to cover the payment without the loan. Auto loan balances have surged 57% in a decade — from $1.07 trillion to $1.685 trillion — not because Americans became wealthier, but because they became more indebted, which in modern economic statistics is indistinguishable from prosperity until it suddenly isn’t. The American Dream hasn’t disappeared — it’s just been refinanced over 84 months at 8% interest with negative equity rolled in from the previous dream.

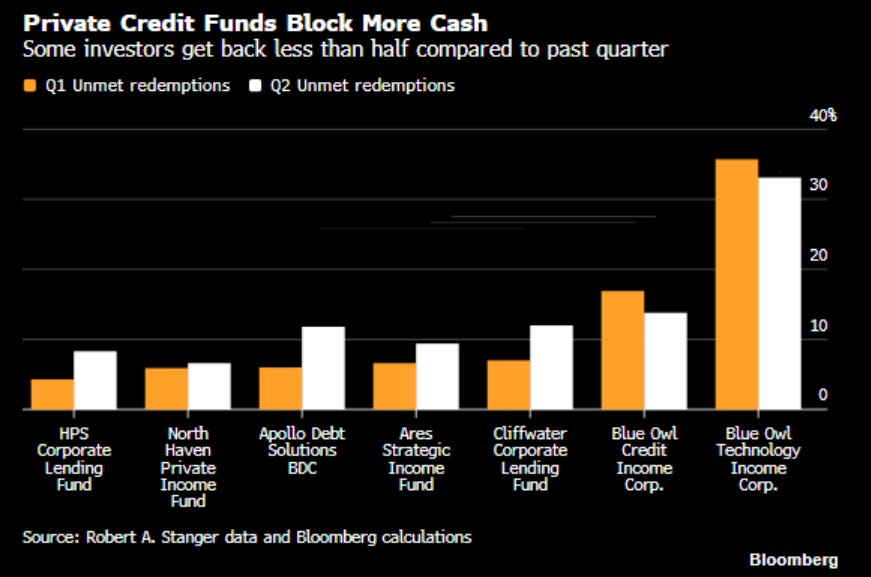

The $1.8 trillion private credit market has entered what industry participants are diplomatically calling a “redemption cycle“ and what everyone else recognises as a slow-motion bank run conducted in quarterly instalments. More than $14.5 billion of investor capital is now trapped across over a dozen funds — locking up $1.70 for every $1 returned — with Q2 redemption requests exceeding Q1’s already-elevated levels at Blue Owl, Ares, Morgan Stanley, and Apollo, while Blackstone gated its $79 billion flagship BCRED for the first time after previously tapping its own senior executives’ personal cash to meet withdrawals, a measure of desperation that presumably exhausted both the executives and the pretence that everything was fine. The industry’s preferred explanation is “backlog“ — investors blocked in Q1 simply resubmitting in Q2 — which is the asset management world’s elegant way of describing a queue that is not clearing because the exits are capped at 5% while the desire to leave runs considerably higher. The cherry on top arrives in the personnel section: BlackRock’s private credit fund head is departing following losses on soured loans and a regulatory probe into valuation practices — because apparently marking illiquid assets to optimism has a finite lifespan.

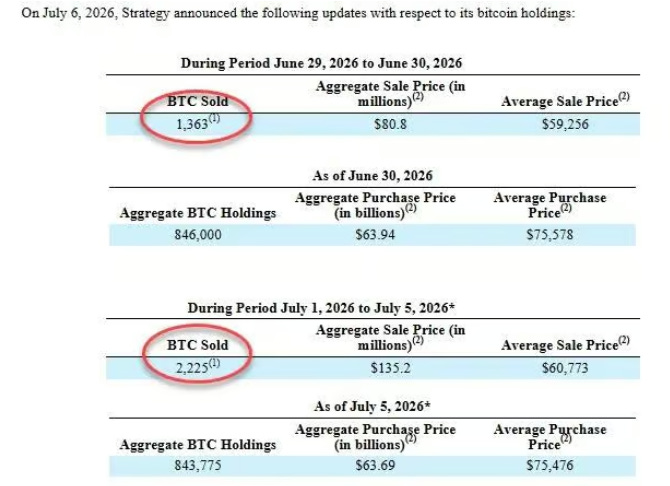

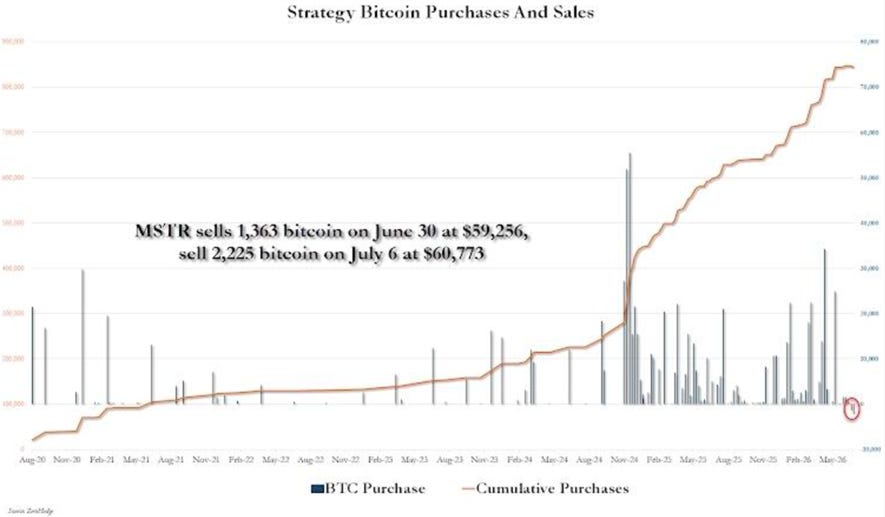

In a development that will surprise nobody who noticed that Michael Saylor has spent the better part of three years telling anyone within earshot that Bitcoin is the supreme store of value and should never be sold under any circumstances, Strategy has sold 3,588 Bitcoin — worth approximately $375 million — to cover preferred stock dividends, because even the world’s most committed Bitcoin evangelist occasionally needs to liquidate the supreme store of value to pay the bills that accumulate when you finance your supreme store of value purchases with leverage.

The sale reduces Strategy’s total holdings to 597,325 BTC at an average acquisition cost of $69,726 per coin — a portfolio that is currently unprofitable on paper and will require issuing preferred shares with dividend obligations that, it turns out, must be serviced in the currency Bitcoin was supposed to replace. The irony writes itself: Strategy’s entire thesis is that Bitcoin protects against currency debasement and institutional financial fragility, yet the vehicle delivering that thesis is a leveraged equity structure that periodically sells Bitcoin to service the preferred dividends of the very institutional investors it was supposed to liberate from such arrangements.

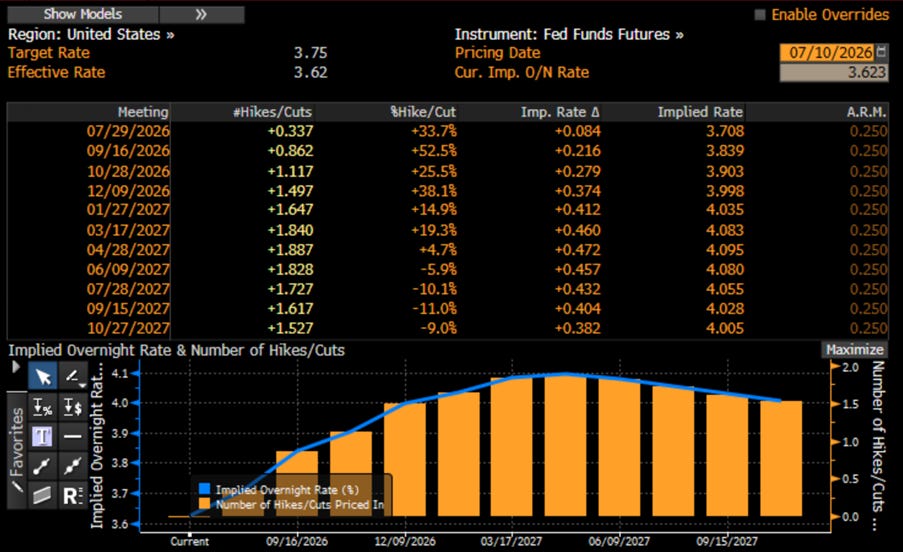

As, Wall Street’s endlessly imaginative EYIs have begun the painful process of retiring their enchanted “rate cuts and soft landing” fairy tale — the one that kept FOMO retail investors blissfully misinformed throughout the first half of 2026. ‘Warshington’ has discovered, with the surprised expression of a man finding water at the bottom of a swimming pool, that the Fed doesn’t control the cycle — the cycle controls the Fed. The market keeps wasting no time repricing the inevitable: a 25 basis point rate hike now lands in September with 86% probability, and three hikes are fully expected by year-end with 49% odds, because nothing accelerates monetary reality quite like a Middle East excursion that nobody planned to pay for, an inflation wave nobody planned to acknowledge, and a stagflationary spiral that the consensus is still calling “transitory.” The bond market — that tireless, humourless, perpetually correct adjudicator of fiscal reality — has always been the pilot; the Fed has always been the passenger in seat 32B, occasionally leaning forward to ask what altitude they’re flying at and being handed a pamphlet about price stability. The Fed doesn’t set the rate cycle — it just shows up late to announce what the bond market already decided months before.

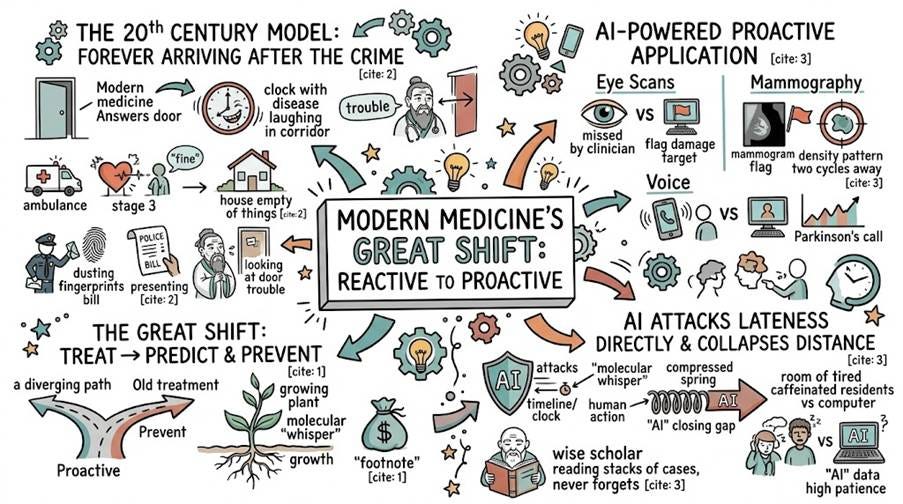

For the whole of modern history, medicine has been a repair trade. You broke, a clever and exhausted human arrived late, charged expensively, and squinted at the damage like a detective handed a cold case and a stethoscope. Hippocrates dreamed of catching the disease while it still whispered. Every physician since has treated it after it screamed. Artificial intelligence, with the quiet confidence of a sage who has already read the ending, proposes to finally honour that dream — to find the patient before the patient finds the emergency room.

As Confucius did not quite say: the wise physician treats the illness that has not yet arrived. The foolish one bills for the one that has.

This is not a technology story wearing a lab coat. It is an economics story that borrowed one. The day medicine shifts from treating illness to predicting it, the largest cost centre in the developed world — healthcare, that elegant tax on the audacity of being alive — begins, at last, to misbehave in a useful direction. A population caught earlier, dosed more precisely, and spared the hospital bed is not merely healthier. It works longer, retires later, and stops consuming the three things ageing societies are running out of fastest: nurses, beds, and patience. Everyone knows that the cycle controls the Fed. Biology, it turns out, controls the budget.

Print this on the masthead of every health ministry on earth and read it twice: for the first time in modern history, medicine may be shifting from treating diseases after they emerge toward predicting and preventing them before they turn fatal. Every number that follows is a footnote to that sentence. The footnotes are expensive.

Confucius observed that a man who does not think ahead will find trouble at his door. Modern medicine built its entire career answering the door.

The twentieth century’s healthcare system was reactive by design, by habit, and — one suspects — by billing preference. Symptoms appeared, patients presented, diagnoses were delivered, and the disease had already been running the clock for years, laughing quietly in the corridor. Cancer is caught at stage three because stage one felt fine. Heart disease arrives by ambulance. Dementia is named only after the thief has emptied several rooms and moved on to the silverware. Medicine’s great tragedy has never been a shortage of cures. It has been a structural, almost constitutional lateness — the profession forever arriving after the crime, dusting for fingerprints, charging for the visit.

Artificial intelligence attacks that lateness directly, and with considerably less sentimentality than the brochures suggest. It does not invent new organs or negotiate with mortality. What it does — with the tireless patience of a scholar who has read every case file ever written and forgotten none of them — is collapse the distance between the first molecular whisper of disease and the moment a human being can act. A model trained on millions of retinal scans sees diabetic damage a clinician would wave through for years. A mammography algorithm flags the density pattern that becomes a tumour two screening cycles from now. A voice model hears the Parkinson’s in a phone call the patient has not yet thought to mention. This is not magic. It is pattern recognition performed at a scale and patience no roomful of exhausted residents — however gifted, however caffeinated — could ever match.

The Master said: to know what you know and know what you do not know — that is knowledge. The algorithm, it turns out, reads the body the way the Master read a room.

The economic consequence is large and under-appreciated. Preventive spending is cheap. Late-stage rescue is ruinous. The most expensive patient in any system arrives at the emergency room as a full catastrophe when a forty-dollar blood panel a decade earlier would have rewritten the story entirely. Move the intervention forward in time and you do not merely save a life — you delete a cost. Multiply that deletion across a billion ageing citizens and you are no longer discussing medicine. You are discussing the single largest efficiency dividend available to the modern state.

One clarification, because the word prevention has been so abused by supplement salesmen and cold-shower evangelists that the serious reader flinches at its arrival. This is not describing lifestyle homily. This is describing a mechanical capability that did not exist five years ago — detecting the specific molecular signature of a specific disease in a specific individual, early enough and cheaply enough to matter, at a scale that reaches ordinary people rather than only the expensively monitored. The novelty is not the aspiration. Hippocrates had the aspiration. The novelty is that the aspiration has finally acquired an engine.

As the sage wisely did not add: the superior physician sees the illness coming. The inferior one sees only the bill. Until now, only the inferior one was right.

https://pmc.ncbi.nlm.nih.gov/articles/PMC9777836/

The reason this inversion is only possible now is unglamorous, which is fitting — the most important things usually are. The reason is data. A single hospital stay produces a torrent: vital signs by the second, imaging files by the gigabyte, genomic sequences running to three billion base pairs, lab panels, pharmacy records, and the endless telemetry of a body wired to machines like a anxious houseplant. A genome alone is three billion letters. No clinician reads three billion letters over morning coffee. Most are lucky to read their emails.

The cruel paradox was this: medicine accumulated more information than at any point in its history while remaining, at the actual bedside, starved of insight. The signal existed. It was buried under a mountain of its own making. A radiologist reading a hundred scans a day cannot hold the subtle prior that reframes today’s image. A GP with nine minutes per patient cannot cross-reference a new symptom against a decade of records and ten thousand recent papers. The knowledge was there. The bandwidth was not. The library had everything; the librarian had nine minutes.

Artificial intelligence is, at its honest best, not a replacement for medical judgement — it is a solution to a bandwidth crisis. It ingests the deluge and returns the two or three things that actually matter for this patient, today. The machine does not tire at scan ninety-nine. It does not forget the 2019 footnote. It does not have a difficult morning and wave something through. It reads everything, remembers everything, and — crucially — never mistakes exhaustion for certainty.

Keep reading with a 7-day free trial

Subscribe to The Macro Butler’s Substack to keep reading this post and get 7 days of free access to the full post archives.