Eternal Bullion…

Why Gold Outlives Every Empire That Tries to Replace It

The Week That It Was…

The third week of Q2’s final month proved yet another holiday-shortened affair, as China’s Dragon Boat Festival, Hong Kong’s Tuen Ng Day, and America’s Juneteenth converged with suspicious convenience to give traders a collectively sanctioned excuse to abandon their Bloomberg terminals. Before the long weekend rescued everyone, investors endured the usual parade of economic entertainment: Bank of Japan and FOMC meetings delivered their carefully rehearsed non-commitments, while retail sales data from China and the United States confirmed that the consumer remains alive but increasingly unimpressed. Six S&P 500 companies reported earnings, though none managed to upstage the far more riveting spectacle of central bankers and soccer players competing to explain, with matching conviction and equal credibility, why everything remains “transitory.”

As a birthday gift for the Manipulator-in-Chief’s 80th, Washington unwrapped yet another Memorandum of Understanding — the geopolitical equivalent of a gift card with terms and conditions on the back — delivering a 60-day truce in a war that was, lest we forget, victoriously concluded on Hour 1 of Day 1. The financial press duly erupted in celebration: oil prices fell sharply, prediction markets assigned better-than-even odds of a Hormuz recovery in H2, and traders briefly convinced themselves that a document with unpublished clauses, multiple circulating versions, and zero implementation details constitutes a peace deal rather than a press release. The proposed terms sound suitably magnificent — Iran agrees not to pursue a nuclear weapon, the Strait reopens, $25 billion in frozen assets get released, and a 60-day negotiation window addresses sanctions, enrichment, and “broader regional security issues,” which is diplomatic shorthand for everything that has resisted resolution for forty years.

The first problem is that reopening the Strait is not as simple as issuing a press release — a concept that appears to have eluded the markets celebrating it. Mines must still be physically removed from the water, security guarantees must be established by parties who have spent the last hundred days trying to sink each other’s vessels, and shipping companies — having learned the hard way that one drone strike can close a waterway faster than any MOU can reopen it — are sensibly refusing to send billion-dollar tankers back until the math actually works on insurance. Commerce may resume in headlines long before it resumes in reality.

The second and rather more inconvenient problem is that the core dispute has not been resolved — it has been scheduled for resolution, which is an entirely different thing. The agreement merely opens a 60-day negotiation window on Iran’s nuclear programme, sanctions relief, and uranium enrichment: the precise issues that ignited the crisis in the first place and have resisted resolution through every administration since 1979. Israel is already denouncing the deal for ignoring missiles and regional proxies; Iranian hardliners are denouncing it from the opposite direction for surrendering leverage for uncertain promises. When both sides declare themselves betrayed before the ink is dry, the market is not pricing in peace — it is pricing in the hope that everyone stays politely betrayed for at least 60 days.

https://www.theguardian.com/world/2026/jun/15/israel-territory-lebanon-defence-minister-israel-katz

In the Tel Aviv theocracy, regime change lurks behind the curtain like a debt collector who’s finally run out of patience — because whatever sins “Sata-Nyahu” accumulated in office, his successors are lining up to make him look positively angelic by comparison. The hardline chorus erupted in biblical fury over The Manipulator In Chief-brokered US-Iran ceasefire, denouncing it as a divine gift to the Ayatollahs that leaves Iran’s nuclear infrastructure, ballistic missiles, and regional proxy network not merely intact but freshly validated — a deal so generous to Tehran that even the devil would have negotiated harder.

https://www.jpost.com/israel-news/politics-and-diplomacy/article-899421

The mistake markets keep making with the enthusiasm of a golden retriever greeting the same stranger for the hundredth time is assuming that reopening a waterway resolves a geopolitical crisis — it does not, any more than removing a fever treats the underlying infection. The Strait of Hormuz is a symptom; the 40-year confrontation between Washington, Tehran, Tel Aviv, and everyone else with a regional grievance and a proxy army is the disease. Even if the Strait reopens tomorrow, insurance premiums don’t instantly collapse, tanker operators don’t suddenly forget that their vessels were targeted, and capital — once burned — develops a long and unforgiving memory. The broader war cycle is expanding, not contracting, regional rivalries, religious tensions, sanctions, energy competition, and the East-West fracture are all firmly intact, and the diplomatic handshake that is supposed to resolve them has the historical track record of a New Year’s resolution made after the third glass of champagne. The First World War was also supposed to be over by Christmas — and the Middle East has been running on “temporary ceasefires” since before most current policymakers were born.

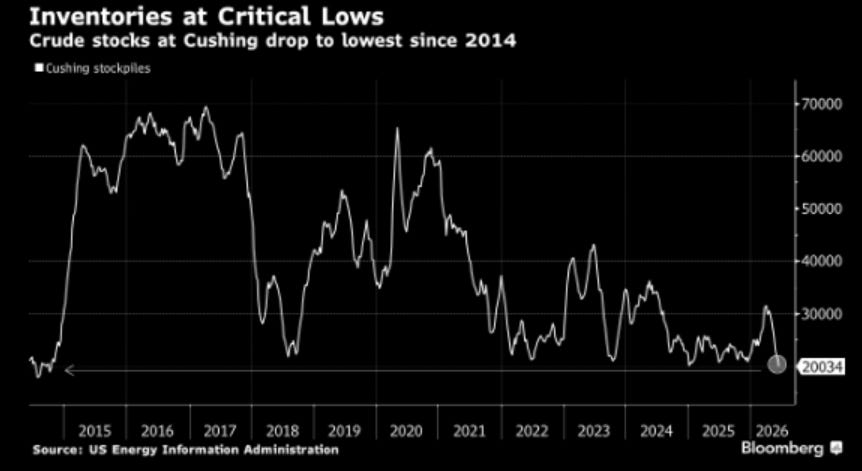

The Ministry of Energy Abundance has a small administrative update: the Empire’s Strategic Petroleum Reserve has quietly hit its lowest level since 1983 — approximately 340 million barrels — while the Manipulator-in-Chief stood before the G7 in France to announce, with the casual candour of a man who has misplaced the classification stamp, that global oil reserves were approximately four weeks from bedlam before the Iran MOU arrived to save civilisation.

The White House, asked to elaborate on whether the President was referring to US or global inventories, heroically referred journalists back to the original remarks — a response that translates as “we also don’t know.” The IEA, that organisation of oil-consuming nations devoted to explaining why everything is fine, had already warned that reserves “are not endless” and that demand would exceed supply this year, while 400 million barrels of strategic reserves were released across IEA member countries at the war’s outset to paper over the arithmetic. The deal that prevented bedlam was signed, celebrated, and declared a historic victory — by the same administration that drew down the reserves, started the bombing, and is now congratulating itself for stopping. The Empire didn’t save the oil market — it burned through its emergency stockpile, declared victory, and sent the invoice to be paid later.

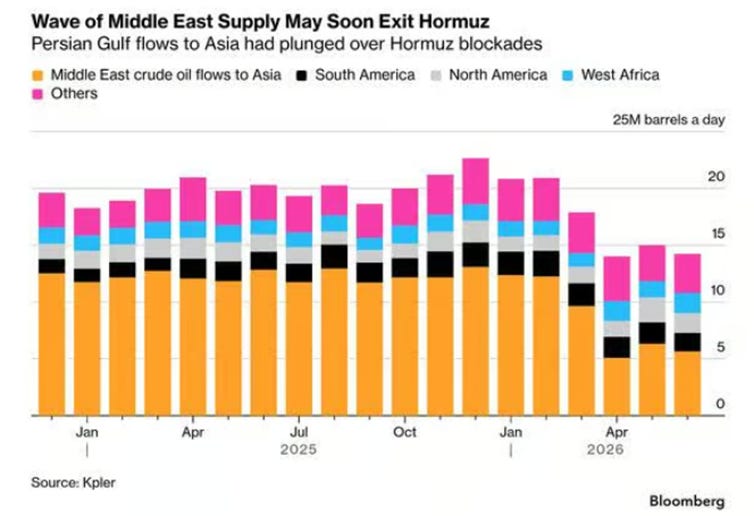

In a plot twist nobody who read the fine print could possibly have anticipated, the Hormuz peace deal that is supposed to unleash a flood of cheap Gulf oil onto grateful Asian refiners is expected to deliver over 60 million barrels of crude on three dozen supertankers queued at the exit of the Strait.

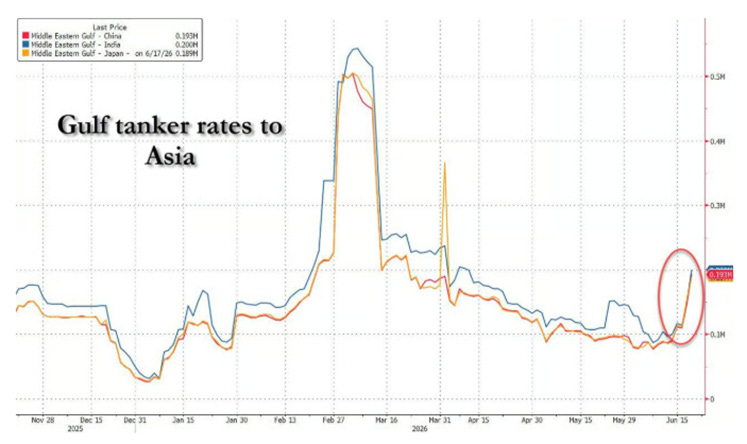

The problem is that nobody wants to pay to collect them. PetroChina sought a supertanker to load Iraqi crude and received offers at tanker rates nearly triple pre-war levels, while Indian Oil IOC issued a force majeure after receiving zero offers whatsoever on its tender — the shipping industry’s elegant way of saying the oil is theoretically available but practically stranded. The problem, as a PetroChina official summarised with admirable brevity, is that “there are tankers available, but the problem is it’s too expensive and there is no guarantee you can exit the strait“ — which is precisely the same problem that existed before the peace deal, now repackaged with a 60-day expiry date and a press conference. Wall Street EYIs have already slashed their oil price forecasts as investment banks celebrated a supply glut that Asian refiners are declining to absorb at current freight rates, and the Strait remains, for all practical shipping purposes, a toll road where the toll is triple and the exit is not guaranteed. In a nutshell, the Versailles Peace deal opened the Strait on paper — the tanker market is still reading the footnotes.

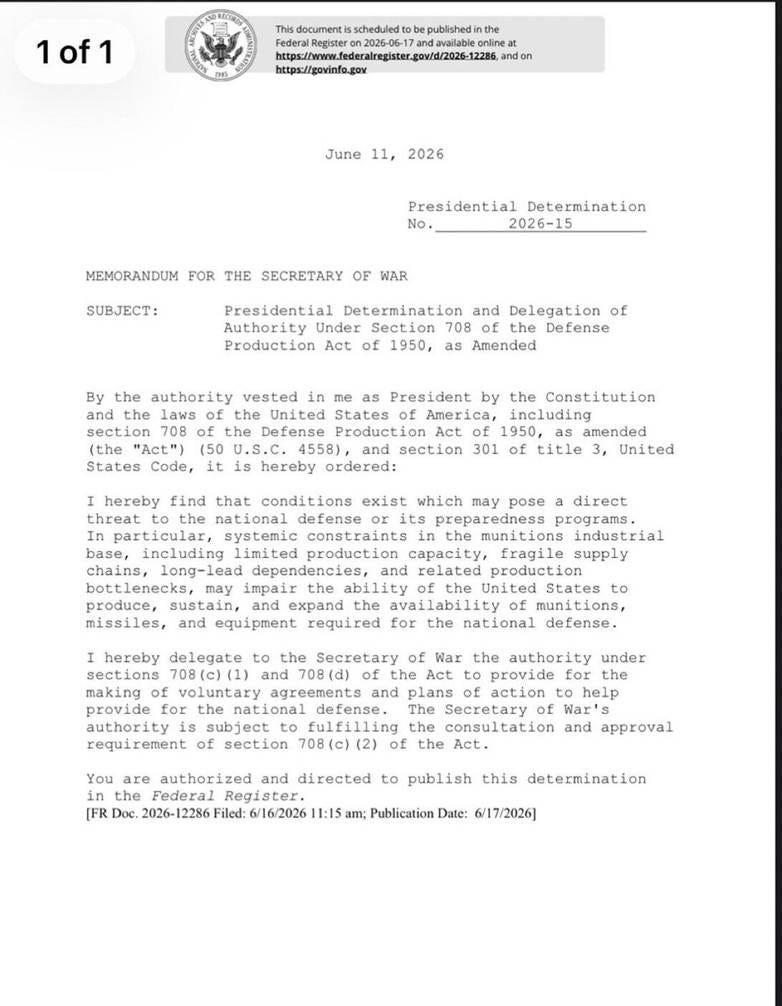

The Ministry of Perpetual Readiness of the Empire has issued a clarifying update: stockpiles are “strong and will only get stronger,” according to War Secretary The Pete — who made this reassuring announcement in the same breath as the administration quietly invoked the Cold War-era Defence Production Act, directed the Pentagon to seek $350 billion in emergency defence spending, and had Senator Cornyn inform the Senate that the military is “running short of funding to acquire the weapons and missiles needed to protect the nation.” The war declared won on Hour 1 of Day 1 has, it emerges, consumed munitions inventories at a pace sufficiently alarming that The Warmonger In Chief signed a June 11 memo finding that “conditions exist which may pose a direct threat to national defence,” — a sentence the White House apparently did not consider contradictory to its simultaneous victory declarations. The Empire fought a short, decisive, totally successful war, exhausted its strategic petroleum reserve to its lowest level since 1983, drew down its weapons stockpiles to emergency levels, and is now spending an additional $350 billion to restock the shelves — all while assuring the public that everything is strong and getting stronger.

When the seven most indebted nations on earth gathered in France to drink Evian mineral water and discuss the global order they are busily bankrupting, wise men travel to Kazan instead. While the G7 — now more accurately described as the G7 Debt Appreciation Society — convened under the hospice of MacroLeon to contemplate their collective fiscal ruin, Russia hosted the first-ever Russia-ASEAN summit on the banks of the Volga, celebrating 35 years of dialogue partnership with eleven nations that have spent the entire Western sanctions campaign conspicuously declining to sanction anyone. Tsar Vladimir, in the Confucian tradition of the host who says everything while committing to nothing, welcomed all parties to build “a just and democratic multipolar world order” — a sentence that translates as “we would prefer a world where Washington’s loyalty card has fewer rewards points.“ The superior man notes that ASEAN nations, home to nearly 700 million people and some of the fastest-growing economies on earth, have concluded that maintaining relations with Moscow, Beijing, and Washington simultaneously is not hypocrisy but rather the ancient and profitable art of keeping all doors open while committing to none. When the indebted lecture the world on order from a French château while the multipolar world quietly meets in Kazan, the centre of gravity has already moved — it simply hasn’t updated its address yet.

https://apnews.com/article/russia-putin-asean-summit-kazan-10599e42de372d53ec740c17f5327def

While the Ministry of Peace was busy celebrating its Middle Eastern ceasefire subscription service in another Treaty of Versailles, the other Eurasian conflict — the one the White House had apparently filed under “handled” — delivered a timely reminder that wars do not observe G7 schedules. Ukraine launched its largest-ever drone barrage against Moscow, striking the Gazprom Neft refinery, shutting down all four civilian airports, evacuating Sheremetyevo passengers to shelters, and closing major highways across the capital — a sequence of events that sits awkwardly alongside Donald Copperfield’s simultaneously delivered assessment that “Russia should make a deal.” The Manipulator-in-Chief, fresh from declaring one war won and another nearly negotiated, told reporters he’d had “a very good meeting” with Kyiv Dancer on High Heels Cokehead — which is the diplomatic equivalent of a fire chief announcing a productive conversation while the building burns behind him.

The Ministry of Beneficial AI has announced, with the serene efficiency of a Friday evening 9 p.m. press release, that Anthropic has been ordered to immediately pull the plug on all foreign access to Claude Fable 5 and Mythos 5 — including its own foreign national employees — just four days after their triumphant launch, citing a national security export control directive. The pretext is a theoretical universal jailbreak that, in a detail the government of the Empire apparently missed during its review, no tester has actually found — with disclosed potential jailbreaks described as either entirely benign or providing no model-specific uplift whatsoever. Anthropic had already warned before launch that perfect jailbreak resistance is not currently possible for any model provider — a philosophical position Washington apparently treats as a four-day processing time. The punchline: to ensure compliance with a foreign-access ban, Anthropic was forced to shut off its most advanced models for every customer on the planet — the geopolitical equivalent of burning the library to stop one person from reading the wrong book. In the race to win the AI war, America’s opening strategy was to confiscate its own weapon.

https://www.anthropic.com/news/fable-mythos-access

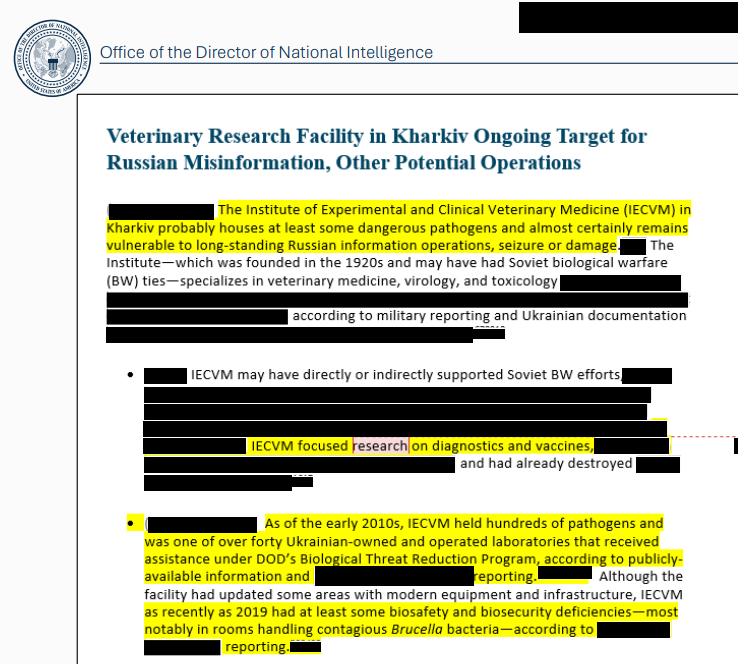

In her final act as outgoing Director of National Intelligence — presumably before the Ministry of Truth reassigns the filing cabinet — Tulsi The Brave has spent her last weeks in office detonating a remarkable quantity of carefully maintained official fictions. First, she declassified intelligence slides confirming that the US government funded more than 120 biolabs across 30 countries, including over 40 in Ukraine, information she says was “knowingly withheld from the American people” while officials including Dr. Fauci “lied repeatedly” about their existence — and threatened those who tried to expose the truth.

https://www.dni.gov/files/BIOLAB_Slides.pdf

Then, in a complementary act of institutional self-immolation, she retracted the intelligence community’s own assessments on Havana Syndrome, finding they had selectively excluded inconvenient evidence, relied on an ethically flawed medical study, and were developed in a manner inconsistent with analytic integrity — which is the bureaucratic way of saying the reports were engineered to reach a predetermined conclusion while the afflicted diplomats and intelligence officers were quietly denied medical care. Taken together, the two revelations sketch a portrait of an intelligence apparatus that spent years simultaneously running programs it denied existed and dismissing the injuries of its own people with reports it now admits it fabricated.

When the outgoing intelligence chief’s farewell gift is proof that the intelligence community lied about biolabs and its own wounded, the conspiracy theorists are owed a very long apology.

The Ministry of Ever-Closer Union has announced, with the solemn gravitas of a press release written by committee, that Eurostan has taken “a major step forward” by agreeing to open the first accession negotiation cluster with Ukraine and Moldova — covering the “core values and principles on which the EU is built, from the rule of law to strong democratic institutions” — a sentence delivered with a straight face by an institution whose founding members include France, currently on its third finance minister of the year, and Italy, which has not balanced a budget since the introduction of the euro. The timing is impeccable: Brussels is formally inviting a country, notoriously corrupt and still actively at war, with a reconstruction bill estimated in the hundreds of billions, into a club whose existing members are simultaneously running deficits above the rules they never enforced, fighting over migration policies they never agreed on, and borrowing money to fund a defence posture they outsourced to Washington for seventy years. The Witch Ursula declared that “enlargement remains one of the EU’s greatest success stories and our best investment in our shared future“ — which is precisely the kind of sentence that sounds magnificent in a press release and terrifying in a budget meeting. Welcoming a war-ravaged nation into a fiscally insolvent union and calling it a strategic investment is either visionary leadership or the world’s most ambitious exercise in shared denial.

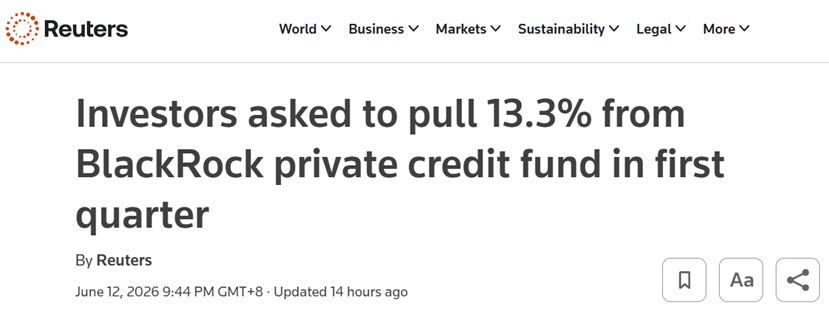

In a development that will shock precisely nobody who remembers that “illiquid“ and “alternative“ are just polite synonyms for “you’ll get your money back when we feel like it,” BlackRock has joined the long list of private debt funds by capping redemptions from its flagship HLEND private credit fund for the second straight quarter after investors attempted to pull a rather emphatic 13.3% — up from 9.3% last quarter — only to be informed they may retrieve a gracious 5%, the financial equivalent of asking for your coat back at a party and being handed one sleeve. This follows Cliffwater gating investors for a second straight quarter and Blackstone — which had heroically tapped senior executives for hundreds of millions of their own cash to satisfy Q1 redemptions — finally surrendering and joining the gate parade in Q2; apparently even the masters of the universe have limits. BlackRock helpfully reminded investors that this “liquidity feature“ is actually a premium service, which is the asset management industry’s sophisticated way of explaining that the exit door only opens in one direction. Meanwhile, industry leaders are warning of rising defaults as AI disrupts borrowers and ultra-low-rate-era debt comes due — suggesting the $1.8 trillion private credit market may be discovering, with considerable surprise, that credit cycles did not in fact get cancelled. When the world’s largest asset managers start gating their own flagship funds in convoy, the “premium return” starts looking suspiciously like a premium prison.

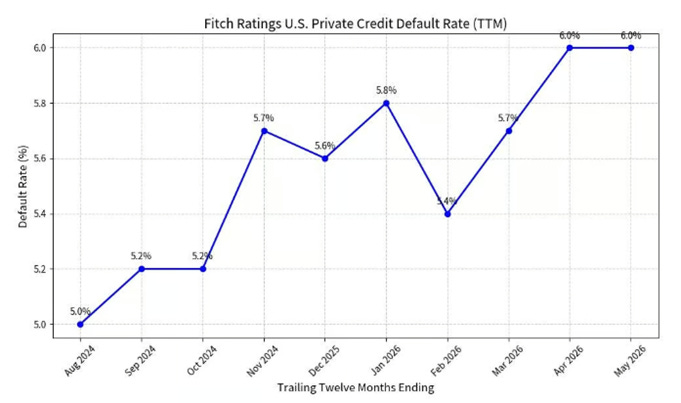

In a development that will stun precisely nobody who noticed that BlackRock, Blackstone, and Partners Group have all been quietly installing redemption gates like emergency fire exits in a burning building, Fitch Ratings has confirmed that the US private credit default rate held at a record 6% in May — logging 14 default events across 1,500 issuers, with six serial defaulters and half of all defaults consisting of maturity extensions under stress — the financial equivalent of a borrower asking for more time to find the money they already didn’t have. Private credit is exposed to the software sector for up to 20% of its loans, which is a delightful concentration given that AI is currently disrupting the very business models backing those loans. The industry’s reassurance that “systemic risk appears far less pronounced than subprime in 2008” deserves a special award for the most expensive sentence in financial history — because “it’s not subprime 2008” is precisely the kind of comfort that looks magnificent in a June press release and considerably less so in a November post-mortem.

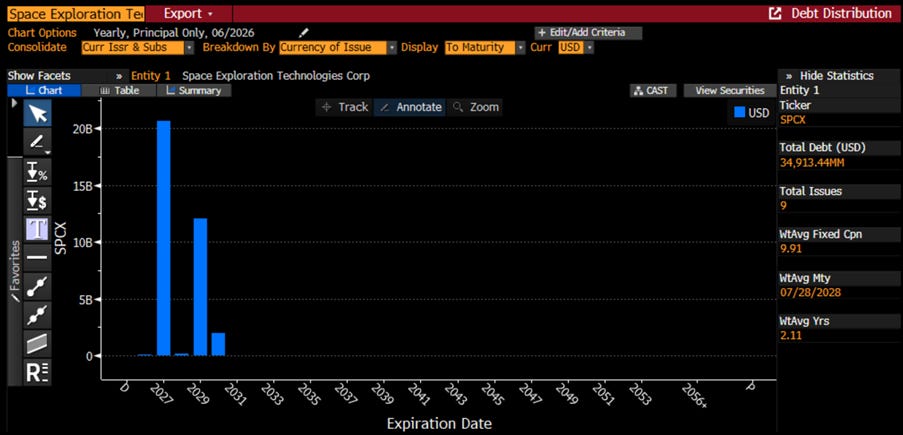

In a move that will surprise nobody who noticed the fine print, SpaceX — fresh off the biggest IPO in history, which turned The Elon into the world’s first trillionaire and its stock promptly down 10% — is preparing to issue at least $20 billion in investment-grade bonds next week, the proceeds of which will refinance a $20 billion bridge loan that makes up the bulk of its $29.1 billion in long-term debt — meaning the record-breaking IPO was essentially a glamorous appetiser before the main course of debt issuance arrived. SpaceX didn’t go public to fund the future — it went public to refinance the past, and called it a revolution.

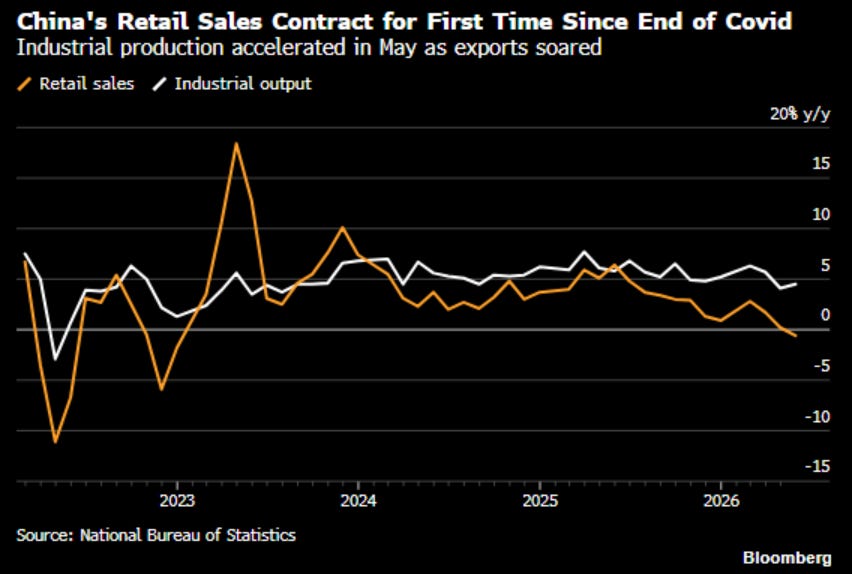

China’s May data arrived like an uninvited houseguest bearing contradictions: retail sales fell 0.6% year-on-year — their first decline since the post-Covid reopening — fixed-asset investment retreated 4.1%, private investment slumped 7.1% at its worst pace since 2020, and car purchases plunged 16%, suggesting the Chinese consumer has studied the art of the closed wallet with monastic discipline. Meanwhile, the factory hummed heroically: industrial production climbed 4.5%, high-tech manufacturing soared 15%, semiconductors exports exploded 111%, and AI-related electronics jumped 17% — proof that the Middle Kingdom has mastered the ancient paradox of producing everything the world desires while its own citizens desire nothing at all.

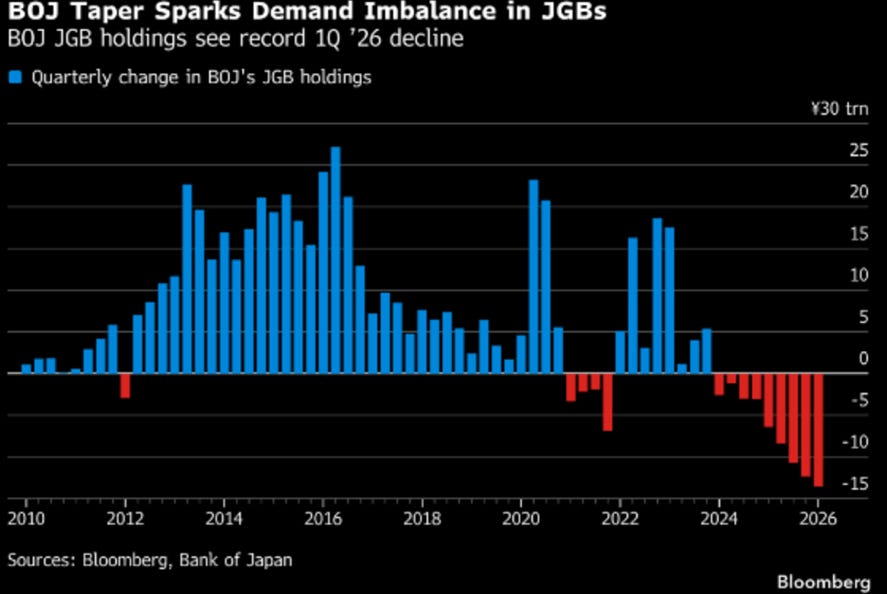

In another landmark moment for a central bank that spent three decades perfecting the art of doing nothing, the Bank of Japan heroically raised rates to 1% — its highest since 1995 and a number the rest of the developed world would recognise as still essentially zero, but which in Japanese monetary policy circles qualifies as a hawkish revolution worthy of a ticker-tape parade. The accompanying decision to pause bond purchase tapering was immediately punished by the super-long JGB market, with yields on 20-year-and-above tenors rising on the entirely reasonable observation that pausing a taper does nothing to fill the structural demand void the taper already created — foreign sellers active, domestic buyers tentative, life insurers returning “selectively,” which is polite bond-market language for “barely.” The taper pause stops the active bleeding while passive redemption runoff ensures the balance sheet shrinks anyway — the monetary equivalent of announcing you’ve stopped punching yourself while your nose continues bleeding on the carpet.

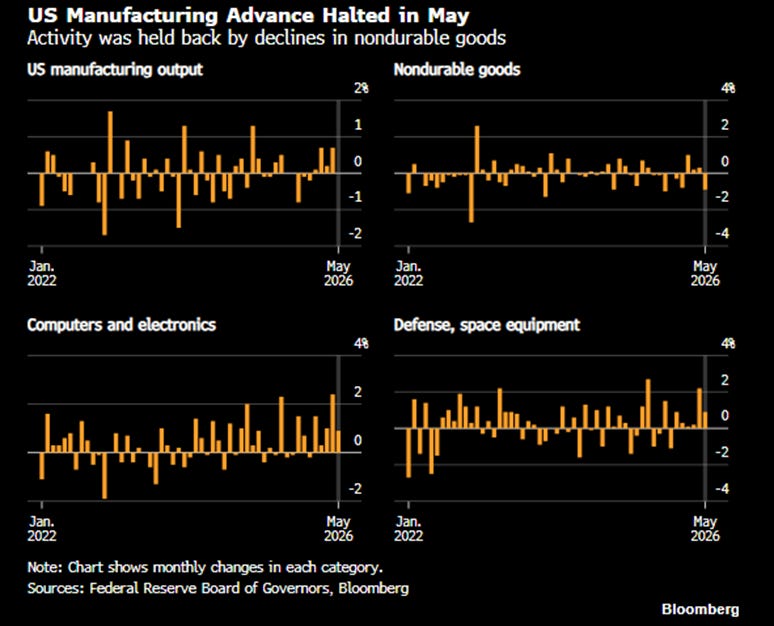

America’s long-awaited manufacturing renaissance arrived in May and immediately sat down for a rest, with factory output flatlining after four months of gains — missing the consensus forecast with the quiet dignity of a student who studied the wrong chapter. The headline conceals a tale of two factories: durable goods, data centres, computers, and defence equipment hummed along heroically, with computer and electronic output up more than 4% over three months — its best run in five years — while nondurable goods manufacturing was dragged into the gutter by chemicals and petroleum, with synthetic dyes and pigments alone dropping 5.5%, a supply-chain casualty of the war that Washington declared won in Hour 1. Looking at the data with forensic precision, US factory output actually increased in only about one-third of categories — which is the polite way of saying two-thirds of American manufacturing is either stagnant or declining while the press release celebrates the remaining third.

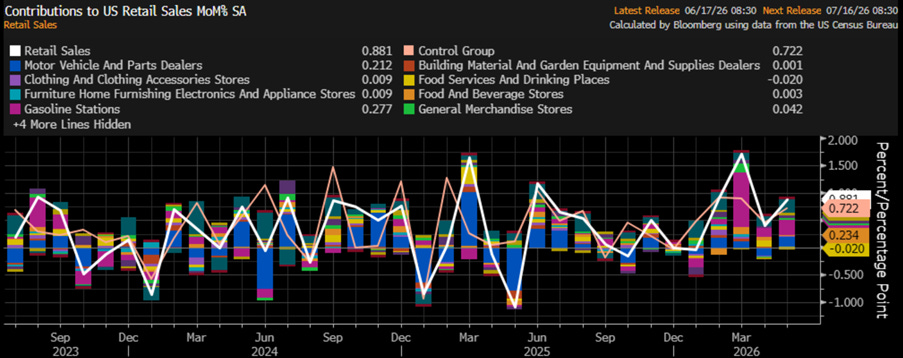

In a triumph of statistical presentation, May retail sales rose a headline 0.9% — a number that loses considerable glamour once one notices that gas station receipts alone jumped 3.4%, meaning Americans didn’t spend more because they felt wealthy but because filling the tank got more expensive courtesy of the Iran war. Strip out the gasoline inflation effect and the picture is a firm but thoroughly unspectacular 0.7%. The fine print is even more instructive: the figures are not adjusted for inflation, real wages are declining, the savings rate is sliding, and the card data from BofA and JPMorgan quietly reveal that it’s wealthier Americans doing the heavy spending lifting while lower-income households navigate tighter budgets and elevated borrowing costs — a K-shaped “resilience” that would be more honestly described as two entirely different economies sharing the same headline.

Adjusted for CPLie, headline retail sales managed a heroic +0.24% MoM in real terms — barely clawing to January 2021 levels, which sharp-eyed historians of recent financial disasters will recognise as the precise inflection point that preceded the last stagflationary surge. The consensus will naturally overlook this inconvenient parallel, busy as it is celebrating the nominal number with the analytical rigour of someone reading only the restaurant’s name and not the bill.

US Retail Sales Adjusted to inflation (i.e. CPI) (blue line); S&P 500 to WTI ratio (yellow line); 7-Year Moving Average of the S&P 500 to WTI ratio (red line).

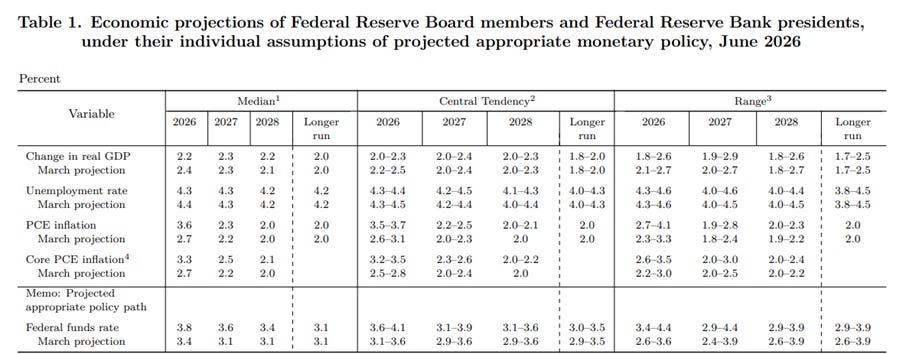

The Federal Reserve’s debut under Kevin “The New Sheriff” Warsh opened with a unanimous non-event — rates parked at 3.5%–3.75%, untouched, while the main act was not a decision but a deletion: paragraph 4 of the policy statement amputated, forward guidance abolished, and the market’s beloved hand-holding ceremonially discontinued. Regime change, delivered by scissors. The projections accompanying this historic act of editing were, to use the technical term, not great: core PCE now forecast at 3.3% this year — upgraded from March’s 2.7% to precisely match the latest actual reading, meaning the Fed’s heroic disinflation forecast amounts to “from here, none” — while the median dot gamely promises 2.5% next year, growth slows politely, unemployment somehow improves anyway, and everything magically converges to 2.7% by year-end, because in central banking optimism isn’t a bias, it’s a job requirement. The forecast, as ever, remains exactly one revision away from perfection.

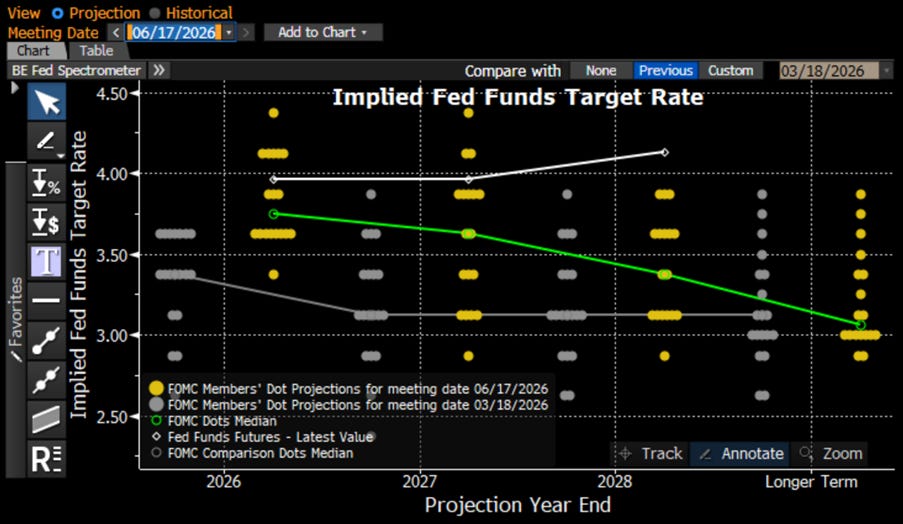

The dot plot staged a full ideological coup: where the prior Fed had zero officials pencilling in hikes, nine have suddenly discovered their inner hawk — one brave soul going for three, five for two, three for one — while the entire dovish wing evaporated almost entirely, leaving a single lonely cut-believer clinging to the wreckage of last quarter’s consensus. The committee that spent 2025 debating how fast to ease is now debating how fast to tighten, which is either a triumph of data-dependence or an embarrassing admission that the last set of dots aged like warm milk. The finishing touch: only 18 of 19 officials submitted a dot at all, with the missing entry widely attributed to Warsh himself — the man campaigning to abolish forward guidance declining, with perfect consistency, to contribute to the guidance chart. Enjoy it while it lasts; under a Chair who’d happily shred it, this dot plot may be among the last of its kind.

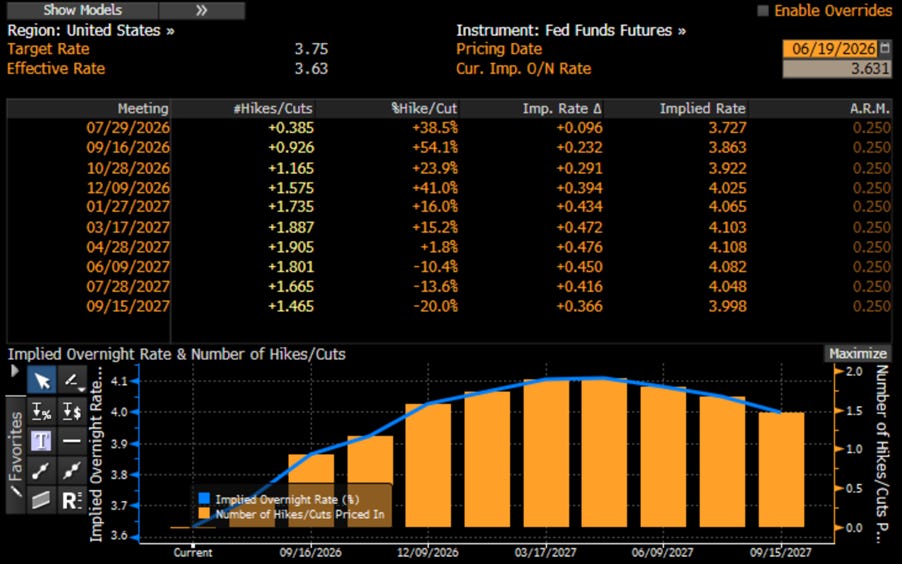

As the first nothing-burger meeting of the new Central Banker-in-Chief fades into history, Wall Street’s endlessly imaginative EYIs have begun the painful process of retiring their enchanted “rate cuts and soft landing” fairy tale — the one that kept FOMO retail investors blissfully misinformed throughout 2026. ‘Warshington’ has discovered, with the surprised expression of a man finding water at the bottom of a swimming pool, that the Fed doesn’t control the cycle — the cycle controls the Fed. The market has wasted no time repricing the inevitable: a 25 basis point rate hike now lands in September with 92% probability, and three hikes are fully expected by year-end with 56% odds, because nothing accelerates monetary reality quite like a Middle East excursion that nobody planned to pay for, an inflation wave nobody planned to acknowledge, and a stagflationary spiral that the consensus spent all year calling “transitory.” The bond market — that tireless, humourless, perpetually correct adjudicator of fiscal reality — has always been the pilot; the Fed has always been the passenger in seat 32B, occasionally leaning forward to ask what altitude they’re flying at and being handed a pamphlet about price stability. The Fed doesn’t set the rate cycle — it just shows up late to announce what the bond market already decided months before.

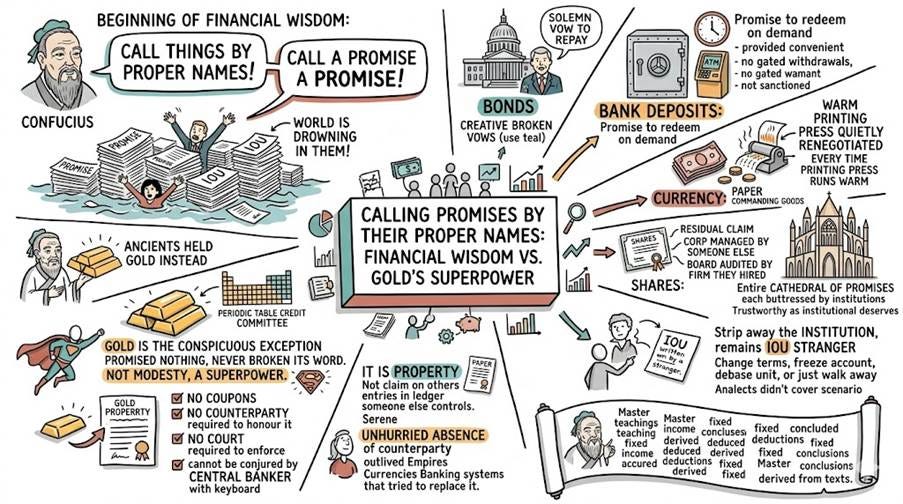

Confucius once observed that the beginning of wisdom is to call things by their proper names. The beginning of financial wisdom is to call a promise a promise — and then to notice that the world is drowning in them. Every financial asset that men have invented is, at its dignified core, a promise.

A bond is a government’s solemn vow to repay — the kind of vow that governments make with great ceremony and break with even greater creativity.

A bank deposit is a promise to redeem on demand, redeemable at any hour of the day, provided the hour is not inconvenient, the bank has not gated withdrawals, and you have not been sanctioned.

A currency is a promise that the paper in your hand will still command goods tomorrow — a promise renewed daily, like a marriage of convenience, and quietly renegotiated every time the printing press runs warm.

A share is a promise of a residual claim on a corporation managed by someone else, governed by a board you did not choose, audited by a firm they hired themselves.

The Master taught that a man of honour keeps his word. Modern finance has instead built an entire cathedral of promises, each buttressed by the institution that issued it, each only as trustworthy as that institution deserves to be — which is to say, some very trustworthy and some, shall we say, aspirationally trustworthy. Strip away the institution and what remains is an IOU written by a stranger who may change the terms, freeze the account, debase the unit, or simply walk away to pursue other opportunities. The Analects do not cover this scenario. They did not need to; the ancients held gold instead.

Gold is the conspicuous exception — the one major asset that promised nothing in the first place and has therefore never broken its word. This is not modesty. It is a superpower. Gold does not pay a coupon. It does not require a counterparty to honour it. It does not need a court to enforce it. It cannot be conjured into existence by a central banker with a keyboard and a mandate to be creative. It is property — not a claim on someone else, not a favour owed, not an entry in a ledger that someone else controls. That single quality — the serene, unhurried absence of a counterparty — is the reason gold has outlived every empire, every currency, and every banking system that has ever tried to replace it. As the Master might have said, had he worked in fixed income: He who trusts no one cannot be betrayed. He who owns gold trusts no one. Draw your own conclusions.

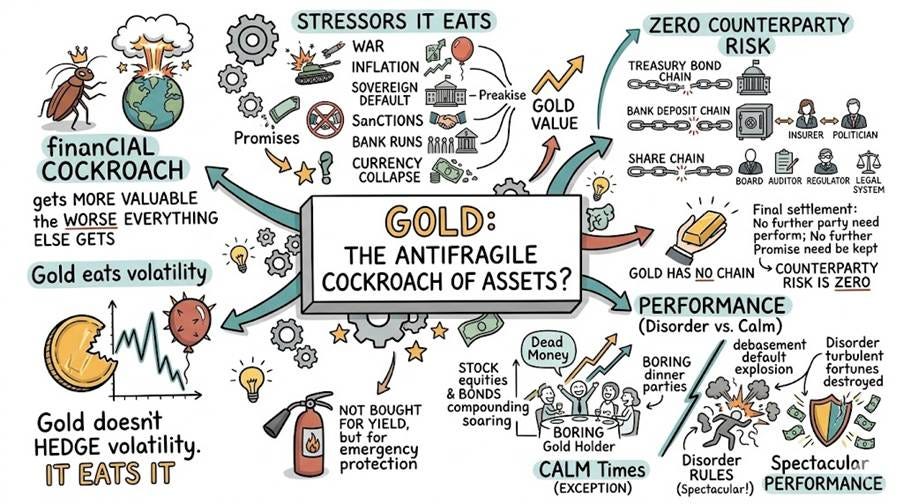

Gold did not survive three thousand years because it is shiny. Many things are shiny. Politicians’ promises are shiny. Leveraged structured products were, briefly, very shiny indeed. Gold survived because it is the only money that no one can default on — the only financial instrument whose credit committee is the periodic table

Nassim Taleb gave us “antifragile“ to describe things that don’t merely survive chaos but grow fat on it. A wine glass is fragile. A paperweight is robust. An antifragile asset is the thing that gets more valuable the worse everything else gets — the financial equivalent of the cockroach that inherits the earth after the nuclear exchange. Gold is that cockroach. War, inflation, sovereign default, sanctions, bank runs, currency collapse: every one of these is a stressor that destroys the value of promises and increases the value of the one asset that isn’t one. Gold doesn’t hedge volatility. It eats it.

The mechanism is counterparty risk — or rather, its total, glorious absence. A Treasury bond chains your wealth to the continued solvency, honesty, and goodwill of the issuing government. A bank deposit chains it to the bank, the deposit insurer, and the political will to honour the scheme when honouring it becomes inconvenient. A share chains it to a board, an auditor, a regulator, and a legal system that will theoretically enforce your claim — eventually, after fees. Every one of these is a chain, and a chain breaks at its weakest link. Gold has no chain. An ounce in your hand is the final settlement: no further party need perform; no further promise need be kept. In the language of risk management, its counterparty risk is zero. In plain language, it’s the asset you hold when you’ve decided to stop trusting strangers with your money.

And yes — over a calm times, gold looks like dead money. It yields nothing while bonds compound and equities soar and everyone at dinner parties tells you how boring you are. But calm decades are the exception in monetary history, not the rule. The rule is debasement, default, and disorder, occasionally interrupted by stretches of stability long enough to make people forget the rule. Gold does poorly in the stability. It does spectacularly in the disorder — and since the disorder is precisely when fortunes are destroyed, the insurance is worth rather more than its average annual return implies. You do not, after all, buy a fire extinguisher for its yield.

US Aggregate Chaos Index (blue line); Gold Price in USD (red line).

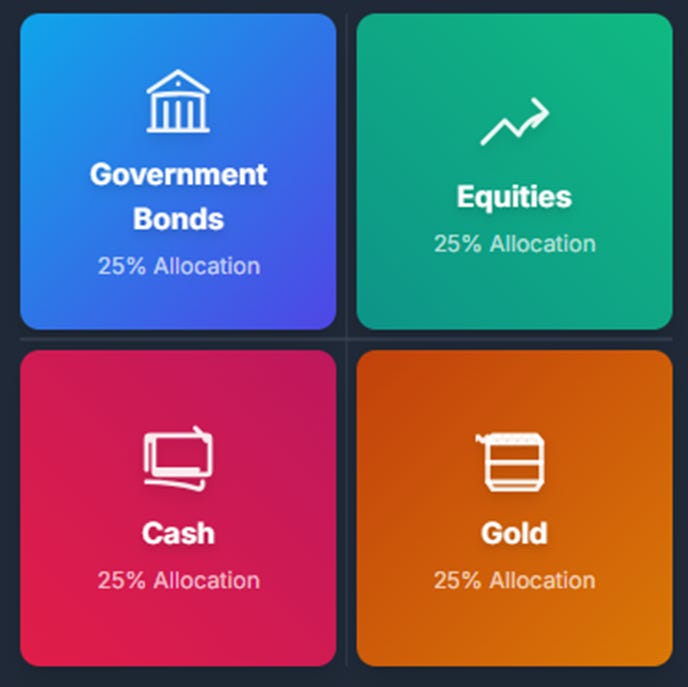

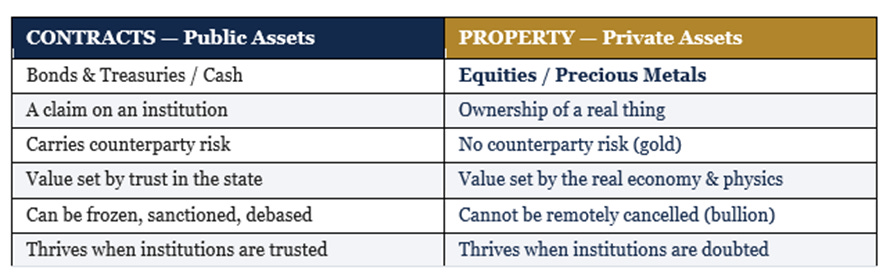

Harry Browne’s Permanent Portfolio — stocks, bonds, cash, gold, one equal slice each — is a fine framework, but there is a simpler cut: forget the four seasons and draw one line instead, the line between contracts and property.

On the left sit the contracts — bonds, cash — which are not really things at all but politely worded IOUs from public institutions, worth precisely as much as those institutions deserve to be trusted, which on a good day is quite a lot and on a bad day is the subject of this newsletter.

On the right sit the property — equities and precious metals — which are ownership of actual, physical, stubbornly real things that continue to exist regardless of what any government decides, prints, freezes, or tweets at 2am. The central insight is this: when the world trusts its institutions, capital migrates left toward the contracts; when it stops, capital migrates right toward the property. Everything that follows in this letter is simply an argument that the migration is already underway — and that gold, the most property-like property of all, is its principal destination.

When trust in public institutions rises, capital migrates toward contracts — people happily lend to the state, hold its currency, and pocket its promises, secure in the belief that the cheque will not bounce. When trust falls, capital moves the other way: out of bonds and cash, into equities and precious metals, from the public side of the ledger to the private one, from claims on institutions to ownership of things. The great wealth-preservation question of our age is therefore not “will there be inflation?” or “where are rates going?” — entertaining as those parlour games are — but the rather more uncomfortable one: do you still trust the institutions whose promises fill your portfolio? For a growing share of the world’s investors and central banks, the honest answer, delivered quietly and in tonnages of gold, is no.

Trust in public institutions does not erode gently, like a sandcastle at high tide. It is broken, suddenly and violently, and the most reliable instrument for breaking it across the whole of recorded history is war. War is expensive in ways that no honest fiscal system can absorb, and so it reliably forces the state into the same three moves it has always made: borrow beyond its means, debase its money to cover what it cannot borrow, and — in the modern, sophisticated variant — weaponize the financial system itself against its enemies, thereby demonstrating to every observer, friendly or otherwise, that the “neutral” plumbing of global finance is in fact a loaded gun kept under the issuer’s counter. Each move is a withdrawal from the reservoir of public trust. Borrowing beyond capacity tells creditors they will be repaid in depreciated money, or not at all, or — imaginatively — both. Debasement tells every currency holder that the unit of account is a moving target, which is a polite way of saying that someone is stealing from them slowly.

Keep reading with a 7-day free trial

Subscribe to The Macro Butler’s Substack to keep reading this post and get 7 days of free access to the full post archives.