Eyes Wide Shut Fed…

What’s behind the numbers?

As expected, the Federal Open Market Committee hit snooze for the fourth straight meeting, keeping rates cozy at 4.25%–4.5%. Powell and friends basically said, “Let’s just see what happens,” as they squint at the data like it’s a magic 8-ball. With war chaos and tariff tantrums piling on, the Fed’s current strategy seems to be equal parts patience and crossed fingers.

As expected, the tariff circus stole the spotlight in the Fed’s latest economic projections and press conference, with officials grudgingly updating their forecasts to reflect what everyone else has been whispering: stagflation is knocking, even if no one at the Eccles Building wants to say the S-word out loud.

Growth for 2025? Downgraded to a sleepy 1.4%. Core inflation? Up to a toasty 3.1%. Unemployment? Yep, that’s creeping up too. But in true Fed fashion, they assure us that inflation will gently float back down to 2.1% by 2027—as if markets, wars, and tariffs will politely cooperate with their spreadsheet fantasies. So, to recap: lower growth, higher inflation, more unemployment... but hey, at least the PowerPoint looked optimistic.

The Fed’s latest dot plot still clings to its fairy tale of two rate cuts in 2025—same as March—proving once again that hope is a monetary policy strategy.

In his press conference, Powell expertly dodged every attempt to pin him down on future rate moves, essentially admitting that no one on the FOMC is betting the farm on their own forecasts. As for the Middle East conflict, he downplayed the impact, noting that since the U.S. no longer relies heavily on the region for oil, the market might just shrug it off—assuming, of course, that geopolitics starts taking Fed talking points seriously.

Adding yet another log to the bonfire of economic uncertainty, the Fed announced—almost cheerfully—that it will keep trimming its balance sheet by $5 billion a month. Because nothing screams “we’ve got this under control” quite like tiptoeing away from a $7 trillion mountain of IOUs with scissors and a prayer.

FED Balance Sheet (blue line); US Unemployment Rate (red line).

Powell’s opening remarks stuck safely to the middle lane, though Bloomberg’s Rate Strategy sentiment gauge picked up a slightly more dovish tilt than in May—fewer hawkish jabs, a bit more feather-soft talk, but still no clear off-ramp in sight.

At the end of the day, the June meeting confirmed what many already suspected: the Fed is eyes wide shut, powerless to steer the economic ship, and likely to lose the looming battle against tariff-fueled stagflation. As for the market’s reaction? A touch more bullish than in May—because investors know the real driver of the business cycle isn’t Powell’s pressers, but good old-fashioned chaos.

Market reactions.

US indices closed with modest changes, led by the Nasdaq outperforming the S&P 500 and Dow, as geopolitics—not the Fed—continues to steer the market narrative.

In money markets, traders—largely ignoring the Fed’s growing irrelevance—have trimmed the odds of a September rate cut to 71% post-Jackson Hole, though they’re still pricing in two cuts by year-end, clinging to the soft-landing dream.

The dollar got a modest bump from the Fed’s statement and Powell’s presser, but it barely registered—still trapped in a tight range and unable to crack the stubborn 100 psychological ceiling.

Gold extended its sideways shuffle as investors remain slow to grasp a basic truth: in an inflationary bust, it’s gold—not stocks or bonds—that keeps your wealth intact. Instead of panicking on rallies, they’d be wiser to treat every dip like it’s on sale.

The US 10-year yield remains in the consolidation patter above its 61.8% Fibonacci Retracement (4.34%) as it is just a matter of time that those with a modicum of common sense realize that the FED and the government’s actions will lead to much higher long-term yields in the foreseeable future as the once upon risk free rate is no more free of risks.

Thoughts.

While Wall Street still clings to the fantasy that the FED can control business cycles, a look at the FED Funds rate and the S&P 500-to-oil ratio reveals a clear pattern: rate cuts often mark the peak of this ratio, and no rate cycle has ever stopped it from falling below its 7-year moving average, signaling the shift from boom to bust.

Upper Panel: FED Fund Rate (purple line); Lower Panel: S&P 500 to WTI ratio (green line); 7-Year Moving Average of the S&P 500 to Oil ratio (red line).

Investors will remember that despite Wall Street's belief the FED can only control the short term rate while long dated interest rates are set by the market and impact the life of every American consumers and businesses as they borrow to buy houses, cars and expand their business at a rate which is dependent of the US 10-Year and 30-Year yields. In no cases the action of the FED on the FED fund rates impacts the evolution of the long-dated yields.

US 30-Year Yield (blue line); US FED Fund Rate (red line) & Correlation.

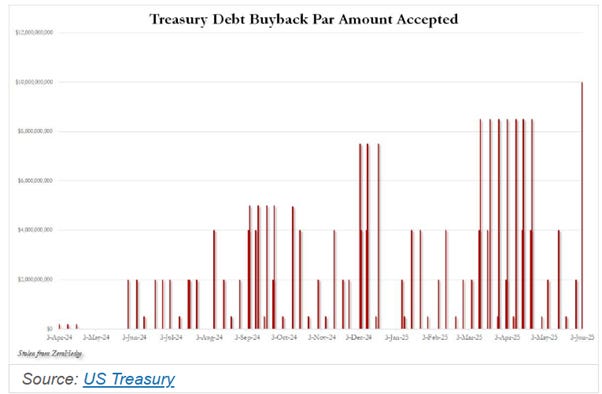

Back in April when the ‘Tariff Tantrum’ was making headlines, as bond yields spiked and rumors swirled that China or Japan were dumping Treasuries and while the $2 trillion basis trade quietly imploded, the ‘Treasurer In Chief’ popped up on Bloomberg to play financial firefighter. He casually mentioned he grabs eggs and coffee with Powell weekly and might "up the buybacks" if the FED stayed asleep.

Fast forward to June: the Fed’s still on mute, yields are dancing near 5%, and voilà—Bessent drops a $10 billion buyback bombshell, the biggest in history. QE-lite? Buybacks for bonds? Call it whatever you like—just don’t call it price discovery.

While the usual suspects—financially allergic journalists and YOLO-touting YouTubers—scream that the $10 billion Treasury buyback is a desperate ploy to save the dollar and stave off economic Armageddon, let’s take a breath. The U.S. Treasury market trades over $900 billion a day. A $10 billion buyback? That’s like a gnat trying to steer a battleship.

Primary Dealer Daily Average Trading Volume In US Government Securities (in million USD)

What’s truly laughable is the chorus of pundits calling the $10 billion Treasury buyback “QE Light”—as if the Treasury could magically print money. It can’t. The Treasury only issues debt: it doesn’t create money. Even actual QE isn’t “money printing” in the literal sense—it’s a duration swap where the FED buys long-term bonds to influence long-term rates, which are ultimately set by the market. The FED only controls short-term rates.

FED Balance Sheet (blue histogram); US 10-Year Yield (red line).

Yet every time, it’s the same tired chorus: "Sell dollars! The end is nigh!"—a song on repeat since Nixon ditched Bretton Woods in ’1971. Meanwhile, the U.S. Treasury market remains the deepest, most liquid on Earth, with everyone from foreign governments to pension funds swimming in it. So no, this wasn’t some ‘Bondpocalypse’ prevention maneuver—it was a routine effort to smooth the debt profile, targeting maturities between mid-2025 and mid-2027. The real kicker? As Powell’s higher-for-longer rates jack up borrowing costs, Treasury’s buybacks are just a quiet admission: Keynesian levers are broken, and the debt beast needs gentler feeding.

In 1995, President Clinton surprised many by balancing the U.S. budget—something that seemed almost magical at the time. But the real trick wasn’t fiscal wizardry; it was global capital flows doing the heavy lifting. After U.S. interest rates spiked in 1994, capital came flooding into America, especially from Japan. This surge was magnified as investors fled Southeast Asia, paving the way for the Asian Currency Crisis of 1997. In short, Clinton didn’t tame the deficit—he rode a tidal wave of foreign capital looking for safety and yield.

FED Fund Rate between 1990 and 2003.

In his April interview with Bloomberg, the ‘Treasurer In Chief’ brushed off fears that foreign central banks were driving a U.S. bond selloff, pointing instead to leveraged position unwinds. The Japanese yen’s April high didn’t even surpass its 2024 peak, and ironically, much of Japan’s U.S. debt holdings are by private institutions hedging against their own government's monetized debt. What the press missed entirely was Bessent’s hint that Treasury buybacks could expand if needed. Reporters asked if he was working with Powell to stabilize the bond market, prompting Bessent to wave off the panic—rightly so. This isn’t new. Clinton balanced the budget in the '90s not through fiscal magic, but by shortening debt maturities to cut interest costs. While the national debt still rose, the shift slowed its pace. Once short-term rates dropped post-Dot-Com bust, the strategy paid off—until rising rates later made it costly.

Meanwhile, mainstream analysts obsess over the Fed, often misunderstanding its role entirely. Conspiracy theories about big banks owning the Fed miss the point: Congress, not the FED, pulls the fiscal trigger. The Fed’s structure was designed to avoid taxpayer-funded bailouts. The real issue isn’t the Fed—it’s persistent deficit spending. History offers a lesson: when Andrew Jackson killed the Second Bank of the U.S., the result was the sovereign debt crisis of the 1840s and the “Hard Times.” The parallels are hard to ignore.

US Public Debt to GDP (histogram); US FED Fund Rate (blue line).

And let’s be clear: debt is money that pays interest. Institutions routinely post T-bills as collateral—even to trade gold futures. Before 1971, borrowing against government debt was illegal, so ironically, it was less inflationary to borrow than to print. Today, it’s the reverse—borrowing against debt fuels inflation more than outright money creation. So, the idea that politicians should control the money supply instead of the Fed is madness. The real problem is the politicians—they’re already the ones creating the debt in the first place.

The Fed's QE wasn’t “money printing”—it was a swap. It bought long-term debt to nudge down long-term mortgage rates during the MBS crisis of 2007–2009. The market, not the FED, sets long-term rates. QE didn’t expand the money supply in any meaningful sense—debt, when it serves as collateral, is already functionally money. There was no inflation explosion in the U.S. or Europe during QE, yet armchair theorists scream "money printing" and MMT fanboys claimed it proved you can print forever without consequences—because they conveniently ignore debt in their definition of money.

In reality, most of today’s "money" is sovereign debt. It pays interest and backs financial markets—T-Bills get posted to trade everything from gold to soybeans. This isn’t the Roman Empire; we’re not trading coins by weight anymore. Western governments are running synchronized Ponzi schemes, and the FED simply swapped cash (that pays no interest) for bonds (that do). Yet the conspiracy crowd is out in force again after the Treasury's $10B buyback—the biggest in U.S. history, they scream—as if that’ll “prop up” the Treasury market or save the dollar from collapse. In reality, $10 billion is a rounding error in a $34T+ debt market with $900B in daily volume. The buyback is about reducing borrowing costs, tweaking maturity profiles, and injecting a bit of liquidity—hardly a crisis response. This is Clinton 2.0. Back in the '90s, Bill played the optics game by shortening the average maturity of debt to lower interest expenses and claim a “balanced budget.” It worked—until rates rose again, and the rollover cost ballooned by 2007.

US Total Debt Outstanding Bills to US Total Government debt (blue line); FED Fund Rate (red line).

Now, Treasury Secretary Scott Bessent—who once criticized Yellen’s short-dated issuance strategy—is running the same playbook with slightly more honesty. The problem? A wall of $5 Trillion in refinancing before the end of the Jubilee Year which is colliding with weak savings and higher rates. And yes, every central bank sees the storm on the horizon as the bell of the Trump Stagflation are already ringing on the horizon.

So, while the Fed-watchers obsess overshadows on the wall, the real game is in the structure and rollover of debt. Sadly, that’s too boring for financial influencers and too complex for the clickbait press.

What we’re likely witnessing is not QE, but a fiscal version of Operation Twist—a maturity rebalancing maneuver historically executed by central banks, not Treasury Secretaries. Traditionally, the FED sells short-term securities and buys long-term ones, aiming to lower long-term yields without expanding its balance sheet. It’s designed to reduce borrowing costs on mortgages and corporate debt while containing inflation risk. But here, it’s the Treasury doing the maneuvering—not to stimulate growth, but to reduce borrowing costs on the front-end while pretending all is under control. Problem is, this isn't 2011. Back then, Operation Twist worked in a low-debt, post-crisis world. Today, the U.S. is running $2 trillion deficits, servicing over $1 trillion in annual interest, and refinancing nearly $9 trillion before the 2025 presidential deadline. The context has changed. This isn’t some tactical tweak—it’s a scramble.

Worse still, we’re not heading into disinflation. We’re staring down stagflation, with war on the horizon, global trade fracturing, and structurally tight commodity markets. Rates are not going back to zero. Any attempt to manage the yield curve through financial engineering is just buying time—not solving anything. The real story is hiding in plain sight: the fiscal side is now being forced into duration management—because the market won’t do it for them at a reasonable price. And if the trend continues, long-term yields will climb as short-term rollover risk becomes unmanageable. Welcome to the endgame of debt monetization in a fractured global order.

Let’s face it: the old idea that lower rates magically spark investment is so last century. Investment actually depends on perceived opportunities, and guess what? The FED has zero control over the real issues—tariffs, wars, taxes, and government spending. As the US economy heads toward an inflationary bust, neither stocks nor bonds will save you once the S&P 500 to WTI ratio dips below its 7-year moving average (probably by mid-2025 when tariffs kick in). So, don’t be shocked by the FED’s impotence. With the S&P/Gold ratio now teetering below its 7-year average, a harbinger of doom for the S&P/WTI ratio in a few months, it’s clear that the FED’s actions won’t do a thing to prevent the US economy from shifting into the Trump Stagflation. US Treasuries? Yeah, they will not be a great store of value compared to gold, the eternal antifragile asset.

Key takeaways.

The FED may remain politically independent, data dependent, but in reality, it’s becoming increasingly irrelevant in the face of global challenges it can’t control.

Variables such as the war cycle and economic uncertainties surrounding the new fiscal policies implemented by the 47th U.S. president will inevitably bring back stagflation sooner rather than later.

In this context, Wall Street must still acknowledge the FED’s impotence in changing the course of the business cycle, as what truly matters is Corporate America’s ability to generate profits based on the cost of energy.

In this context, the misguided Wall Street bankers will once again be wrong in thinking rate cuts will solve economic problems, which will only worsen as the ‘Manipulator In Chief’ thinks he can solve the problems of the US economy and avert the business cycle.

Rising economical; political and geopolitical uncertainties and stagflation will ultimately lead to a stronger USD, higher Treasury yields, and higher oil and gold prices.

As the 47th US president is unable to deliver on his promises of peace and prosperity for anyone outside his plutocratic circle, trust in public institutions (including the FED) will continue to decline, leading investors to move even more into assets with no counterparty risk and which are non-confiscatable, like physical gold silver and platinum.

For fixed-income investors still chasing long-duration trades, more pain awaits, as long-dated yields have not yet reflected the new stagflation reality.

In an inflationary bust, the best way to protect wealth on an inflation adjusted basis is to own a substantial part the portfolio in Physical Gold (at least between 25% to 40%) and avoid long dated bonds.

As the risks of an inflationary bust are rising, investors should also prepare their portfolios for MUCH HIGHER volatility.

In a nutshell, investors should also remain prepared for dull inflation-adjusted returns in the foreseeable future.

Bottom line: The economic theories used by the FED are flawed as they keep ignoring key realities like the global circulation of money, debt dynamics, and the role of public confidence in spending. Economic policies based on academic theories, crafted by those with no real-world experience, will ALWAYS FAIL IN PRACTICE. It's time to implement a new economic theory grounded in the business cycle, one that prioritizes expertise and market data over appearances in leadership and policymaking. We must prevent academics with ZERO real-world experience or trading backgrounds from proposing theories they are NOT qualified to develop. It's akin to a man writing a book on how it feels to give birth—unrealistic and misguided. Economic theory needs a reality check, not another flawed experiment.

In the current environment, investors should allocate at least 30% to 40% of their portfolios in physical gold. Among equities, they should focus on low-leverage companies with sustainable EPS and FCF growth and buy dips in energy producers while selling rips in energy consumers. The Aerospace Defence sector also offers opportunities to buy dips, as the prospects for peace fade. In fixed income, avoid long-dated bonds, especially government bonds with maturities beyond six months, and instead favour investment-grade corporate bonds with maturities under 12 months. As the inflationary bust escalates, replacing long-dated fixed-income assets with physical gold, silver, or platinum will help investors focus on the Return OF Capital rather than the Return On Capital on an inflation-adjusted basis, while maintaining peace of mind during times of war and financial crisis.

Let’s be honest—the Fed, Wall Street analysts, and CNBC still haven't figured out that cycles run the show. They’re like people trying to control the tides with a mop. Meanwhile, economics keeps pretending it’s a science, when really, it’s just fortune-telling with spreadsheets. If they’d just crack open the story of Joseph—yes, that Joseph with the coat and the Pharaoh—they’d get it: seven fat years, then seven lean years. Save during the good times, brace for the bad ones. It’s not rocket science—it’s agriculture with a calendar.

But no, we get endless Keynesian tinkering, top-down "climate salvation" plans that assume Mother Nature runs on a linear Excel chart, and wars that always seem to break out right after everyone maxes out their credit cards and gets too comfortable. Everything has a cycle. Markets. Economies. Even your brain. (No brainwaves? Game over.) But most investors—and yes, our beloved “Central Banker in Chief”—are still squinting at the world like it’s a flat line. The day they finally see the cycle is the day they realize just how little control they actually have. Independence? Please. That’s like calling a hamster in a wheel a free spirit.

If this research has inspired you to invest in gold and silver, consider GoldSilver.com to buy your physical gold:

https://goldsilver.com/?aff=TMB

Disclaimer

The content provided in this newsletter is for general information purposes only. No information, materials, services, and other content provided in this post constitute solicitation, recommendation, endorsement or any financial, investment, or other advice.

Seek independent professional consultation in the form of legal, financial, and fiscal advice before making any investment decisions.

Always perform your own due diligence.