Deep Thinking Through A Stargate

THE WEEK THAT IT WAS...

The first week of the second month of the jubilee year once again brought investors’ focus to U.S. Manufacturing and Non-Manufacturing ISM data, as well as the January Non-Farm Payroll report. It also marked the second leg of earnings season for the Magnificent 7, with Alphabet and Amazon reporting alongside 126 other S&P 500 companies.

Probably still influenced by the optimism surrounding a new administration and a new year, the ISM Manufacturing Index rose into expansion for the first time since September 2022, reaching 50.9, beating expectations of 49.9 and the prior reading of 49.2. All underlying components increased, with Prices Paid at their highest since May 2024, New Orders at their highest since May 2022, and Employment returning to expansion for the first time since May 2024.

A new year and a new president have brought renewed optimism to the U.S. manufacturing sector. Over the past decade, only two months, during the post-pandemic reopening, have seen business sentiment improve as sharply as in January. While this signals confidence in the U.S. economy, the ISM Manufacturing Index also underscores that inflation remains sticky. Time will tell if this wave of optimism holds as tariffs and trade wars take centre stage in the new presidency, while monetary illusion continues to spread.

After the unexpected surge in the ISM Manufacturing Index, the US ISM Services Index expanded more slowly in January as frigid weather forced some warehouses to close. Businesses remained uncertain whether customer demand was driven by underlying business dynamics or merely panic buying ahead of tariffs. Within the ISM Services Index, new orders weakened dramatically, inflation declined but remained elevated, and employment improved modestly.

In a nutshell, the ISM January data reinforced the trend seen since the November 5th election—manufacturing sentiment has been improving, while services sentiment has deteriorated following the confirmation of ‘The Donald’s return to the White House.

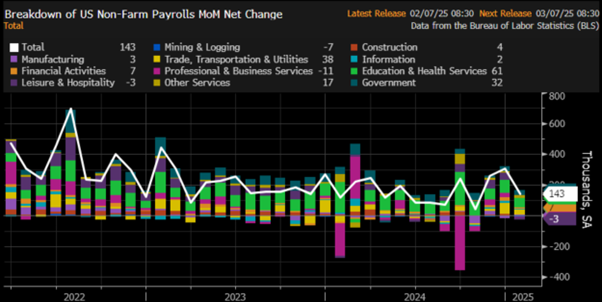

The January Non-Farm Payroll report revealed that the U.S. economy added 143K jobs, significantly below the forecasted 175K and the lowest monthly job creation since last October. Despite the era of DOGE being hyped by the new propagandistic mass media, the government, along with education and health services, remained the main contributor to job creation in January, while mining, leisure, and hospitality shed jobs over the past month.

Average hourly earnings accelerated from +0.3% MoM to +0.5%, reaching +4.1% YoY, signalling that wage reflation is back on the agenda for U.S. entrepreneurs even before tighter immigration rules take effect. The unemployment rate fell to 4.0%, beating expectations of 4.1%, but remains above its 24-month moving average, a historical precursor to economic downturns within 12–24 months.

Upper Panel: US Unemployment Rate (blue line); US Unemployment 24 months moving average (green line); Lower Panel: S&P 500 to WTI ratio (yellow line); US S&P 500 to WTI Ratio 84 months moving average (red line).

In an increasingly polarized country, with tariff-related Executive Order threats like ‘pigs in the air with their tails forward’, it's no surprise that consumer sentiment deteriorated further in early February. Year-ahead inflation expectations surged to 4.3% (vs. 3.3% prior), the highest since November 2023 and well above the 2.3%-3.0% pre-pandemic range. Long-run inflation expectations edged up slightly to 3.3% (vs. 3.2% prior). Concern over tariffs also grew, with about one-third of consumers mentioning them spontaneously, up from 27% last month and less than 2% before the election.

In this context, while the new Treasury Secretary seeks to mediate between the 47th U.S. president and the Fed chairman, Wall Street bankers and their parrots continue to delude themselves into believing the increasingly impotent FED will keep cutting rates, even as the president enacts tariffs and tighter immigration policies that will fuel stagflation. While the FED's dot plots still project two rate cuts this year, consensus assigns a 43% probability, with the first now pushed back from June to July or even September, and the second in December. This timeline extends well past the first 100 days of the new presidency, by which point the U.S. economy will likely be in an inflationary bust, potentially forcing the Fed to raise rates if it remains committed to fighting inflation for the benefit of American citizens.

In an increasingly polarized and interconnected world, investors who analyse the health of the economy and financial markets through the lens of the business cycle have already understood that a healthy economy relies not only on an abundant and cheap source of energy but also on access to data, especially in a world where data is increasingly seen as the new oil.

With Trump’s return to the Oval Office, investors will recall how his first term escalated the U.S.-China rivalry from a trade war to a tech war. The 2018 arrest of Huawei CFO Meng Wanzhou and the U.S. ban on high-end semiconductor exports to China underscored Washington’s belief in its technological edge. By 2021, Commerce Secretary Gina Raimondo sought European support to curb China’s innovation, dragging European firms—especially ASML—into an unwanted tech cold war. Since then, China has surged ahead in 5G, high-speed rail, EVs, batteries, and drones, prompting fresh trade barriers in the West. Yet many investors, swayed by political and media narratives, overlook a crucial fact: China now graduates more STEM students annually than the rest of the world combined. Betting against China’s technological rise is therefore short-sighted.

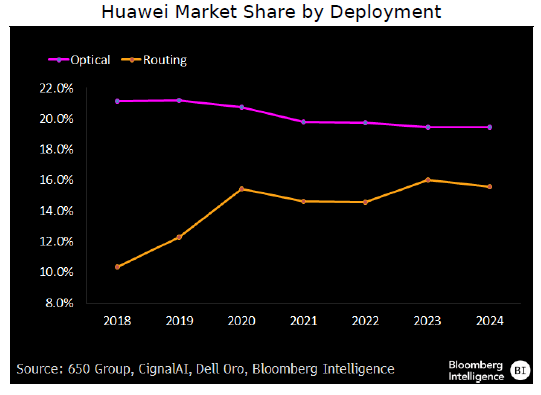

Indeed, the Western propagandistic narrative of Huawei’s demise was more than premature. U.S. sanctions have not generated the expected boost in routing and optical sales for Cisco, Juniper, Ciena, and Nokia, and this dynamic is unlikely to change under the Trump administration implementing more sanctions. Huawei's global market share outside China has remained steady at 19–20% in optical and 15–16% in service-provider routing, with modest gains in Europe, suggesting that sanctions and security concerns have had little impact on sales. This stability indicates that Huawei’s ability to develop and access advanced optical and routing chips has not been significantly affected. While the company may lack access to the latest-generation process nodes for these chips, it appears to have sufficient components to serve a broad segment of the market.

On January 25, 2025, the Western world, still clinging to its illusion of dominance over the Global South, was shaken by the emergence of DeepSeek, a large language model (LLM) reportedly cheaper and better than the now-iconic ChatGPT and other AI models from the so-called Magnificent 7. This revelation challenged two key market assumptions since ChatGPT’s launch in November 2022: first, that competing in AI requires massive, energy-intensive spending, and second, that Nvidia’s dominance in AI chips is unassailable. While U.S.-China tensions may slow AI advances, others stand to benefit. Nvidia’s 50%+ profit margins—unmatched even by past tech giants like Apple and Cisco—highlight the opportunity for disruption. Capitalism should naturally drive competition to claim a share of those margins, and DeepSeek may be the first major challenger. Beyond exposing Washington’s futile attempts to stifle China’s tech rise, DeepSeek suggests AI development may be far less costly than previously thought. This could accelerate innovation while prompting CFOs to scrutinize the massive AI-related spending. The four major hyperscalers spent an estimated $222 billion on AI last year, and Meta alone expects to spend $60–65 billion in 2025—far exceeding prior analyst forecasts.

First and foremost, investors must understand that AI is not new, it has been evolving slowly for decades. The recent frenzy began only after OpenAI released its large language model (LLM), the generative AI software ChatGPT, two years ago. To grasp the magnitude of the Magnificent 7’s rise, their combined market capitalization now exceeds that of most major economies.

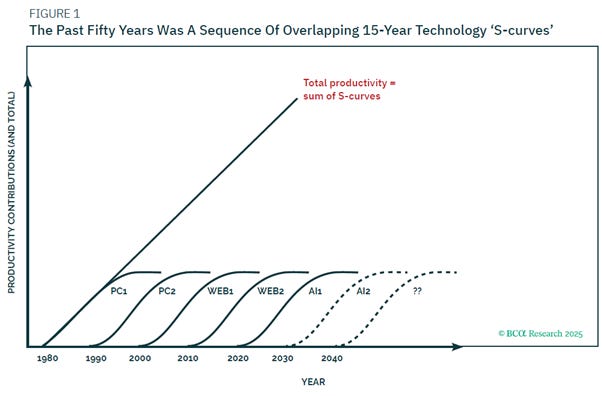

AI will undoubtedly transform how we live and work, much like past general-purpose technologies (GPTs) such as the PC and the internet. However, without repeating Paul Krugman’s infamous mistake of dismissing the internet’s economic impact as no greater than the fax machine’s. He should have acknowledged that while transformative, no technology, whether the internet, the PC, electricity, or the steam engine, has been singularly exceptional. Technological progress follows overlapping 15-year S-curves: the PC (1980–95), the laptop/cell phone (1990–2015), Web 1.0 (2000–15), Web 2.0 (2010–25), and now generative AI (2020–35). Initially, adoption is slow, then accelerates sharply before flattening as productivity gains diminish. Since these S-curves overlap, AI’s rapid adoption (2025–30) will coincide with the stagnation of prior technologies. For AI to drive an overall surge in productivity, its impact must surpass that of its predecessors, something for which there is no clear evidence. Thus, total economic productivity is likely to remain on its long-term steady-state trajectory.

Even if generative AI sustains productivity at its steady rate, the key question is: who benefits? There are three possible winners. In competitive industries, AI-driven efficiency will lower prices, benefiting consumers. In fields with 'superstar' workers, like law, healthcare, and creative sectors, AI will replace support staff, concentrating gains among top professionals. If AI has high barriers to entry, monopolies will capture most of the profits. This mirrors the Web 2.0 era (2010–25), where network effects created dominant monopolies, Google in search, Amazon in retail, Meta in social media, diverting productivity gains into corporate profits rather than wages, contributing to real wage stagnation since the 2010s.

AI enthusiasts often point to the Jevons Paradox. The Jevons Paradox, first observed by economist William Stanley Jevons in the 19th century, states that as technological advancements improve efficiency in resource use, overall consumption of that resource often increases rather than decreases. In the tech sector, advances in semiconductors, cloud computing, and fibre-optic networks have made computing more powerful and energy-efficient, yet demand for AI, data storage, and high-performance computing has surged. Faster processors, improved bandwidth, and lower costs have fuelled exponential adoption, leading to greater energy use and infrastructure strain. Rather than curbing consumption, efficiency gains in tech are expected to drive ever-expanding workloads, reinforcing the sector’s relentless growth cycle.

However, anyone with a common understanding of how technological breakthroughs work is aware of the risk of obsolescence, which is a regular occurrence in tech, as the list of faded, once seemingly omnipotent tech star companies is long. During tech bubbles, investors tend to forget about the risks and grossly overpay for stocks, as they have today. Hard lessons typically follow.

As the West grasped DeepSeek’s disruptive potential, the 47th U.S. president launched the Stargate AI initiative with his ‘tech bros’, a bold push to cement America’s dominance in AI and quantum computing, particularly against China. The program aimed to integrate AI into defence, enhance cybersecurity, and leverage quantum computing for breakthroughs in encryption, logistics, and drug discovery. While promising, it raised concerns over surveillance, autonomous weapons, and ethical risks. Savvy investors recognize that just as pipelines ensure cheap energy, AI’s future depends on data access, now considered the new oil. In this context, fibre-optic networks serve as AI’s infrastructure backbone, supporting cloud computing, national security, and economic competitiveness. As cyber threats and geopolitical tensions rise, sustained investment in fibre networks is crucial to maintaining U.S. technological leadership and digital resilience.

Globally, the fibre optics market is expected to grow from USD 3.2 billion in 2024 to reach USD 6.8 billion by 2029; it is expected to grow at a CAGR of 16.4% from 2024 to 2029. 5G infrastructure is dependent on optical fibre communication. These optical fibres can transfer data at high transmission rates from one location to another.

North America holds 16% of the global fibre optic cable market in 2024, driven by FTTH expansion, 5G rollouts, and government funding programs like BEAD, RDOF, and ReConnect. Growing demand for high-speed internet, cloud services, and data centre connectivity is fuelling investments in fibre infrastructure, with major telecom providers enhancing network resilience and reducing latency.

The fibre optic market in the US is a rather concentrated market with Cisco and Arista dominating the market in terms of market share.

Fiber optics technology enables high-speed, long-distance data transmission using light signals through thin glass fibres. The system consists of fibre optic cables, light sources (lasers or LEDs), optical amplifiers, and Wavelength Division Multiplexing (WDM) to transmit multiple signals simultaneously. Fiber optics offer advantages like faster speeds, immunity to electromagnetic interference, and enhanced security. The numerical aperture (NA), determined by the refractive indices of the core and cladding, measures a fibre’s ability to gather and transmit light. A higher NA improves light collection, data rates, and transmission efficiency, making it ideal for high-demand applications like telecommunications and data centres.

https://www.newport.com/t/fiber-optic-basics

Networking earnings are poised for a strong recovery in 2025, driven by higher telecom and enterprise spending as inventory backlog issues ease. The rebound will be broad-based, with telecom-focused companies likely seeing the strongest sales and EPS growth, while enterprise growth remains more modest. The AI networking sales rebound is expected to benefit leading vendors like Arista, Ciena, and Corning, with Ethernet emerging as the dominant technology for cloud AI networks. Arista is expected to see the largest gains, potentially surpassing $1 billion in AI backend sales in 2025, while Ciena and Corning could benefit from data-centre interconnects and fibre optics.

The rapid growth of generative AI infrastructure is creating an $18 billion sales opportunity by 2028, according to 650 Group. Ethernet is expected to replace Nvidia's InfiniBand as the leading technology in 2025, driven by an ecosystem of chips and standards that enable hyperscalers to disaggregate infrastructure. AI networking, which reached $3 billion in sales in 2024, is projected to grow 43% annually, reaching $17.6 billion by 2028. While InfiniBand currently leads with 53% of total sales and 73% of back-end AI network sales, Ethernet AI chips and software standards are expected to accelerate adoption in late 2024, pushing Ethernet ahead of InfiniBand in 2025.

While Stargate will inevitably benefit US suppliers, other measures such as tariffs are unlikely to have a significant impact on US fibre optic manufacturers, as networking sales are mostly regional. Chinese suppliers have minimal US presence, limiting market share opportunities for US vendors from China-related restrictions. Tariffs, however, could affect vendor sales, with Cisco, Juniper, and Arista realigning supply chains away from China. Tariffs on Mexican products could raise equipment prices and margins, although companies may pass these costs to customers, which could take a couple of quarters.

As usual, savvy investors didn't wait for the 47th US president's flashy stargate initiative to recognize the critical role of networking in AI's expansion with the global data networking sector outperforming the Nasdaq and the Magnificent 7 since last July.

Relative performance of Global Data Networking & Communication Equipment Index to Nasdaq Index (blue line); to Magnificent 7 index (red line) in USD since December 29th, 2023.

As the American president and his 'techligarchs' are ‘deep thinking’ through a stargate that tariffs and bans will stop the rest of the world from progressing to their bright mercantilist future, investors who have relied almost exclusively on passive investments over the past two years, buying the dips in the increasingly less ‘Magnificent 7’ stocks that were supposed to dominate the world, will increasingly realize that their equity allocations must be reduced. This shift will occur as the US economy transitions from the ongoing inflationary boom into an inflationary bust, favouring real assets like physical gold and silver. These investors will also come to understand the growing importance of sector and stock picking within equity markets. A balanced allocation across IT, Energy, and Aerospace & Defence sectors, each of which has outperformed the S&P 500 not only at the start of the decade but also during the most recent inflationary bust (January 2022 to March 2023), will be crucial. Additionally, investors will take note that during the same period, the global data networking sector outperformed the S&P 500 IT Index by more than 4%. In an inflationary bust, savvy investors know the riskiest part of a smart defence equity portfolio is exposure to energy-consuming companies (e.g., IT). As a result, investors will need to manage actively this allocation and look for part of the IT sector, such as the networking sector, which will deliver access to cheap data to every users who are going to understand that an inflationary bust is a period when they can buy even less for even more than over an inflationary boom.

Relative Performance of Equity Smart Defence Portfolio to the S&P 500 index (blue line); Global Data Networking & Communication Equipment Index to S&P 500 IT Index (red line) in USD between January 2022 and March 2023.

As tariffs are increasingly used as tools of negotiation or even to spark perpetual kinetic bankers' wars, it’s clear that the world is heading toward a depression for some nations, driven by an impending sovereign debt crisis that will be remembered in the history books as the "Trump stagflation." Ultimately, the global business cycle cannot be altered, regardless of who sits in the Oval Office. To weather the upcoming "Trump stagflation," holding physical gold, the only antifragile asset with no counterparty risk, alongside a portfolio of short-dated investment-grade (IG) USD bonds with maturities of less than 12 months and Treasury bills (T-bills) with maturities not exceeding 3 months will provide stability as Trump’s economic decisions lead to "Trump stagflation."

By doing this, investors will continue to prioritize the RETURN OF CAPITAL over the RETURN ON CAPITAL, enjoying both peace of mind and preserved wealth.

WHAT’S ON THE AGENDA NEXT WEEK?

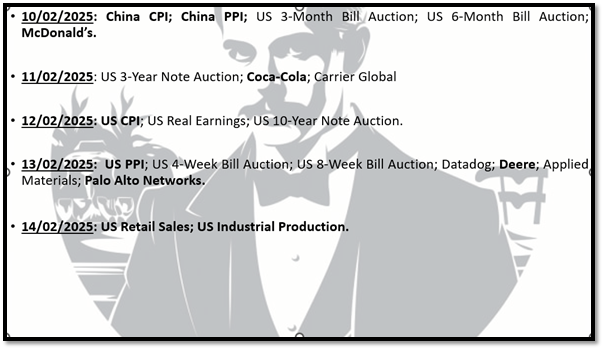

The second week of the second month of the jubilee year will bring investors’ focus to inflation data in China and the US with the release of January CPI and PPI for the world's two largest economies. The week will also offer an additional check on US consumer health with the release of January retail sales. Another 137 companies from the S&P 500 index will report earnings, including McDonald's, Coca-Cola, Deere, and Palo Alto Networks.

KEY TAKEWAYS.

As the second month of the jubilee year unfolds, the key takeaways are:

January's ISM data showed strengthening manufacturing sentiment but weakening services growth, as tariff concerns fuelled uncertainty, continuing the post-election trend.

January’s NFP report showed weak job growth, government-driven hiring, rising wages, and an unemployment rate still flashing an imminent economic bust.

Amid rising polarization and tariff fears, consumer sentiment worsened in February, with inflation expectations surging to their highest since November 2023.

AI will transform society like past general-purpose technologies, but its impact on productivity may follow similar S-curves, with no clear evidence it will surpass previous technological revolutions.

As the world is still ‘Deep Thinking’ , the U.S. recently launched the Stargate AI initiative to enhance its AI and quantum computing leadership, with fibre-optic networks critical for supporting AI's data needs and ensuring digital resilience.

Networking earnings are primed for a 2025 rebound, with Ethernet taking the lead in AI, driving growth while tariffs have limited impact on U.S. fibre optic makers.

As tariffs fuel a mercantilist future, investors should continue to focus on the Smart Defence Equity Portfolio with data networking replacing the broad-based IT sector during the inevitable upcoming inflationary bust.

As volatility is expected to rise, investors should favour antifragile assets like gold over bonds, as gold offers low equity correlation, stability, and resilience against currency debasement.

In such environment, investors will once again need to focus on the Return OF Capital rather than the Return ON Capital, as stagflation spreads.

Physical gold remains THE ONLY reliable hedge against reckless and untrustworthy governments and bankers.

Gold remains an insurance to hedge against 'collective stupidity' and government’ hegemony which are in great abundance everywhere in the world.

With continued decline in trust in public institutions, particularly in the Western world, investors are expected to move even more into assets with no counterparty risk which are non-confiscable, like physical Gold and Silver.

Long dated US Treasuries and Bonds are an ‘un-investable return-less' asset class which have also lost their rationale for being part of a diversified portfolio.

Unequivocally, the risky part of the portfolio has moved to fixed income and therefore rather than chasing long-dated government bonds, fixed income investors should focus on USD investment-grade US corporate bonds with a duration not longer than 12 months to manage their cash.

In this context, investors should also be prepared for much higher volatility as well as dull inflation-adjusted returns in the foreseeable future.

HOW TO TRADE IT?

The first week of the second month of the jubilee year saw yet another round of a ‘chaos monkey’ market, where trading remains driven more by Truth Social tweets, leading to wild swings. Notably, the Nasdaq was the only one of the three major indices to end the week in the green, outperforming the S&P 500 and the Dow Jones, despite two more Magnificent 7 members issuing disappointing guidance for the current quarter. Year-to-date, the Dow continues to lead, while the Magnificent 7 have turned negative since the start of the year. As of February 7, 2025, all three major U.S. indices—the Dow, S&P 500, and Nasdaq—remain in bullish daily reversals. However, with the Magnificent 7 closing below its 50-day moving average for the first time since early September, the ongoing rotation from growth stocks to more value-oriented names like those in the Dow reflects the slow and painful, yet inevitable, shift of the U.S. economy from an inflationary boom to an inflationary bust.

"Chaos Monkey," a tech industry term, refers to stress-testing systems by introducing failures to ensure resilience. As Mega-Cap tech earnings continue to disappoint, with Mag7 stocks losing over $625 billion in market cap over two weeks, investors should recognize that the market is already pricing in what lies ahead evidenced by the Dow Jones outperforming while the Nasdaq weakens over the jubilee year.

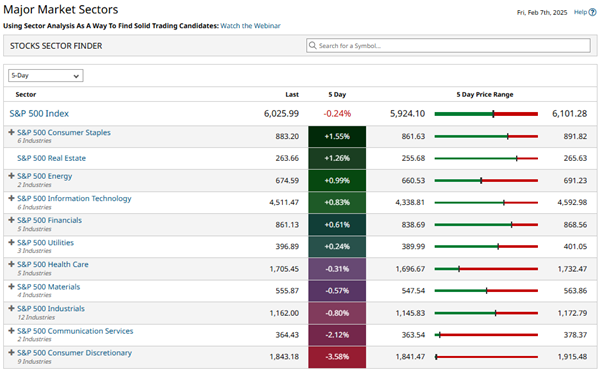

In this context, it's no surprise that Consumer Staples, Real Estate, and Energy outperformed, while Communication Services and Consumer Discretionary lagged.

As of February 7th , 2025, the US remains in an inflationary boom, but with the S&P 500 to Gold ratio below its 7-year moving average, an inflationary bust will materialize much sooner than Wall Street pundits and their parrots are eager to tell their clients. In this context, investors should stay calm, disciplined, and use market data tools to anticipate changes in the business cycle, rather than fall into the forward confusion and illusion spread by Wall Street.

In the perpetuating environment of monetary illusion, fueled by additional tariffs that will inevitably push the world from an inflationary boom to an inflationary bust, equity investors will need to be increasingly selective in allocating their portfolios to growth stocks. While they should underweight these stocks, investors can turn to the global networking equipment sector to stay invested in IT while avoiding the overowned and overhyped Magnificent 7. In an inflationary bust, investors understand the importance of a disciplined, rigorous quantitative approach to stock picking. Within this subindustry, investors will focus exclusively on stocks with a long track record of growing EPS, sales, free cash flow, and low leveraged balance sheet. As of end of January 2025, there are 5 companies which are meeting these criteria.

A backtest of this systematic and disciplined quantitative approach has delivered a total return of more than 162% since the start of the decade, outperforming the Global Networking & Communication Equipment Index by more than 100% over the period.

As the global economy, including the U.S., transitions into an inflationary bust, gold remains the ultimate antifragile asset, outperforming government bonds, cash and Bitcoin. Fixed-income assets, once a staple of the Permanent Browne Portfolio, are now more "pipe dream" than reliable. Savvy investors have learned that once the economy is in an inflationary bust, they will have to focus exclusively on energy producers, aerospace defence, and energy infrastructure equities to secure returns and navigate this challenging period. In the years ahead, wealth preservation will depend on physical gold and disciplined equity selection, not on fleeting Wall Street recommendations but based on a disciplined and unbiased quantitative process. This strategy provides a shield against wars, reckless government policies, and the looming spectre of ‘Trump Stagflation.’ which will lead into World War 3.

If this report has inspired you to invest in gold, consider Hard Assets Alliance to buy your physical gold:

https://www.hardassetsalliance.com/?aff=TMB

Disclaimer

The content provided in this newsletter is for general information purposes only. No information, materials, services, and other content provided in this post constitute solicitation, recommendation, endorsement or any financial, investment, or other advice.

Seek independent professional consultation in the form of legal, financial, and fiscal advice before making any investment decisions.

Always perform your own due diligence.