FAT TAILS…

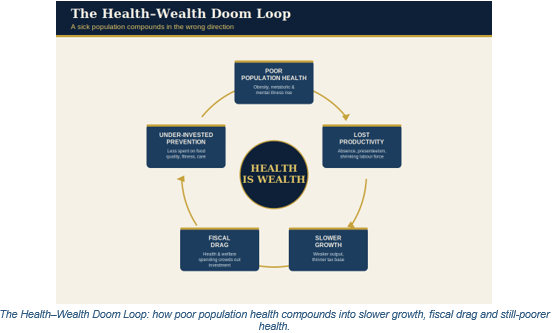

When a nation's health fails, its balance sheet follows — the compounding cost of sickness is coming due.

The Week That It Was…

The week marking Q2’s exit arrived gift-wrapped in holidays: Hong Kong toasted its return to the Middle Kingdom on July 1st while America spent a long weekend celebrating 250 years of independence with barbecues, fireworks, and a $40 trillion national debt. The data calendar delivered another round of forever-misinterpreted ISM Manufacturing and a jobs report that will be revised beyond recognition by September. Of the five S&P 500 companies reporting, only Nike — whose supply chains are hostage to the very Asian factories imperilled by weaponised trade — and Constellation Brands — whose beer-drinking customers are the canary in the stagflationary coal mine — offered any honest read on how stretched the American consumer already is.

The Manipulator-in-Chief issued another Truth Social communiqué from the Ministry of Perpetual Victory, announcing that US aircraft have struck Iranian missile and drone storage sites “AGAIN” for violating the ceasefire agreement — the same ceasefire that was declared a historic triumph approximately one week ago and has since required at least two sets of airstrikes to remain theoretically intact. The post closes with the measured diplomatic warning that “the Islamic Republic of Iran will no longer exist“ if Tehran fails to learn its lesson — a sentence that sits somewhat awkwardly alongside the simultaneous assertion that the war was “very successfully started” and is already complete, raising the entirely reasonable question of what exactly was completed and why it apparently requires ongoing airstrikes, existential threats, and Truth Social posts to stay that way. When your ceasefire requires weekly airstrikes to enforce and a presidential threat of national annihilation to clarify, the peace deal has become indistinguishable from the war it replaced — just with better branding.

The war that was declared won on Hour 1 of Day 1 has produced its most geopolitically clarifying moment yet: over 100 nations — including China, Russia, Pakistan, India, Turkey, Saudi Arabia, Hezbollah, Hamas, and the Taliban — descended on Tehran to pay respects to Supreme Leader Khamenei, assassinated by the US and Israel on February 28 alongside his wife, daughter, daughter-in-law, and grandchild. Over 10 million Iranians are expected in Tehran alone, with millions more gathering in Qom, Mashhad, and across Iraq — a funeral procession spanning an entire civilisation that the ceasefire was supposed to have pacified. The IRGC commander Ahmad Vahidi — unseen for months — emerged publicly for the first time, while Iran’s military explicitly warned Washington and Tel Aviv that any attack on the funeral will be met with “harsh retaliation.” The guest list alone is the geopolitical verdict: when half the world’s nations attend the funeral of the man your coalition assassinated, the war did not isolate Iran — it consecrated it.

https://english.pravda.ru/world/167237-medvedev-tehran-visit-russia-iran/

The Master observes: the man who is deceived by the same ruse twice has not studied history — he has merely lived through it. The Confucian Master Lavrov has now sheepishly admitted that the Anchorage summit, like the Minsk Accords before it, served primarily to buy time for Ukraine to rearm — a revelation that arrives three and a half years after Angela Merkel made the identical confession about Minsk, and approximately one year after Putin, who had famously warned his own strategists against “wishful thinking,” fell into the same trap with the same adversary using the same playbook. The superior man does not fault the river for flowing downhill — he faults the navigator who ignored the current twice. Russia now faces three paths: escalate decisively to end the conflict on its own terms, endure an indefinite war of attrition, or freeze the conflict — none of them the outcome Moscow anticipated when it sat down in Alaska to negotiate with a man who then signed a G7 statement calling for more arms to Ukraine and privately encouraged the Dancer on High Heels from Kyiv to act “more boldly.”

https://www.yahoo.com/news/politics/articles/lavrov-don-t-want-assume-105200822.html

The Ministry of Humanitarian Protection has issued another policy clarification: the 4.4 million Ukrainians currently housed, fed, educated, and employed across Eurostan under the Temporary Protection Directive will continue to receive full benefits — however, military-age men newly arriving from Ukraine will no longer qualify for temporary protection, a measure the European Commission insists is “not discrimination” but which Sweden’s Migration Minister summarised with refreshing candour as ensuring “the war needs to be fought and won“ by keeping more men in Ukraine to die in it.

The compassion that opened Europe’s borders in 2022 has discovered, after four years of bleeding, that ammunition can be manufactured but young men cannot — and with 200,000 soldiers having gone AWOL, two million Ukrainians wanted for draft evasion, renunciation of citizenship made illegal under martial law, and an unelected president demanding men aged 25 to 60 report for “rotation,” Europe has quietly transitioned from offering protection from Tsar Vladimir to facilitating conscription for the Kyiv Cokehead. The Ministry of Truth frames this as solidarity; the men boarding buses to the front line may use a different word. When the humanitarian protection directive becomes a mechanism for closing the escape routes, the refugees weren’t being sheltered from the war — they were being held in reserve for it.

The Ministry of European Solidarity has a minor budget clarification: the EU has transferred another €3.9 billion to Ukraine specifically for drone procurement, part of a broader €90 billion loan programme designed to keep Kyiv funded through 2027, bringing total European support to €211.3 billion since the war began — a figure delivered with the straight face of an institution whose member states cannot balance their own budgets, fund their own pensions, or explain to their own citizens why electricity bills doubled.

https://www.reuters.com/world/eu-sends-ukraine-39-billion-fund-drones-under-loan-deal-2026-06-30/

Brussels insists this is not war financing but solidarity — the same solidarity that has censored dissent about the war, restricted military-age Ukrainian men from refugee protection to keep them available for conscription and is now building what can only be described as the financial architecture of a permanent war economy. The sanctions that were supposed to collapse Russia in weeks have instead pushed Europe into depressionary conditions, yet the prescription remains identical: more loans, more drones, more debt, and the serene confidence of an institution that has never been held accountable for a single forecast it got wrong.

The Ministry of Democratic Warfare has unveiled its most innovative product yet: a monetised kill system in which Ukrainian soldiers receive $330 for a confirmed enemy kill and $2,200 for a live capture — a pricing structure that assigns human lives the same transactional logic as a corporate bonus scheme, complete with video verification requirements and group-split provisions for collaborative eliminations. The e-Points system goes further still: units earn points for confirmed destruction of enemy personnel and equipment, redeemable through the Brave1 marketplace for drones, electronic warfare systems, and robotic ground platforms — essentially a loyalty card programme for killing, where enough confirmed kills earns you the upgrade that helps you confirm more kills. Ukraine’s Defence Minister celebrated this as “clear incentives and fair rewards,” which is the Ministry of Truth’s preferred framing for what military historians would recognise as a bounty system, and what Call of Duty players would recognise as a killstreak reward. The same Western governments currently lecturing the world about rules-based international order and the protection of human dignity are financing, with $211 billion in European funds alone, a battlefield that has been reduced to a performance dashboard where the dead are data points and the living are assets awaiting monetisation.

The PLA of 2026 is not the PLA of 2013 — it is a fundamentally different force, oriented around defeating the United States in a high-intensity regional conflict over Taiwan, and the Great Master Xi has now directed it to accelerate further, because apparently the world’s largest military modernisation programme — backed by an official defence budget of $247 billion and estimated actual spending closer to $471 billion — is proceeding at an insufficiently urgent pace. The Ministry of Peaceful Rise has issued its 15th Five-Year Plan, formally prioritising the PLA’s transition toward “intelligentised” warfare — the Orwellian rebranding of AI-enabled autonomous killing systems as a Five-Year Plan deliverable — while Xi has ordered the military to be capable of seizing Taiwan by force by 2027, a deadline now approximately twelve months away. The timing is exquisite: the US has just spent three months exhausting munitions, draining its strategic petroleum reserve, destroying its Gulf bases, and discovering that its defence industrial base cannot restock fast enough — while Beijing, having observed every operational lesson of the Middle East campaign from a ringside seat, is directing its military to move faster toward the one theatre Washington has been too distracted to reinforce.

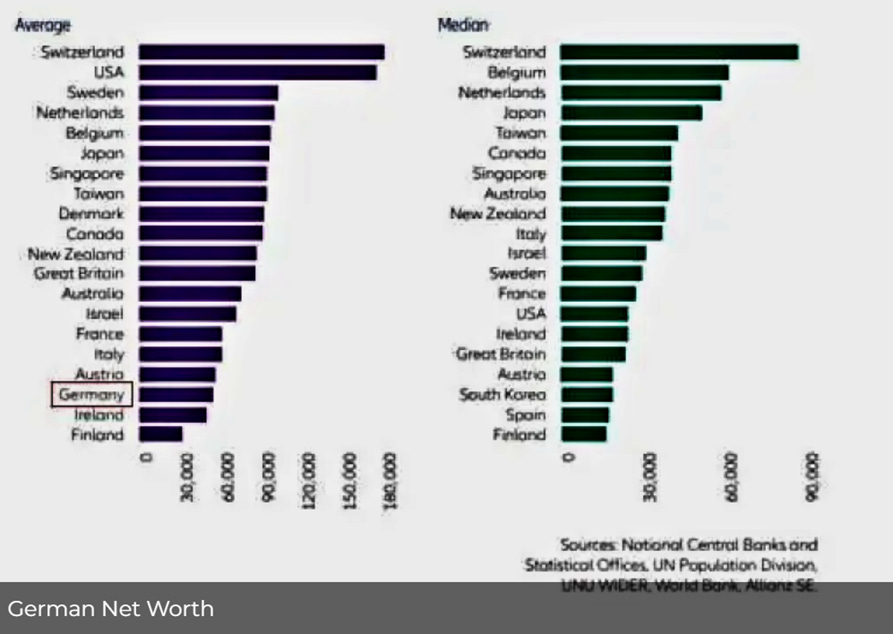

Volkswagen — the crown jewel of German engineering and the company that once dominated China — is now reportedly considering cutting up to 100,000 jobs while closing factories and restructuring its entire business, following a 53% collapse in operating profit despite revenue holding steady, with global deliveries falling another 4% in Q1 2026 including a 15% decline in China and a 20.5% crash in the United States.

The culprits are well known to anyone who wasn’t in Brussels: Germany shut down nuclear power and energy costs exploded, regulators piled impossible climate targets onto manufacturers, governments forced billions into EVs before consumers wanted them, China developed superior models at half the price, and the average German citizen now has a lower net worth than residents of Southern European nations — a sentence that would have been considered satire a decade ago. The punchline writes itself: China has even bid to acquire the shutdown VW factories within Germany itself, meaning the nation that spent years lecturing the world on industrial policy is now entertaining offers from the competitor its own policies gifted the market to.

The Ministry of Smart Living has a clarification for anyone who dismissed the 2012 Wired headline “CIA Chief: We’ll Spy on You Through Your Dishwasher“ as paranoid fantasy: that was not a conspiracy theory — it was then-CIA Director David Petraeus speaking at an In-Q-Tel summit, calling connected home devices “transformational” for “clandestine tradecraft” and confirming that “items of interest will be located, identified, monitored, and remotely controlled” through RFID sensors, embedded servers, and internet-connected appliances. They did not hide it — they announced it at a conference, published it in a major technology magazine, and then waited patiently while the public bought the devices, installed the apps, connected everything to Wi-Fi, and signed away their privacy in user agreements nobody reads. The architecture has since expanded precisely as advertised: licence plate readers now simultaneously harvest smartphones, smartwatches, Bluetooth devices, infotainment systems, AirTags, and pet microchips — your television, thermostat, refrigerator, car, watch, and dog now function as a distributed surveillance network that would have required a team of agents and a court order to replicate in 1984. The rollout followed the Ministry’s preferred sequencing: first smart technology, then public safety, then national security, and eventually total surveillance — each step individually reasonable, the aggregate a totalitarian’s operational manual delivered gift-wrapped with a monthly subscription fee.

https://www.wired.com/2012/03/petraeus-tv-remote/

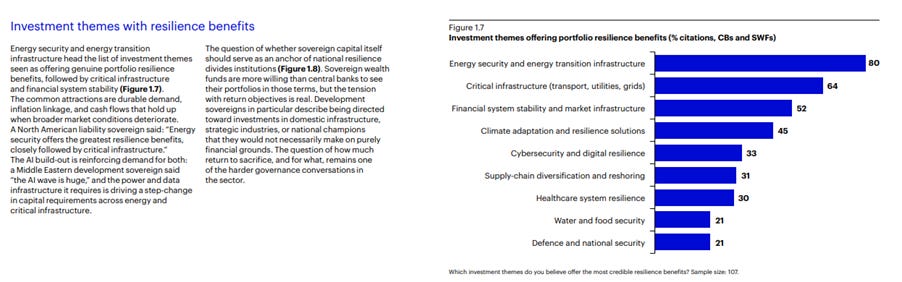

In a survey that will surprise nobody who has been paying attention, sovereign wealth funds and central banks managing a combined $29 trillion have concluded that energy assets are the most credible investment for portfolio resilience, infrastructure has reached 9% of sovereign wealth fund allocations, and 61% of central banks polled openly admitted that US debt levels negatively impact the dollar’s long-term reserve status — which is the diplomatic way of saying the world’s most important investors are quietly diversifying away from the Empire’s IOUs while continuing to attend its dinner parties. The same institutions that spent decades dutifully recycling petrodollars into US Treasuries have apparently noticed that trade tariffs, closed shipping channels, weaponised sanctions, and a $40 trillion debt trajectory make “risk-free” a somewhat optimistic description. The positive bond-equity correlation of recent years has further eroded bonds’ diversification appeal, pushing sovereign investors toward real assets and liquidity — which is the $29 trillion community’s elegant way of confirming what we have been saying all along: own producers of scarce things, hold gold, and treat the once-upon-a-time risk-free asset with the caution it has now thoroughly earned.

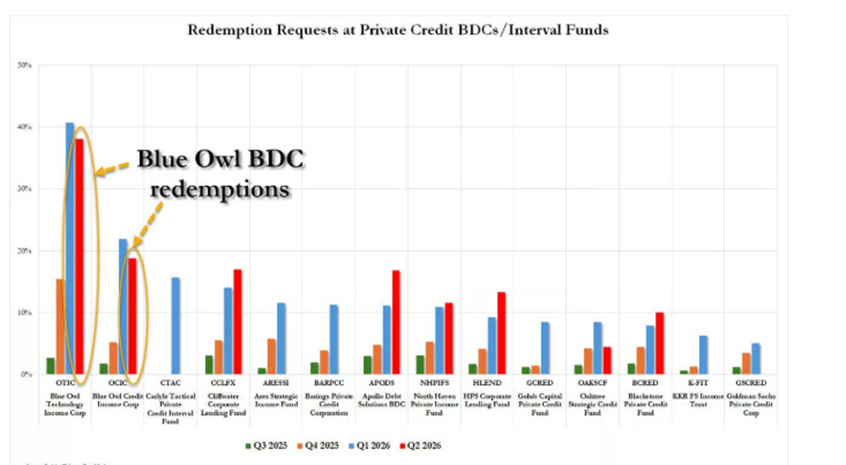

In a development that will stun precisely nobody who noticed that Apollo, BlackRock, Blackstone, Ares, and Cliffwater have all already gated their investors for a second consecutive quarter, Blue Owl has joined the another round of the redemption gate parade after investors in its $34 billion Credit Income Corp attempted to withdraw 18.8% — $3.6 billion — while the smaller Technology Income Corp saw a spectacular 38.1% redemption request, suggesting that “limited exposure to software disruption” was not the reassurance it was marketed as. Blue Owl executives, in what the article charitably describes as a “roadshow,” spent the quarter flying around the world explaining to investors why their money is safe in a fund they cannot leave — a persuasion effort so successful that redemption requests barely declined from Q1’s record levels despite the stock market staging a historic rebound. The firm helpfully noted that “OCIC does not need to sell a single private loan to satisfy the tender offer” — a sentence that reads considerably less reassuringly when the tender offer cap means most investors aren’t getting their money back anyway — and then announced it had acquired a stake in the Cleveland Cavaliers, which is apparently the alternative asset management industry’s preferred response to an existential liquidity crisis.

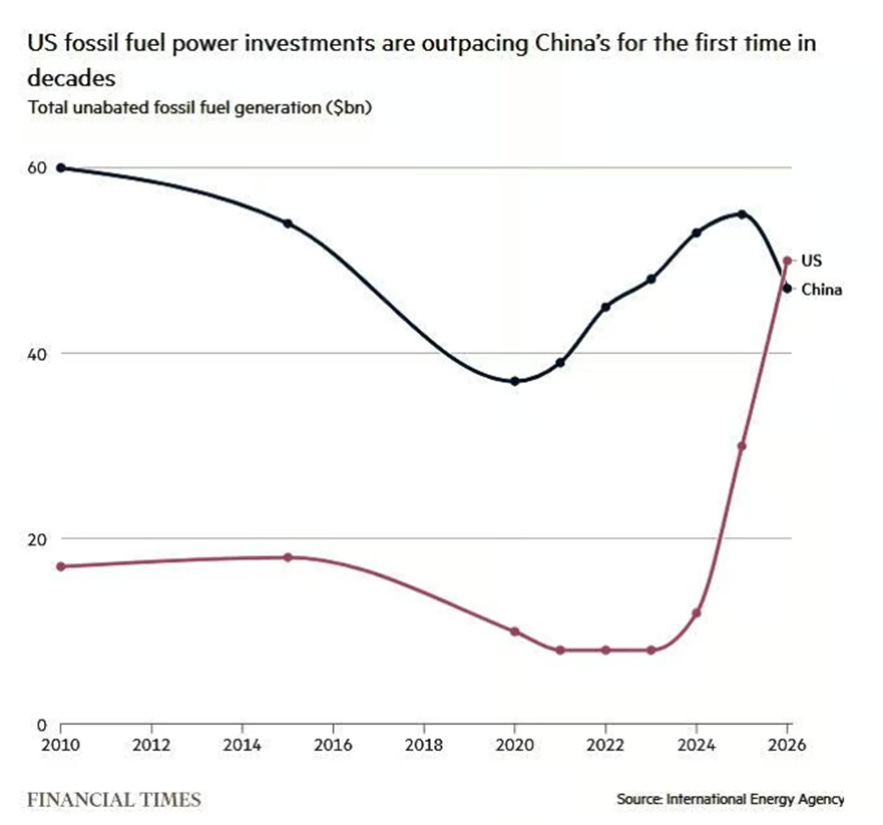

In a magnificent plot twist that will require considerable explaining at the next climate summit, America is set to spend $50 billion on coal and gas power generation this year — more than China, for the first time in decades — because the AI revolution that was supposed to usher in a clean, digital, weightless economy has turned out to require rather a lot of electricity generated by burning things. US companies ordered 20 gigawatts of gas turbine capacity in Q1 alone, gas turbine prices have tripled from $800 to over $2,500 per kWh on supply constraints, and Siemens, GE, and Mitsubishi are scrambling to double production capacity — proof that the data centre boom is doing more for fossil fuel investment than any energy policy since the Texas oil rush. The same Silicon Valley evangelists who spent a decade promising to save the planet with software are now the largest single driver of coal and gas infrastructure investment in human history, while wind and solar — unable to keep the grid balanced when the weather is uncooperative — are ironically fuelling demand for the very baseload fossil fuel capacity they were supposed to replace. The AI revolution didn’t kill fossil fuels — it became their most enthusiastic customer.

The Eternal Bullion spent the final days of Q2 testing the patience of the faithful — plunging to $3,955 on the evening of June 29 with the theatrical despair of a student who has failed his examination — only to rise from the ashes like a phoenix that had merely been resting its wings. The chart reveals a classic V-shaped reversal so textbook it could be taught in the Academy: from the June 29 low, gold climbed relentlessly through $4,050 resistance on July 1, consolidated briefly to gather its breath on the morning of July 2 — as the wise man pauses before ascending the final flight of stairs — and then surged to $4,208 before settling at $4,187, up +2.66% from the June 26 close and +$108.60 in five sessions. The superior man notes two things the chart whispers but does not shout: first, the June 30 low was higher than the June 29 low, meaning each dip attracted more buyers than the last; second, gold has now decisively reclaimed the $4,075 average — the orange dotted line the bears had been clinging to as proof of weakness. Confucius reminds us: the tree that bends in the storm does not break — it stores the energy for the spring. He who sold gold at $3,955 because it was falling now watches from the riverbank as the Eternal Bullion crosses $4,200 without looking back.

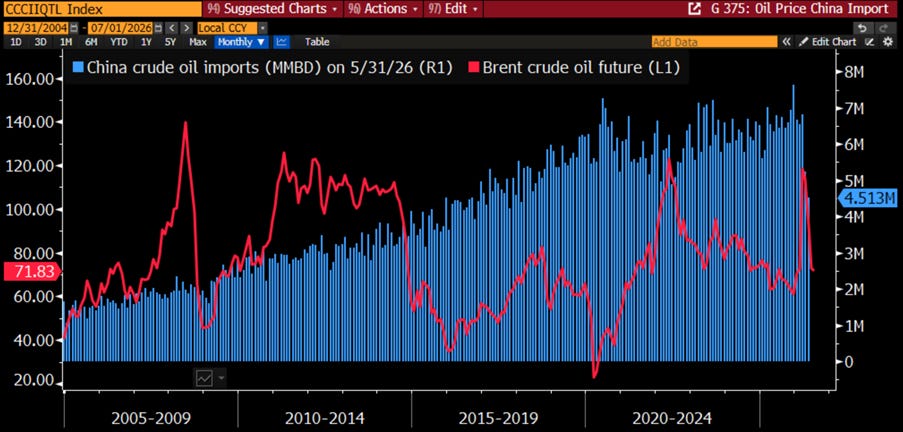

The Master observes: when the world’s largest consumer of oil imports fewer barrels than at any point in recent history while the price of those barrels sat at its highest in half a decade, the wise investor does not celebrate — he asks when the wise man will be filling the storage tanks again. The chart, which never lies, delivers a quietly devastating verdict on the “oil glut” narrative currently soothing Western markets: China’s crude imports reached a record 7.6 million barrels per day in early 2026 before settling at a still enormous 4.513 million as of May 31. The superior man recognises this divergence immediately: Beijing was not panic buying while the Strait was closed, as oil was not cheap then. Now that the Strait of Hormuz is temporarily less lethal than it has been over the past two months, and the ancient art of filling the granary during the harvest applies equally well to strategic petroleum reserves, the wise man will expect Chinese oil imports to reaccelerate — and put a floor under the price of oil that has erased all of its geopolitical premium. He who fills his storehouse when prices are low does not fear the winter — he fears only the fool who sells him the grain and calls it a bear market.

China oil Imports in million barrels per day (blue histogram); Brent Crude Price (red line).

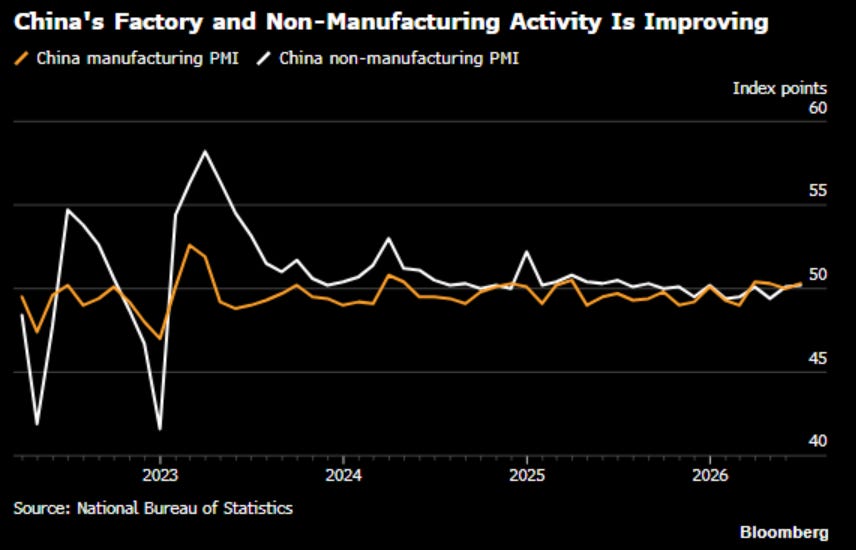

China’s June manufacturing PMI heroically crawled back above the expansion threshold to 50.3 from May’s precarious 50.0, while non-manufacturing surprised with a 50.2 — the kind of barely-positive readings that get celebrated as “moderately positive surprises” when the alternative is contraction. The high-tech PMI of 53.5 is doing virtually all the heavy lifting, while overall employment and inventories continue slumping, prompting economists to describe the recovery as “uneven” — diplomatic code for “the parts that matter to ordinary Chinese workers are still shrinking.”

Exports remain the only functioning engine, propped up by the AI supercycle and export prices rising at their fastest pace in three years, even as the EU prepares fresh countermeasures against the export flood and the PBOC quietly cut its overnight rate below expectations — a de facto easing move dressed up as a technical adjustment. The economy isn’t recovering; it’s being kept on life support by foreign demand for chips while domestic consumption continues its post-pandemic-era retreat.

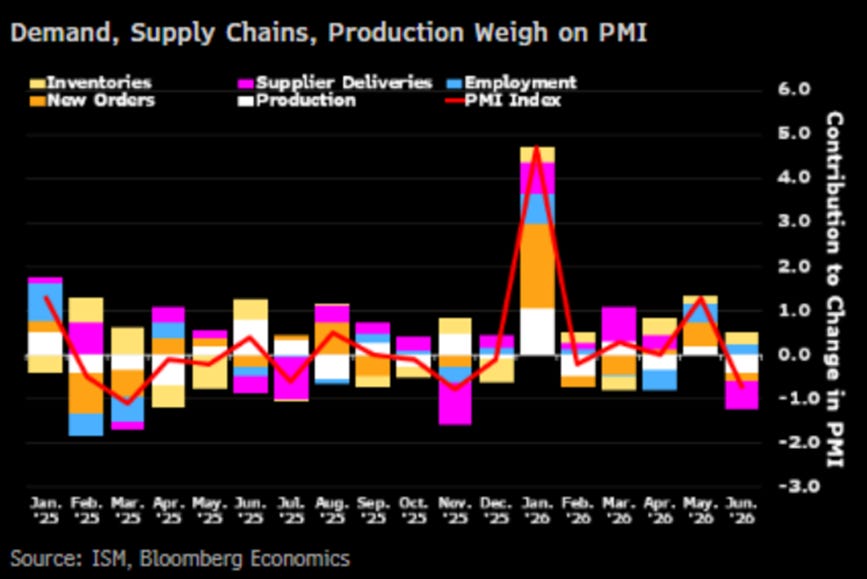

June’s US manufacturing data arrived wrapped in the usual “sixth straight month of expansion” ribbon — S&P Global’s PMI dipping from 55.1 to 53.9 and ISM sliding from 54.0 to 53.3, both missing estimates and both still conveniently above 50, which is apparently the only number that matters when writing fake news. The headline strength conceals the same structural rot identified last month: output is expanding because firms are panic-building inventory ahead of the next supply disruption, employment is being “cut sharply” as companies simultaneously celebrate growth while firing the people producing it, and business confidence has fallen sharply on the entirely reasonable concern that once the war-driven stockpiling binge ends, the demand holding everything together evaporates with it. The prices-paid index delivered its largest single-month drop since July 2022 — celebrated as evidence that inflation is cooling — courtesy of the Iran MoU sending oil prices lower, which is the data’s polite way of saying that the manufacturing expansion is as durable as the peace deal underpinning it, currently being maintained by alternating drone strikes and diplomatic communiqués.

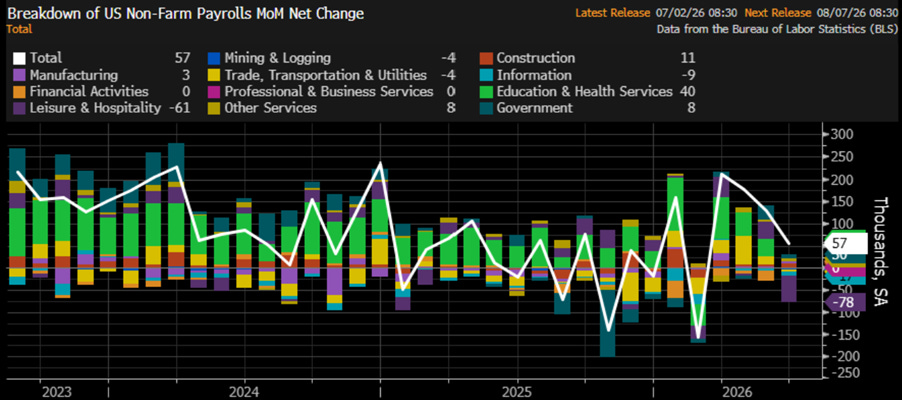

June’s jobs report delivered the kind of number that sends S&P 500 futures higher and rate-hike bets lower — which tells you everything about what the market has become: a machine that celebrates bad news as evidence the Fed won’t tighten. Nonfarm payrolls came in at a deeply unimpressive 57,000 — roughly half the consensus of 113,000 and the weakest print in recent memory — after downward revisions to the prior two months ensured the disappointment was fully retroactive. The sectoral detail is equally flattering: leisure and hospitality posted its biggest payroll decline since 2020, retail and information shed jobs, Big Tech is firing people to fund the AI that is replacing them, and information payrolls have now fallen in 17 of the last 18 months — a streak so consistent it has stopped being a trend and started being a structural verdict.

The unemployment rate fell to 4.2%, not because more people found work but because labour force participation plunged to its lowest level in over five years, the statistical equivalent of declaring the search party a success by sending fewer people into the forest.

Upper Panel: US Unemployment Rate (blue line); US Unemployment 2-Year moving average (green line); Lower Panel: S&P 500 to WTI ratio (yellow line); US S&P 500 to WTI Ratio 7-Year moving average (red line).

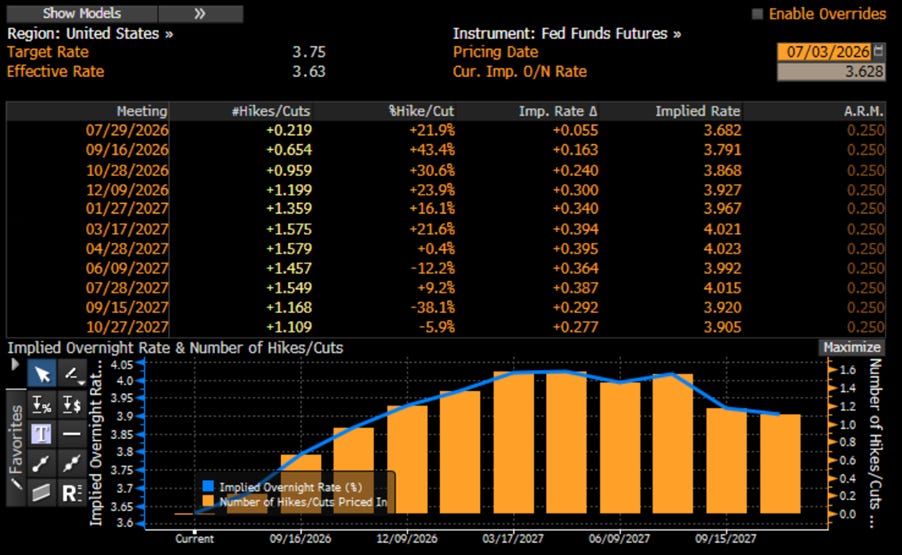

As, Wall Street’s endlessly imaginative EYIs have begun the painful process of retiring their enchanted “rate cuts and soft landing” fairy tale — the one that kept FOMO retail investors blissfully misinformed throughout the first half of 2026. ‘Warshington’ has discovered, with the surprised expression of a man finding water at the bottom of a swimming pool, that the Fed doesn’t control the cycle — the cycle controls the Fed. The market has wasted no time repricing the inevitable: a 25 basis point rate hike now lands in September with 65% probability, and three hikes are fully expected by year-end with 19% odds, because nothing accelerates monetary reality quite like a Middle East excursion that nobody planned to pay for, an inflation wave nobody planned to acknowledge, and a stagflationary spiral that the consensus spent all year calling “transitory.” The bond market — that tireless, humourless, perpetually correct adjudicator of fiscal reality — has always been the pilot; the Fed has always been the passenger in seat 32B, occasionally leaning forward to ask what altitude they’re flying at and being handed a pamphlet about price stability. The Fed doesn’t set the rate cycle — it just shows up late to announce what the bond market already decided months before.

As the Empire celebrates 250 years of independence with barbecues, fireworks, and a $40 trillion debt tab, a Reuters/Ipsos poll delivers the party’s most inconvenient appetiser: nearly one in five Americans won’t bother celebrating, and two in five doubt the republic will survive another 250 years — a vote of no confidence delivered not by foreign adversaries but by the citizenry itself. Only 29% of ‘Dumbocrats’ report being proud to be American, versus 90% of Republicans, and just 36% of adults under 34 expressed any national pride at all — a generation that simultaneously despises its own founding while exercising the constitutional freedoms that founding uniquely guarantees. The pattern is as old as Rome: empires do not fall because the barbarians at the gate are strong — they fall because the citizens inside stop believing the walls are worth defending. Unsustainable debt, inflation, declining living standards, and institutional collapse do not create political division — they are the accelerant poured on divisions that were already there, waiting for a match. The Empire’s greatest threat was never China, Russia, or Iran — it was always the slow, self-administered discovery that half the country no longer agrees on what it is celebrating, or whether it should celebrate at all.

https://www.the-independent.com/news/world/americas/us-politics/america250-independence-trump-divisions-pennsylvania-b3004933.html

The Empire’s greatest threat was never China, Russia, or Iran — it was always the slow, self-administered discovery that half the country no longer agrees on what it is celebrating, or whether it should celebrate at all.

As another unmistakable sign that the Empire is approaching its twilight years, the Megalomaniac-in-Chief has once again floated the idea of having his face engraved alongside the Founding Fathers on Mount Rushmore — because apparently winning one election, losing another, winning a third, starting a war he declared won in an hour, draining the strategic petroleum reserve to its lowest level since 1983, and presiding over the inevitable stagflation that bears his name is the modern equivalent of drafting the Constitution and purchasing Louisiana.

A nation does not go broke all at once. It goes broke the way a body does: slowly, then suddenly, one quiet compromise at a time — a skipped vegetable here, a deferred check-up there — until the bill arrives with compound interest and no instalment plan.

The World Health Organization nailed what is health back in 1948 and has been coasting ever since: health is complete physical, mental and social well-being — not merely the absence of disease, which means not being in hospital is the bar you clear, not the trophy you win. Think of it as a capital account, because it behaves exactly like one — it compounds, with every salad, walk and decent night’s sleep a deposit, and every drive-thru, all-nighter and “I’ll start Monday” a withdrawal. The account pays interest in both directions, and the statement, cruelly, only arrives in your sixties, by which point the early withdrawals have done their quiet, compounding damage. The cosmic joke is that it’s the one balance sheet you can’t outsource, refinance or hand to a wealth manager: he can rebalance your portfolio, but he cannot rebalance your pancreas.

https://apps.who.int/gb/bd/PDF/bd47/EN/constitution-en.pdf?ua=1

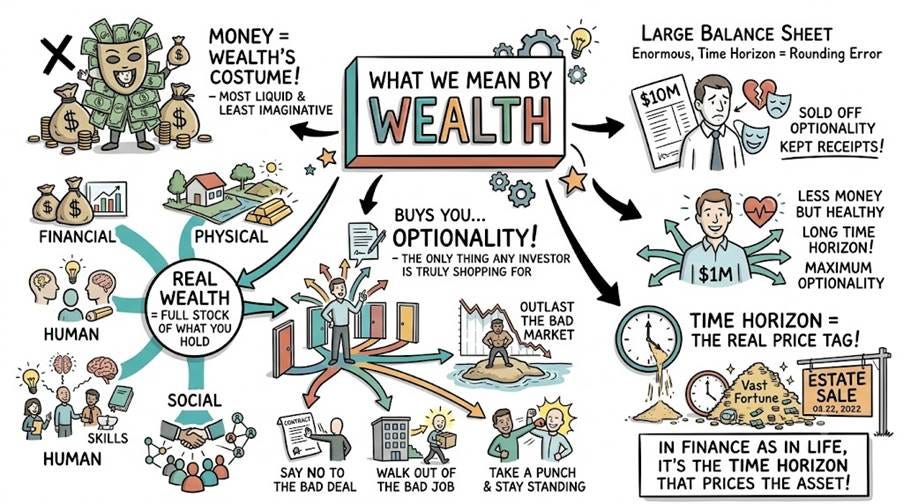

Wealth, properly understood, is not a pile of money — money is just wealth’s most liquid and least imaginative costume. Real wealth is the full stock of what you hold, financial, physical, human and social, and what it buys you is the only thing any investor is truly shopping for: optionality. The freedom to say no to the bad deal, to outlast the bad market, to walk out of the bad job, to take a punch and stay standing. Which is why a man with ten million dollars and a failing heart is poorer than a healthy man with one, because he has quietly sold off all his optionality and kept only the receipts. No amount of money buys back the years his arteries have already foreclosed on — his balance sheet is enormous, and his time horizon is a rounding error, and in finance as in life, it’s the time horizon that prices the asset. A vast fortune on a short clock is just an estate sale waiting for a date.

“Health is wealth“ usually turns up embroidered on a cushion, which is a shame, because underneath the needlework it’s a hard statement about human capital — the productive capacity bundled inside people, and, by most national-accounts estimates, the single biggest line in a nation’s wealth, worth more than all its buildings, machines, land and financial assets combined. A country is, in the end, just a portfolio of human beings, and its long-run growth is the weighted return on that portfolio. Which brings us to the one holding nobody can rebalance out of: your own body. You can’t short your metabolism and go long someone else’s, you can’t hedge your hippocampus, and there is no liquid secondary market in working kidneys for the prudent man to tap when his own hand in their notice. Health is the only asset you own that is non-fungible, essentially uninsurable, and required to enjoy every other asset you’ve got — which makes a villa you can no longer climb the stairs of exactly what it sounds like: a liability with a sea view.

This is why health and wealth aren’t merely correlated, to be noted in passing and filed under “obvious.” They’re a feedback loop — a doom loop when it turns negative, a virtuous circle when it turns positive. Healthy populations work longer, learn faster, save more and cost their governments less, freeing up capital to invest in making the next generation healthier still. Sick populations run the same machine in reverse, and the loop tightens with every turn. Investors spent their careers watching investors hunt for the next great secular trend across exotic asset classes and faraway markets, when the thing has been sitting on the dinner plate the entire time, going cold.

Like it or not, you are, with apologies to the poets, largely a reassembled pile of your recent grocery decisions. Every cell you’re running on was built from something that came off a plate, which means your body is less a temple than a construction site working strictly with whatever materials you keep delivering. Send it olive oil, fish and vegetables and it quietly builds something that ages well. Send it a decade of beige, deep-fried rectangles engineered in a lab to be impossible to stop eating, and it builds accordingly, then mails you the structural survey somewhere around fifty. The inconvenient punchline is that there’s no separate “health” account you can fund later to offset the diet — the food is the health, paid in real time, three times a day, whether or not you’re reading the receipt.