The Global War for Chips

AI and geopolitics are colliding in The Global War for Chips — because the 21st century belongs to whoever controls the silicon.

The Week That It Was…

The second week of Q2’s second month delivered another episode of “CPI: Creative Pricing Index,” with both China and the United States releasing inflation data as supply shortages continued to build. Investors also received a fresh read on the resilience of the American consumer through April retail sales, while a relatively quiet earnings calendar shifted attention toward MOS and Cisco Systems.

While the Empire continued enforcing the blockade of the blockade to encourage Tehran’s “voluntary cooperation,” Iran appeared to play a card that Donald Copperfield never included in the script. A massive oil spill emerged near Kharg Island, the terminal handling roughly 90% of Iran’s crude exports, with satellite imagery from May 6–8 showing a spreading slick covering tens of square miles across the Persian Gulf. The official cause remained “under investigation,” naturally, but the timing fuelled speculation that Tehran may have decided that if sanctioned oil can no longer be stored or sold freely, it can at least be redistributed environmentally. In the grand Orwellian energy transition, the theocracies of Washington, Tel Aviv, and Tehran continued preaching morality while conducting geopolitics through blockades, shortages, and floating crude oil.

In yet another blessed chapter of the “rules-based order,” the UAE appears to be moving ever closer to the sacred alliance of Washington and Tel Aviv, where every geopolitical manoeuvre is conveniently baptized as “security,” “innovation,” and “regional stability.” What was marketed to the faithful as a historic peace breakthrough increasingly resembles a strategic merger between surveillance technocracy and permanent conflict management, complete with AI-powered governance, expanding military coordination, and enough digital oversight to make Orwell look underprepared. And as if to confirm the holy communion, reports now suggest Israel deployed Iron Dome systems and IDF personnel directly on UAE soil during the conflict to help shield the kingdom from Iranian retaliation. Naturally, the high priests of geopolitics assure us this is all perfectly normal, deeply democratic, and absolutely unrelated to the gradual construction of a deluxe 21st-century security state with biometric features included.

https://www.cbsnews.com/news/netanyahu-united-arab-emirates-mbz/

In what future historians may politely describe as the Empire’s “final harmony tour” through the Middle Kingdom, Donald Coppergfield arrived in Beijing accompanied by America’s Tech Bro aristocracy to exchange ceremonial smiles with Xi Jinping while both sides quietly measured the distance to the next crisis. The Great Mandarin Xi declared relations “stable,” which in diplomatic Confucian usually translates to: “we are not arguing loudly today.” Discussions covered oil flows, trade access, fentanyl, agriculture, semiconductors, and the sacred modern principle that global peace depends entirely on keeping container ships moving through the Strait of Hormuz. Meanwhile, CEOs from Tesla, Apple, Boeing, and NVIDIA followed closely behind like wealthy disciples seeking enlightenment through supply chains. Xi ultimately invoked the “Thucydides Trap,” gently reminding both empires that when rising powers and aging hegemons compete too aggressively, history tends to turn philosophy lectures into naval exercises.

The “Thucydides Trap” refers to the idea that war becomes increasingly likely when a rising power begins challenging an established dominant power. The concept originates from Thucydides, who argued that the Peloponnesian War became unavoidable because of “the rise of Athens and the fear that this instilled in Sparta.” In modern geopolitics, the term is frequently used to describe tensions between the United States and China — a rising economic and military power confronting an aging global hegemon increasingly determined to preserve its dominance. History suggests that when ambition meets fear, empires often stop speaking the language of diplomacy and begin speaking the language of military budgets.

https://www.hks.harvard.edu/publications/destined-war-can-america-and-china-escape-thucydidess-trap

Meanwhile, the official White House scripture described the summit as a glorious triumph of “stability,” “cooperation,” and carefully choreographed optimism:

“Trump had a good meeting with Xi.”

Naturally, the propaganda liturgy concluded that all tensions are under control, trade relations are improving, and geopolitical rivalry can apparently be solved with soybeans, crude oil, and sufficiently enthusiastic press releases.

And of course, no imperial pilgrimage would be complete without a triumphant post on Truth Social from “Donald Copperfield” himself, graciously inviting Mandarin Xi to the White House while simultaneously hinting at launching Season 2 of the Epic F**k Up before Air Force One had even departed the capital of the Middle Kingdom. Nothing captures modern diplomacy quite like smiling for cameras, praising “historic cooperation,” and threatening the next trade, tech, or geopolitical escalation before the jet engines finish warming up — especially when both empires are quietly competing to dominate the world before the next decade even begins.

https://truthsocial.com/@realDonaldTrump/posts/116575104401917058

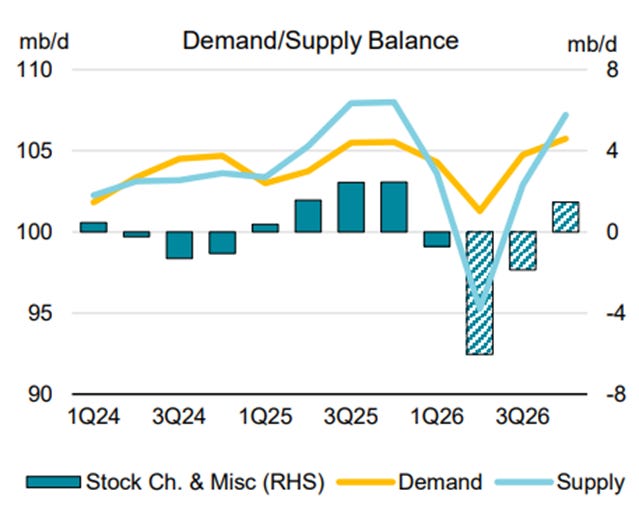

In a shocking development absolutely nobody who passed Economics 101 could have predicted, the IEA has discovered that shutting down major oil flows during a Middle East war may create… an oil shortage. The agency now expects global oil demand to outpace supply by 1.78 million bpd in 2026, with roughly 10.5 million bpd of Gulf production offline and the Strait of Hormuz closure hammering refinery operations, jet fuel production, and global supply chains. Apparently “energy transition” slogans do not magically replace missing barrels. The IEA also warned markets could remain severely undersupplied through Q3, even assuming the conflict ends soon, while refinery throughput collapses under infrastructure damage and feedstock shortages. Translation: higher oil prices, slower growth, demand destruction, and another inflation surprise are no longer risks — they’ve already RSVP’d.

According to the IEA, global oil inventories are now projected to collapse by 8.5 million barrels per day in Q2 2026 as Middle Eastern production falls — proving once again that removing millions of barrels from global supply during a geopolitical crisis is apparently “bullish” for inflation after all.

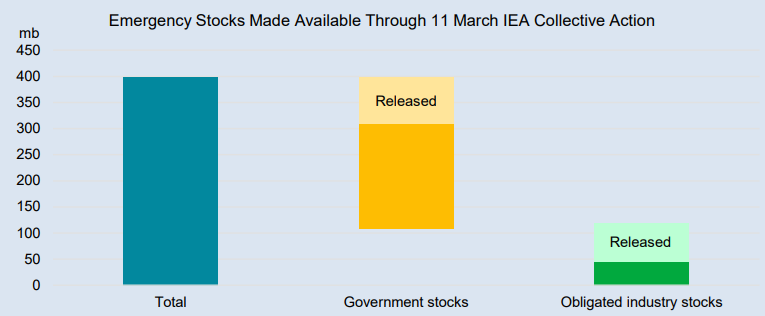

The release of 400 million barrels from IEA reserves may buy markets a little time, but with supply deficits still looming, it increasingly looks less like a solution and more like using a garden hose to stop an oil-field fire.

As the Empire continues exporting “democracy” through regime-change adventures, more countries are inevitably concluding what Pyongyang understood years ago: in the modern Orwellian rules-based order, the ultimate despot survival package is not human rights — it is nuclear deterrence. On cue, North Korea quietly updated its constitution to authorize an automatic nuclear strike if Comrade Kim is assassinated or if the country’s nuclear command system is threatened. The message was refreshingly straightforward by diplomatic standards: if leadership disappears, so does everyone else. Iran, apparently, provided the latest reminder that in the global security marketplace, nuclear weapons remain the closest thing to a lifetime insurance policy.

When trust in the empire fades, kingdoms seek the shield of the dragon. From Iran and Saudi Arabia to Japan, South Korea, and parts of Europe, nations are increasingly reconsidering nuclear deterrence as faith in U.S. security guarantees and the old non-proliferation order steadily erodes. The lesson many capitals drew from Iraq War, Libya, and recent geopolitical conflicts is brutally simple: in the modern world, sovereignty without deterrence may be little more than a temporary illusion. As all nuclear powers continue expanding and modernizing their arsenals, the world is quietly drifting from globalization toward a new era of atomic multipolarity.

On the Eastern front of Eurostan, European governments now call it “humanitarian coordination” while quietly helping manage the demographic depletion of a country being consumed by war. Ukraine’s leadership increasingly treats population itself as a strategic resource: men restricted from leaving, refugees pressured to return, citizenship locked down, and conscription expanded as casualties mount and demographics collapse.

Meanwhile, Western leaders continue packaging all of this as a heroic defence of “democracy” and “European values,” because apparently freedom now means the state deciding where you live, when you leave, and potentially where you die. The war is no longer just destroying infrastructure — it is hollowing out Ukraine’s future population itself, while Europe applauds the process with carefully sanitized Orwellian vocabulary like “solidarity,” “repatriation,” and “humanitarian assistance.”

In Asia, Taiwan’s deployment of U.S.-supplied HIMARS systems just off China’s coastline is being sold as “peace preservation,” because in modern geopolitics, placing long-range missile systems within minutes of major population centres is apparently the new language of stability. Washington calls it deterrence. Beijing calls it encirclement. Both sides continue militarizing the Pacific while insisting they are acting defensively, proving once again that war is peace, escalation is stability, and missile deployments are now classified as humanitarian reassurance.

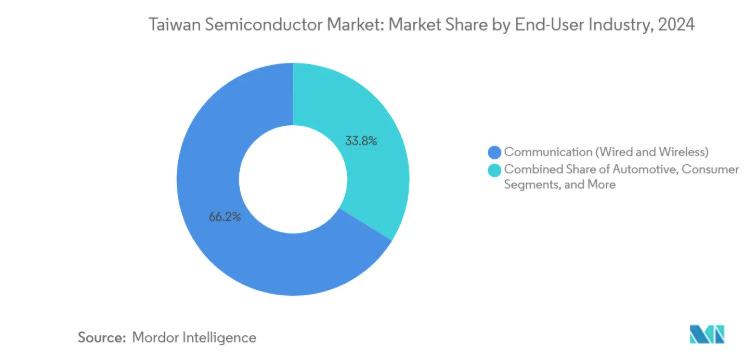

Meanwhile, the economic consequences remain carefully excluded from the official optimism package. Taiwan sits at the center of global semiconductor production and critical shipping routes, meaning any conflict in the Strait would detonate supply chains already weakened by debt, inflation, and energy instability. But the militarization continues under the reassuring banner of “stability.” The more weapons systems arrive, the more both sides lock themselves into escalation while publicly insisting they are preserving peace. History rarely begins with leaders announcing they want catastrophe. More often, it arrives through gradual escalation, strategic posturing, and mutual miscalculation — right up until nobody can politically afford to step backward anymore.

https://www.mordorintelligence.com/industry-reports/taiwan-semiconductor-market

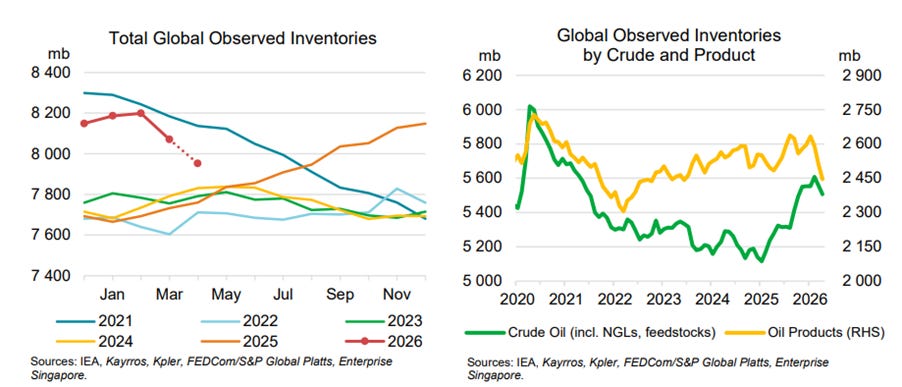

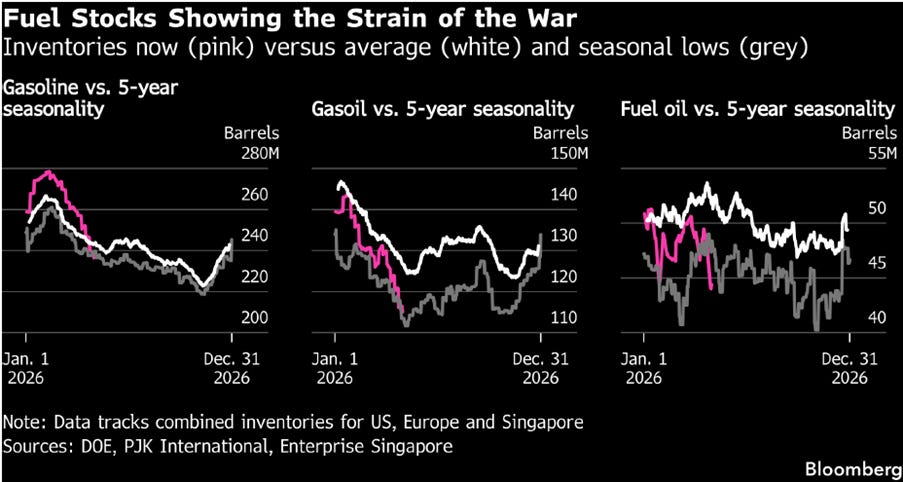

While markets continued debating whether the “Epic F**k Up” was finally ending, the reality inside global storage facilities looked far less comforting: crude inventories kept collapsing toward levels where the issue was no longer price, but whether the system could physically function at all.

According to JPMorgan Chase projections, inventories were expected to fall toward 7.6 billion barrels by June 2026 — the so-called operational stress level — before approaching 6.8 billion barrels by September, effectively the minimum needed to keep pipelines pressurized and refineries operating. Below that threshold, the conversation shifts rapidly from “$90 or $110 oil” to the far more awkward question policymakers prefer to avoid: what happens when fuel infrastructure itself starts breaking down?

Global inventories for major fuels are in the same mood, now sitting at, or below, the lowest seasonal levels of the past five years — just in time for the Northern Hemisphere’s peak summer demand season, because apparently the global energy system enjoys living dangerously. Gasoline inventories looked “reassuring” a few months ago, peaking at their highest levels since 2019 in February, only to perform a spectacular disappearing act by May and fall below the lowest levels seen for this time of year in more than a decade. But markets remain calm, reassured that shortages are surely just another “transitory” phenomenon.

In short, the global economy now has roughly four months to magically rediscover diplomacy before every major market on Earth reprices simultaneously. Energy, food, shipping, manufacturing — all remain tied to the same rapidly shrinking inventory curve that policymakers are still pretending is perfectly “manageable.”

But for now, markets remain comforted by reassuring press conferences explaining that shortages, inflation, and geopolitical escalation are all somehow a non-event.

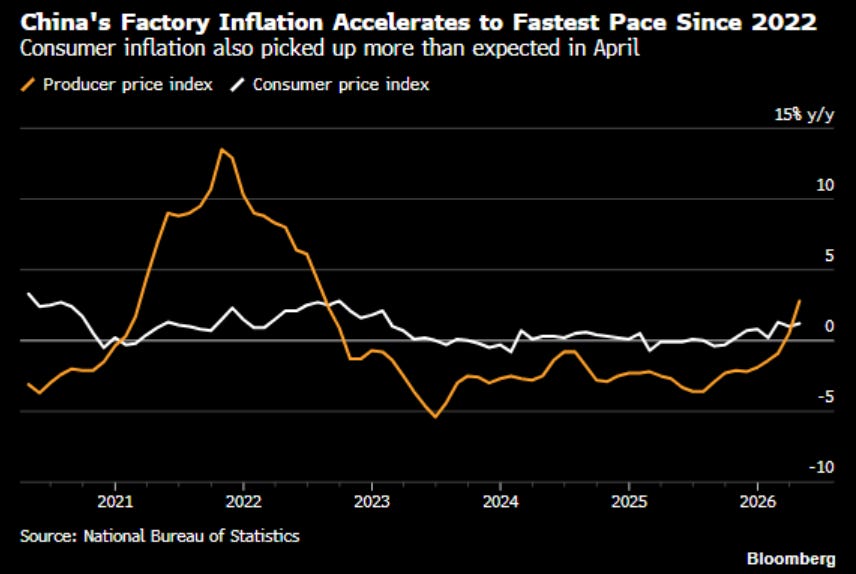

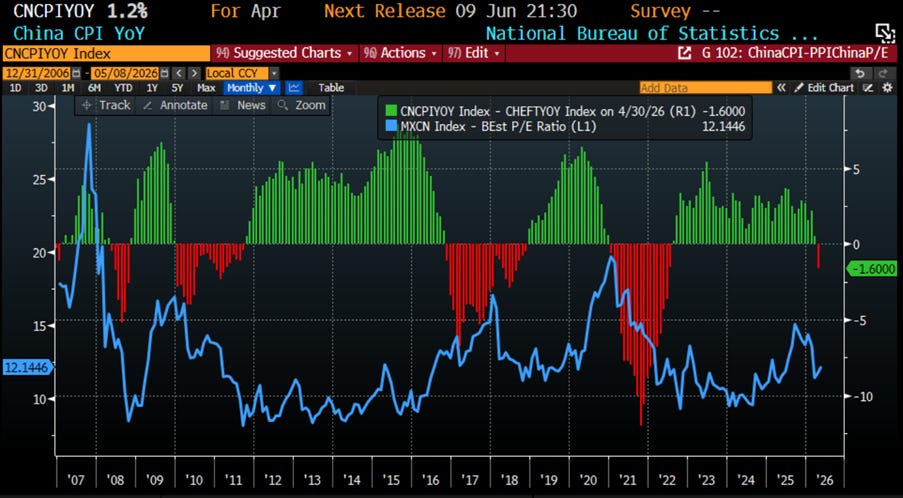

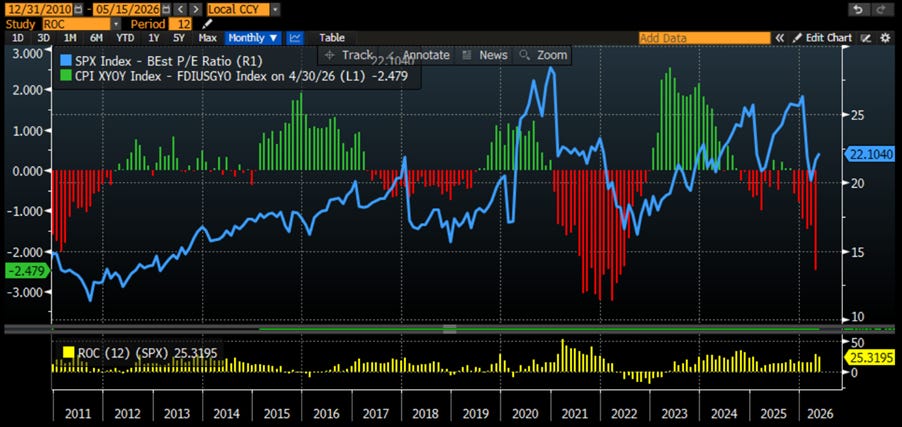

As Confucius almost certainly never said, “When oil burns in the Middle East, factory prices rise in the Middle Kingdom.” China’s producer inflation surged at its fastest pace since the pandemic as the Iran war sent energy and commodity costs soaring, officially ending years of factory deflation and reminding investors that globalization works beautifully right until shipping lanes catch fire. Yet while AI-driven demand for semiconductors and integrated circuits exploded, helping high-tech exports surge, many Chinese manufacturers now find themselves trapped between rising input costs and consumers still reluctant to spend, a situation ancient scholars would describe as “the margin is squeezed from both Heaven and Earth.” Copper, oil, chemicals, and AI chips all became more expensive simultaneously, proving once again that in the modern economy even artificial intelligence ultimately depends on mines, pipelines, and geopolitical chaos.

As everyone knows, “The wise investor watches not the headlines, but the spread between costs and prices.” And unfortunately for China equity bulls, the spread between core CPI and core PPI just reached its worst level since February 2021 — precisely when the Middle Kingdom entered its second wave of the Covid “great harmony campaign,” triggering a derating of Chinese equities that lasted until October 2022. Once again, margins appear to be discovering the ancient Chinese art of suffering in silence.

Spread between China Core CPI and China Core PPI (histogram); 12-monht Forward P/E MSCI China (blue line).

April’s CPI will undoubtedly be marketed as a minor inconvenience caused by the Empire’s “tiny and totally successful” Middle East excursion — you know, the one declared won sometime around Hour 1 of Day 1, yet somehow still managing to rattle global oil supply routes 73 days later and counting. Victory has apparently become a subscription service.

For ordinary Americans not employed by the Malthusian Washington Swamp plutocracy, however, grocery prices will continue their inspiring journey upward, while energy costs remind everyone that “disinflation” was less an economic trend and more a seasonal marketing campaign. Inflation didn’t disappear. It just stopped to tie its shoes before sprinting into Wave Two less than five years after the first one.

Meanwhile, policymakers and market cheerleaders keep celebrating “transitory” inflation while preparing the next fiscal spending bonanza and geopolitical adventure package. Because naturally, the solution to too much money chasing too few goods is apparently… even more money chasing even fewer goods. And here’s the inconvenient part: inflation and collapsing institutional trust tend to move together like synchronized swimmers in a controlled demolition. The more households feel squeezed, the louder the official narrative insists everything is “resilient,” “stable,” and “well anchored.”

But don’t worry. Nothing to see here. Just keep trusting the government statistics while your grocery receipt quietly auditions for a Netflix true-crime documentary.

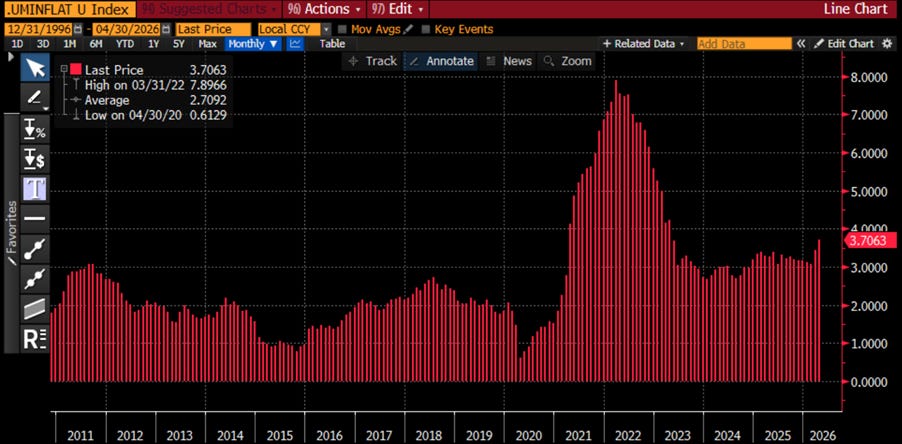

US Umbrella inflation Index (Average of CPI; Core CPI; PPI; Core PPI; Core PCE, 1-year consumer inflation expectations)

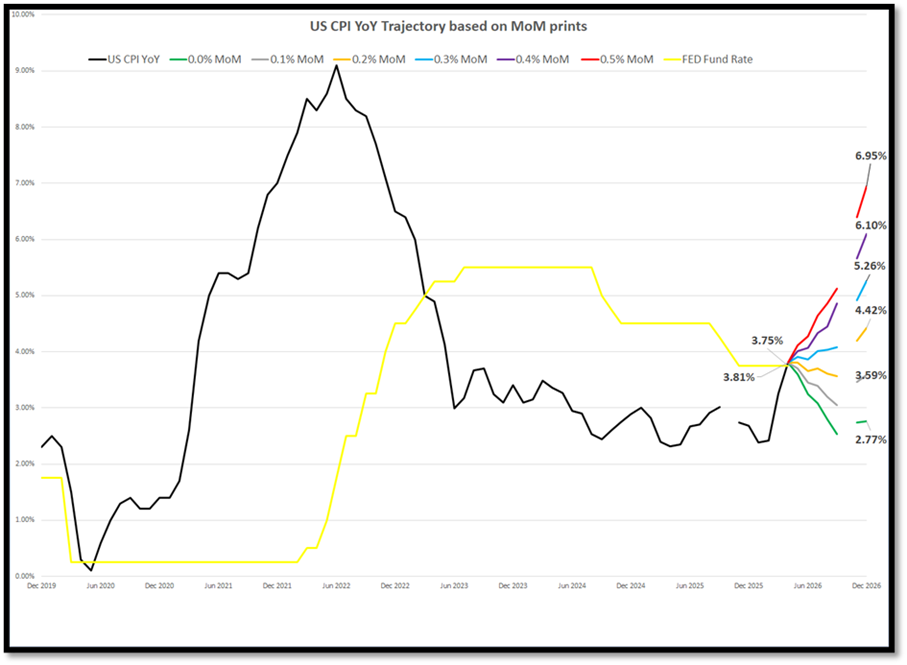

Instead of fantasizing about 2% inflation like it’s another campaign slogan, seasoned investors — unlike certain Wall Street strategists still overdosing on spreadsheet ‘hopium’ — can still perform elementary-school math.

For that miraculous 2% CPI target to materialize by the end of 2026, monthly inflation prints would basically need to hover around or below 0.0% from here onward. Best of luck pulling that off while a freshly politicized Fed chair gets ceremonially crowned and geopolitical conflicts spread faster than a viral TikTok conspiracy thread.

Meanwhile, if monthly CPI keeps printing at a far more realistic 0.3%+, we’re not heading toward “price stability” — we’re cruising straight into roughly 5.3%–7.0% CPI territory by year-end, complete with complimentary media excuses and emergency talking points.

And when reality finally crashes through the narrative, not even Donald Copperfield performing his latest “Central Banker-in-Chief” illusion from beneath a MAGA hat will conceal the fact that cutting rates into an inflationary boom ranked among the Fed’s more spectacular policy magic tricks.

Bonus round: all those delightful shortages, shipping disruptions, and energy shocks are lining up perfectly to collide with midterm election season — right when voters begin asking why their grocery bills now require small-business financing.

Abracadabra: your purchasing power vanished somewhere near the Strait of Hormuz, but thankfully the official CPI basket assures you inflation expectations remain “well anchored.”

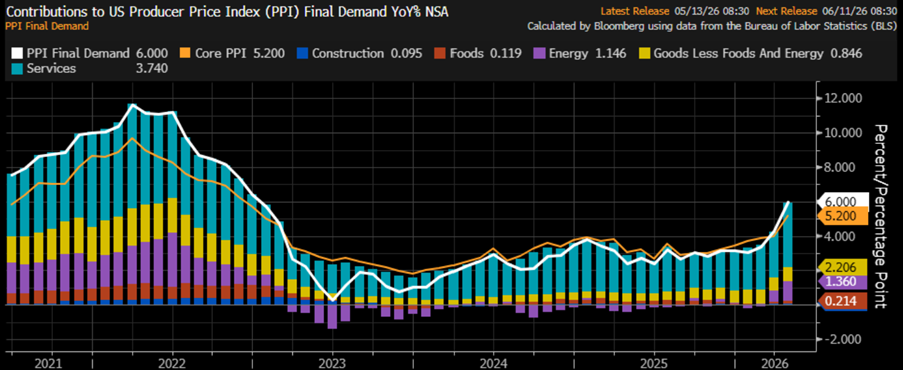

After another hotter-than-expected “CPLie,” U.S. wholesale inflation surged to its fastest pace since 2022, as war-driven energy prices reminded economists that “disinflation” was apparently just a temporary hallucination. Producer prices jumped 6% YoY, core PPI hit its hottest level in over three years, and transportation costs soared as trucking and fuel expenses exploded higher. In other words: energy, freight, and supply chains are all getting more expensive again — but don’t worry, central bankers still assure us inflation expectations remain “well anchored.”

For equities, the real signal isn’t the comforting media narrative but the spread between core CPI and core PPI — a simple measure of whether companies can protect margins while costs explode underneath them. In April, that spread stayed negative for a sixth straight month and hit its weakest level since May 2022, signalling that input costs are once again rising faster than companies can pass them on. The last time this happened consistently, in 2021–2022, equity multiples compressed hard — despite Washington insisting the economy was “strong” right up until reality showed up with the invoice.

Spread Between US Core CPI & PPI (histogram); 12-month Fwd P/E of S&P 500 index (blue line); S&P 500 index 12-month return (below panel; yellow histogram).

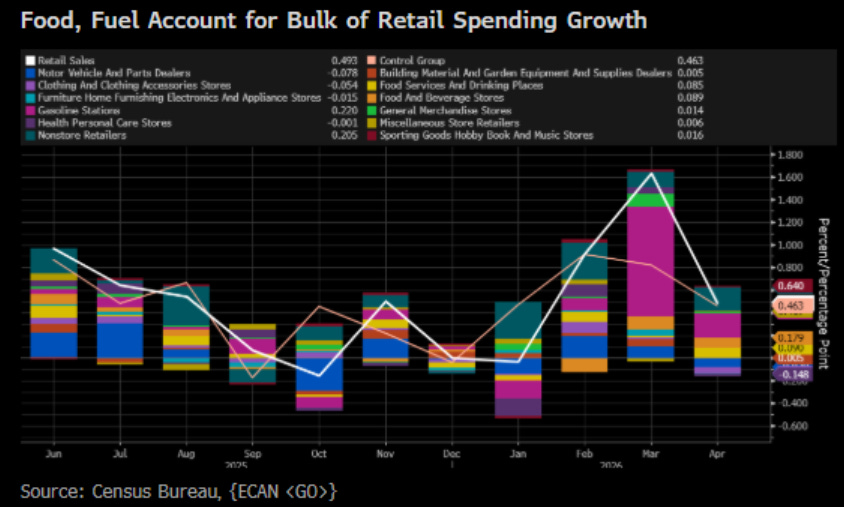

US retail sales rose for a third straight month in April, once again proving that American consumers will keep spending until either confidence, savings, or credit cards physically collapse — whichever comes first. Headline retail sales climbed 0.5%, although nearly half the increase came from higher gasoline prices, meaning Americans mostly spent more just to drive to the store and pay more for groceries. Excluding gas stations, sales rose a far less exciting 0.3%, while vehicle sales slipped as consumers apparently discovered that $80,000 pickup trucks and 7% financing rates are not the bargain of the century.

Adjusted for “CPLie,” headline retail sales actually declined 0.35% MoM — another sign that Americans are increasingly spending more merely to maintain the same routines while ultimately buying less in real terms. Consumers continue driving to keep their jobs and paying more for essentials, but real purchasing power keeps deteriorating beneath the surface. Historically, this type of divergence between nominal spending and real consumption has often marked the early stages of broader stagflationary pressure — a parallel markets may ignore temporarily, but one long-term investors will recognize immediately.

US Retail Sales Adjusted to inflation (i.e. CPI) (blue line); S&P 500 to WTI ratio (yellow line); 7-Year Moving Average of the S&P 500 to WTI ratio (red line).

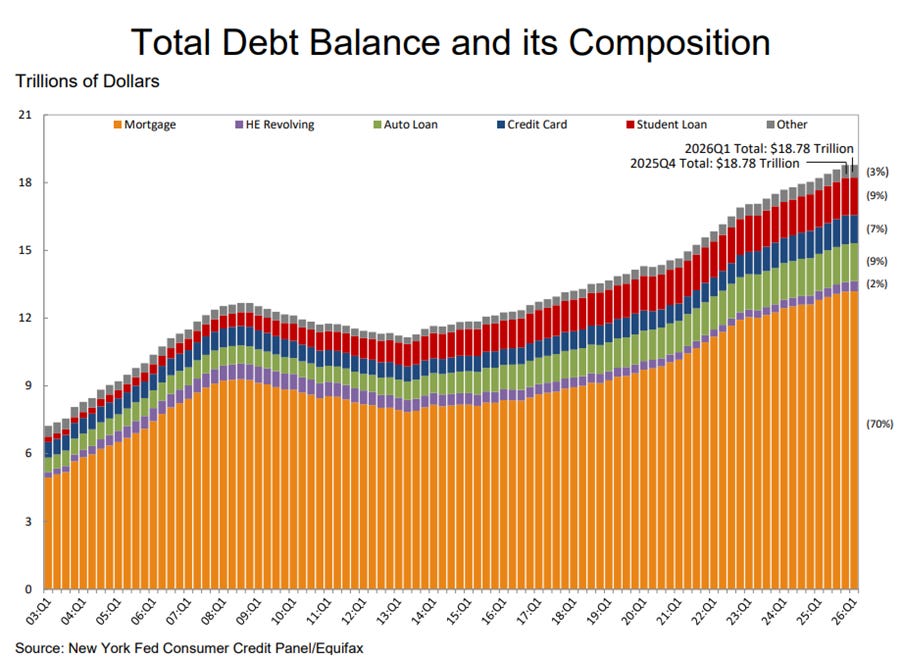

In yet another “totally transitory” side effect of Washington’s forever-war economics, U.S. household debt climbed to a fresh record $18.8 trillion in Q1 2026 — up $4.6 trillion since pre-pandemic days — while mortgage balances, HELOCs, and auto loans kept rising like nothing could possibly go wrong.

Credit card balances dipped slightly thanks to seasonal paydowns, which policymakers will probably interpret as proof the consumer is “resilient,” even as mortgage delinquencies quietly worsen, student loan delinquencies jump above 10%, and foreclosures begin creeping higher again. But don’t worry according to the official narrative, Americans drowning in debt while borrowing against their homes to survive inflation is apparently just another sign of a “strong economy.”

https://www.newyorkfed.org/medialibrary/interactives/householdcredit/data/pdf/HHDC_2026Q1

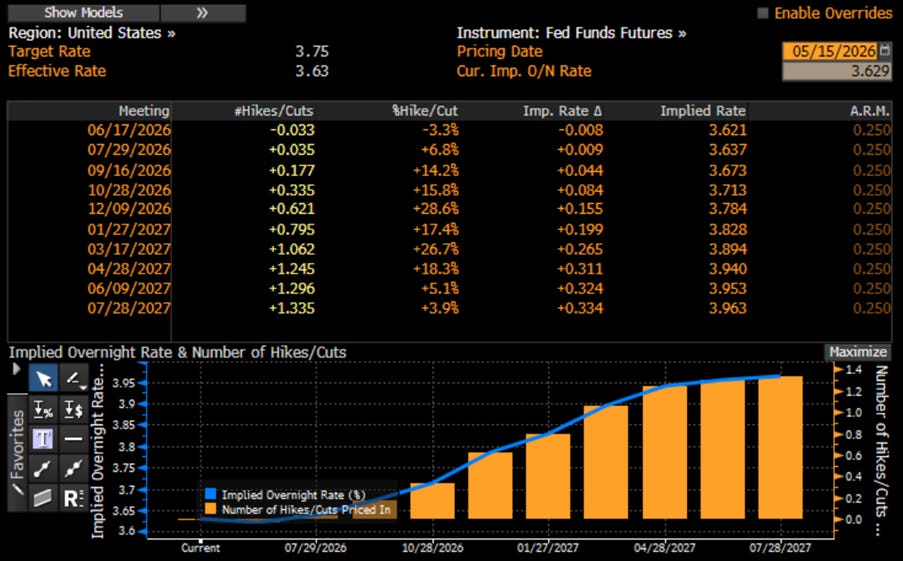

As the new Fed Chair was officially crowned Central Banker In Chief, Wall Street’s endlessly imaginative EYIs finally woke up from their enchanted “rate cuts and a soft landing” fairy tale and are now pricing a 25bps hike by December with a delightful 62% probability. Meanwhile, Trump Stagflation has rapidly evolved from “baseless conspiracy theory” into what increasingly looks like the Empire’s official economic doctrine, while the Manipulator-in-Chief reassured the population that the Persian “little excursion” is merely a tiny inconvenience required to continue exporting democracy, inflation, and regime change all at once. At this stage, like all the public institutions of the Empire, the Fed resembles less a central bank and more a nervous airline passenger politely handing the cockpit to the bond market, while its credibility continues a graceful descent somewhere above the Strait of Hormuz — still technically a soft landing, just missing a runway, engines, and possibly the plane itself.

The Bronze Age was forged with copper and tin, the Industrial Revolution marched on coal and steel, and the 20th century worshipped at the altar of oil. Now comes the Age of Silicon, where tiny chips hidden inside smartphones, fighter jets, AI servers, and electric cars quietly rule the world with the humility of a Confucian bureaucrat and the power of an emperor. Modern civilization no longer runs only on bread and water, but also on GPUs, memory chips, and semiconductor fabs scattered across a few sacred territories. In this new digital Mandate of Heaven, every nation seeks sovereignty over the semiconductor supply chain: America wants technological supremacy, China seeks self-sufficiency, Europe dreams of industrial independence, while AI consumes chips with the appetite of an imperial court during famine season. The result is no longer a simple trade war, but a geopolitical chess match where whoever controls advanced semiconductors may ultimately write the rules of the 21st century.

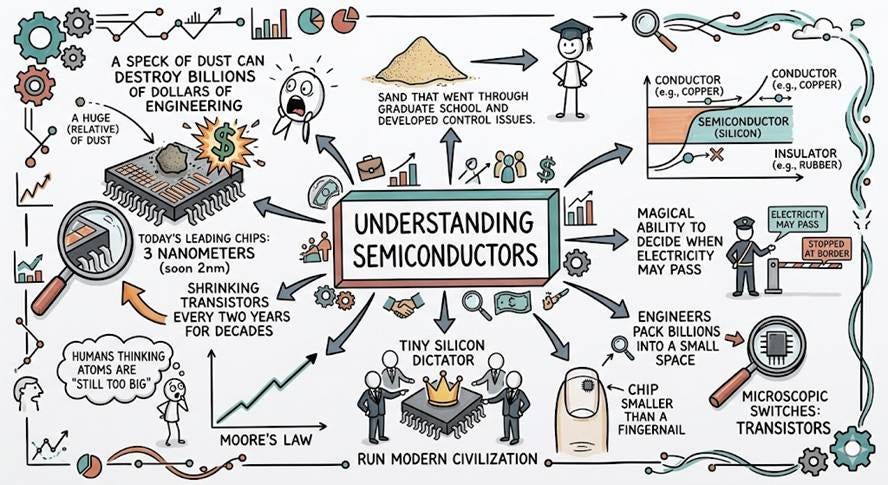

A semiconductor is essentially sand that went through graduate school and developed control issues. Sitting awkwardly between a conductor like copper and an insulator like rubber, silicon has the magical ability to decide when electricity may pass and when it should be stopped at the border. Engineers then pack billions of microscopic switches called transistors onto a chip smaller than a fingernail, creating the tiny silicon dictators that now run modern civilization. Thanks to Moore’s Law, the industry spent decades shrinking transistors every two years, because apparently humans looked at atoms and thought: “still too big.” Today’s leading chips operate at 3 nanometers and soon 2nm, a scale so absurdly small that a speck of dust can destroy billions of dollars of engineering.

A chip is essentially a tiny electronic brain etched onto a slice of silicon, designed to process, store, and move information faster than most government bureaucracies move paperwork. Some chips specialize in logic, like CPUs and GPUs, while memory chips quietly remember everything humanity posts online at 2 a.m. South Korea dominates much of this memory empire, proving once again that civilization now runs on sleep deprivation and server farms. Other chips manage sound, electricity, industrial machinery, and electric vehicles, while AI chips have become the new imperial class of semiconductors, consuming oceans of electricity and entire mountains of GPUs to train machines to generate emails nobody asked for. In the end, modern AI is really just billions of transistors switching on and off at terrifying speed while investors call it “the future.”

https://www.samaterials.com/blog/types-and-classifications-of-semiconductor-materials.html

Modern semiconductors may look like futuristic technology, but the industry is really an elaborate global scavenger hunt involving sand, rare metals, chemicals, water, and geopolitics. Silicon comes from humble quartz sand, although it must be purified to levels so extreme that a single dust particle can financially traumatize an engineer. China dominates rare earths and gallium production, giving Beijing a strategic grip over everything from 5G networks to defence systems, while copper has become the nervous system of AI data centres consuming metal with the appetite of a Roman empire at peak decadence. Meanwhile, neon gas from Ukraine, palladium from Russia, platinum from South Africa, and specialty chemicals from Japan remind investors that even artificial intelligence ultimately depends on mines, pipelines, shipping routes, and weather forecasts. In the end, the semiconductor supply chain is less a triumph of globalization than a highly sophisticated international hostage situation held together by ultra-pure water and diplomatic anxiety.

Semiconductor manufacturing is what happens when humanity decides that building rockets is simply not stressful enough. A modern chip fab can cost more than $20 billion and requires thousands of production steps performed with atomic-level precision inside ultra-clean rooms where a single dust particle can destroy millions of dollars of silicon and several executive careers. At the centre of this industrial madness sits Dutch company ASML, whose EUV lithography machines are so complex and expensive — roughly $200 million each — that they make nuclear reactors look like IKEA furniture. Engineers then obsess over “yield rates,” the percentage of chips that survive the manufacturing process, before packaging them into AI processors designed to consume enough electricity to make entire power grids nervous. In short, modern semiconductors are tiny pieces of sand that require the economic coordination of an empire and the cleanliness standards of a surgical monastery.

The semiconductor supply chain is globalization in its purest and most fragile form: America designs the chips, Taiwan manufactures them, South Korea remembers everything with memory chips, Japan quietly supplies the chemicals nobody can live without, Europe builds the absurdly expensive machines, and China buys almost everything while trying to become self-sufficient. The United States dominates chip design through companies like NVIDIA, AMD, and Intel, while Taiwan’s TSMC has become the industrial equivalent of a sacred temple where the world’s most advanced chips are printed. South Korea’s Samsung Electronics and SK Hynix dominate memory production, Japan supplies critical materials with the quiet efficiency of a master craftsman, and Europe contributes precision engineering through ASML. Meanwhile, China spends hundreds of billions trying to reduce dependence on foreign technology, proving that in the AI era, semiconductors are no longer just electronics — they are economic survival packaged inside microscopic rectangles of silicon.

https://www.rabobank.com/knowledge/s011371708-understanding-the-semiconductor-supply-chain

The semiconductor industry is rapidly becoming the financial equivalent of an imperial gold rush. Global chip sales are expected to reach nearly US$1 trillion in 2026 as the AI boom triggers a historic spending frenzy on data centers, GPUs, and advanced infrastructure. Yet beneath the headlines lies a spectacular imbalance: AI chips now generate roughly half of industry revenues while representing less than 0.2% of total chip volumes, proving once again that in modern capitalism, a few silicon aristocrats eat while the commodity chips survive on ration coupons. Meanwhile, traditional segments like smartphones, PCs, and automotive chips are growing far more slowly as Wall Street focuses almost exclusively on anything remotely connected to artificial intelligence. In other words, the semiconductor sector increasingly resembles a digital monarchy where a few GPU emperors rule over an economy powered by electricity, optimism, and extremely expensive server racks.

Keep reading with a 7-day free trial

Subscribe to The Macro Butler’s Substack to keep reading this post and get 7 days of free access to the full post archives.