When 'Trump Trades' meet 'Trump Tariffs' …

THE WEEK THAT IT WAS...

Over the week of the spring equinox in the Northern Hemisphere, investors once again focused on retail sales in China and the U.S., while the main event was undoubtedly the second FOMC meeting of the Jubilee Year, alongside the Bank of Japan and Bank of England meetings.

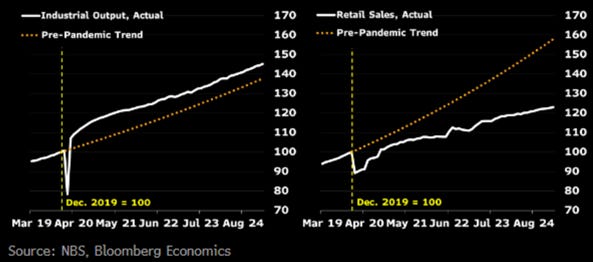

China’s economy performed better than expected in the first two months of 2025, with industrial output expanding 5.9% year-on-year and fixed asset investment growing 4.1%. However, consumption remains weak despite efforts like the cash-for-clunkers program and the success of Ne Zha 2 at the box office. Retail sales rose 4.0%, but monthly figures show a slowdown in growth, with industrial production and retail sales both decelerating compared to previous months. To Make China Great Again, the government must follow through on measures aimed at boosting domestic consumption in an increasingly polarized world.

As widely expected, the Bank of Japan left its key interest rate unchanged at 0.5%, citing "the evolving situation regarding trade and other policies in each jurisdiction" as a potential reason for delaying an inevitable rate hike later this year. Given stronger domestic inflation and rising wages, Japan is inevitable moving into stagflation and an inescapable financial doom loop.

Gold Price to Japanese Bond Ratio (blue line); 84-Month Moving Average of Gold Price to Japanese Bond Ratio (red line); Bank of Japan Overnight Call Rate (green line).

US Headline retail sales rose 0.2% (vs. -1.2% prior, revised lower), well below the 0.6% consensus. Gains in non-store retail and health/personal care offset declines in goods and services. Excluding autos and gas, sales rose 0.5% (vs. -0.8% prior). The control group, which strips out cars, gas, food services, and building materials, jumped 1.0% (vs. -1.0% prior), surpassing both our 0.2% forecast and the 0.4% consensus. Notably, food service and drinking place sales, a key proxy for services spending, dropped 1.5% (vs. a revised 0% prior).

Inflation-adjusted retail sales hit their lowest since August 2024. Investors tracking the business cycle know this rarely bodes well for the S&P 500 to Oil ratio. When it falls below its 7-year average, an economic bust follows likely sooner rather than later, as the White House's 'Tariff Executive Orders' spread hardship globally, turning "Making America Great Again" into a distant illusion. Bottom line: February retail sales saw a modest rebound, led by stronger online and healthcare spending. However, slowing income growth and rising job insecurity likely weighed on discretionary services demand.

US Retail Sales Adjusted to inflation (i.e. CPI) (blue line); S&P 500 to WTI ratio (green line); 84-months Moving Average of the S&P 500 to WTI ratio (red line).

As expected, the FOMC kept the federal funds rate at 4.25%–4.5% but removed its balanced risk assessment, instead warning that “UNCERTAINTY AROUND THE ECONOMIC OUTLOOK HAS INCREASED.” The FED cut its 2025 GDP forecast from 2.1% to 1.7%, raised core PCE inflation from 2.5% to 2.8%, and increased its unemployment projection to 4.4%. The dot plot still signals two rate cuts in 2025, with the year-end median projection at 3.88%, little changed from December's 3.73%.

In this context, Wall Street bankers and their parrots continue to delude themselves into believing that the increasingly impotent FED will keep cutting rates, even as the president enacts tariffs and tighter immigration policies that will fuel stagflation, regardless of the White House's official propaganda. Likely driven by the belief that FED rate cuts will once again rescue Wall Street and Main Street as the U.S. economy shifts into an inflationary bust, the market now prices in a 81% chance of three rate cuts this year, with the first fully expected in June, compared to October just a month ago. The reality is that no rate cut may even materialize over the next nine months, while the FED could be forced to hike rates again to combat the coming inflationary bust if it wants to keep a modicum of credibility among the American people and investors.

Looking at the English dictionary, ‘Trumped’ means to be surpassed or outdone by something stronger or more significant. The term comes from card games like bridge, where a winning card ‘trumps’ others. In broader use, it describes one argument, event, or action overriding another. A ‘trumped trade’ refers to a transaction that is decisively outperformed by a better alternative. In finance, this could mean an investment strategy that is overshadowed by a more profitable opportunity, such as a stock position losing appeal due to a sudden market shift. This definition is based on linguistic roots rather than an established financial term.

It has been 60 days and counting since the ‘Disruptor In Chief’ has been sworn in as the 47th U.S. president, and unless investors have been living in a deep hole in the middle of the Gobi Desert, the word that has predominated in financial media is the supposedly most beautiful word in the English dictionary, i.e. tariffs.

Mentions of Tariffs.

Outside of tariffs, the other hot topic among American CEOs in recent months has been the implementation of government spending by the now-famous Department of Government Efficiency (DOGE), led by the world's richest man and Tesla CEO, Elon Musk.

Tariffs are government-imposed taxes on imports or exports, mainly used to raise revenue, protect domestic industries, or influence trade balances. For example, a 10% tariff on imported steel raises costs, encouraging local alternatives. While tariffs can shield domestic producers, they also spark trade disputes and impact consumer prices. Historically, tariffs have shaped economies for centuries. Ancient empires used them as tolls, medieval states for revenue and protectionism, and mercantilist powers to control trade. The 19th century saw fierce debates between free trade and protectionism, with the U.S. imposing high tariffs like the 1828 "Tariff of Abominations." In the 20th century, the Smoot-Hawley Act worsened the Great Depression, leading to post-WWII tariff reductions under GATT.

The first impact of tariffs is increased trade policy uncertainty, as they can change at any time at the discretion of the ‘Disruptor-in-chief’ in the Oval Office. Since the November 5th election results, this uncertainty alone is expected to reduce world trade by 1.5% and global industrial production by 1.0% by year-end, compared to a scenario with stable trade policy.

US Economic Policy Uncertainty Index.

As tariffs are on, tariffs are off, tariffs are delayed, US consumer confidence has taken a sharp hit, as reflected by the University of Michigan sentiment survey, which dropped to its lowest level since the inflation peaks of 2022. This decline in confidence has led to a noticeable shift in spending patterns. The combination of unclear policy direction and rising living costs is creating a toxic mix for the average American. The US economy is inevitably heading into a period of stagflation, where the prices of goods and services rise while real buying power diminishes, leaving consumers spending more for less. Many are mistakenly equating rising prices with inflation, failing to recognize that stagflation, not deflation, is the real issue, as disposable income stagnates. The lack of confidence in both the economy and government policy has become a self-fulfilling prophecy, with businesses and consumers hesitant to invest, reinforcing a cycle of slow growth and rising costs. Ultimately, it all boils down to a crisis of CONFIDENCE.

University of Michigan Consumer Sentiment.

Tariffs are just one of many policy tools designed to raise trade barriers and realign supply chains in the name of national and economic security. While implementation has accelerated under the 47th U.S. president, the overall direction has remained consistent across three administrations.

In a nutshell, no one wins in a trade war. According to OECD estimates, rising trade barriers, political uncertainty, and a 10% tariff hike on U.S. imports, met with retaliation, could shrink global GDP by 0.3%, hitting North America hardest: U.S. (-0.7%), Canada (-0.6%), and Mexico (-1.3%). Inflation would rise by 0.4 percentage points globally and 0.7 in the U.S. over three years. The OECD warns that escalating trade wars will hurt all economies, with the U.S. among the biggest losers.

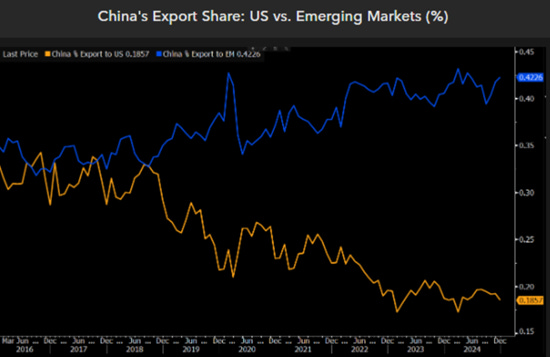

Tariffs may cut China’s U.S. export share, but they accelerate its shift to emerging markets. From 2017 to 2024, China’s exports to EMs nearly doubled to $1.49 trillion, raising their share from 32.5% to 42.3%, while the U.S. share fell from 28.8% to 18.6%. Key growth markets include Mexico ($90B, doubled) and ASEAN ($587B, now China’s top export destination). While new U.S. tariffs will push China’s effective rate to 30%, exports to the U.S. account for just 2.5% of China’s GDP. Even a 30% drop in U.S.-bound exports wouldn’t be a major shock to growth.

By contrast, a full-scale trade war within the tightly integrated North American economies, once unimaginable but now highly likely, would significantly impact all three countries' economic activity. Sustained U.S. tariffs on Canada and Mexico would almost certainly trigger retaliatory duties. U.S. trade with Mexico and Canada accounts for 5.4% of its GDP, a much larger share than China’s trade with the U.S., which represents only 3.7% of its economy.

As the mercantilist Global South moves to de-dollarize trade, fewer USD will be generated globally, while USD-denominated debt remains unchanged. Combined with factors like geopolitics and looming debt crises in Europe and Japan, tariffs will further strengthen the USD against other fiat currencies.

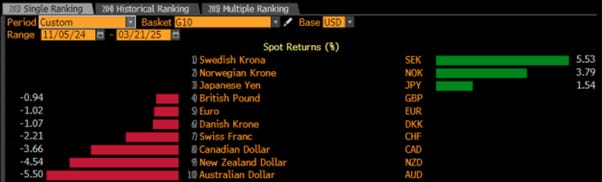

Performance of G10 Currencies against USD since November 5th, 2024.

The binary nature of the tariff narrative, highlighted by Mexico-Canada tensions in early February, makes strong FX directional views difficult. Tariff uncertainty is driving higher FX volatility, with the JPM G-10 one-month volatility index rising to above 8.0 from a 2024 average of 7.71.

Tariffs are adding to the growing list of catalysts for further de-dollarization and FX regionalization. Not only are tariffs stagflationary, but they also contribute to an even more uncertain economic and geopolitical environment, as they are part of the tools used to weaponize USD assets. Ultimately, tariffs will drive the increase in gold reserves held by central banks, which has been the major catalyst for the gold bull trend. Indeed, spot gold has risen 76% since its late-2022 low just above $1,600 per ounce, coinciding with gold's share of central bank FX reserves rising from 13.5% to nearly 21%.

Gold Price in USD (blue line); % of Global FX Central Bank Reserve in Gold (red line).

One aspect of Trump’s tariffs that he and his advisers fail to understand is clearly related to his concepts of how the world economy functions, which were seriously forged in the Middle Ages. Trump's tariffs reflect a view of the economy, rooted in outdated concepts of backing, fiat, and gold. The dollar's reserve status has nothing to do with gold or the old ideas of currency value; all currency is fiat, decreed by governments. Historically, even gold and silver coins were fiat, with governments controlling their weight and value. The true backing of a currency lies in the productivity and freedom of its people, as seen in the rise of Japan and Germany post-WWII, and in America's innovation during the Cold War, exemplified by Nixon's Kitchen Debate with Khrushchev. The dollar became the reserve currency not because of gold, but because of American ingenuity and productivity. This truth traces back to ancient Rome, where currency's value was shaped by the people's capacity to produce, not by the metal content, as noted by Sir Thomas Gresham. The $5 U.S. gold coin, weighing 8.359 grams at 90% purity, was overvalued in the Latin Monetary Union, prompting the creation of a $4 Stella coin pattern, though it was never issued, and the LMU ultimately collapsed.

Trump’s anti-BRICS stance overlooks the real reason BRICS emerged: the Neocons’ desire to undermine Russia's economy for geopolitical gains. Removing Russia from SWIFT raised global alarms, prompting China to create its CIPS system as an alternative. BRICS now represents over 50% of the world’s population, with neutral politics as its core appeal, in contrast to the U.S.’s military-focused approach. The dollar’s reserve status is tied to America's dominance in global trade, much like ancient Rome’s economic power. Trump’s tariffs, aiming to bring manufacturing back to the U.S., would harm global trade and undermine the dollar’s role. Historically, American companies have been more competitive and innovative, which helped maintain the dollar's status, but tax policies forcing businesses to go global in the progressive era pushed many out of the U.S., ultimately weakening its global trade advantage. The threat of US financial sanctions was little discussed by financial media, but one of Donald Trump’s first acts as the 47th US president was to threaten the Colombian government with financial sanctions, not just tariffs, should President Gustavo Petro refuse to allow deportation flights from the US carrying Colombian illegal immigrants to land in the country. Such threats have raised and will continue to raise the risk premium of US assets for foreigners from countries not keen to accept ‘Trumperialism,’ increasing the risk of further weaponization of USD assets in general.

Trump's economic strategies, including his support for cryptocurrencies and imposing drastic tariffs, are grounded in outdated theories that no longer apply. His advisers believe these actions will revive the U.S. economy, but they are misguided. Instead, these policies will likely shrink the U.S. economy and trigger a global recession. The U.S. is headed for an economic downturn and sharp rise in the unemployment rate through 2026 and beyond, as forecasted by the ratios which are driving the businss cycle such as the S&P to Oil ratio and the Gold to Bond ratio. The recent performance of gold, surpassing the S&P 500, and the break of the S&P 500 to gold ratio below its 7-year moving average on January 20th, 2025, the day the 47th president took office, indicates the beginning of a larger economic shift.

S&P to Gold Ratio (blue line); 84-month Moving average of the S&P 500 to Gold Ratio (red line); US Unemployment Rate (axis inverted; green line).

Treasury Secretary Scott Bessent's recent downplaying of tariffs’ inflationary impact is a significant mistake. He claimed tariffs would be a "one-time price adjustment," but this is far from the reality. Tariffs will have widespread, long-term effects that ripple through the global economy. His comments, likening tariffs to the past "transitory" inflation narrative, overlook the substantial economic consequences. Bessent's optimism about inflation being unaffected by tariffs reflects a misunderstanding of the broader economic impacts.

https://www.foxbusiness.com/video/6369692167112

Anyone with a modicum of economics knowledge knows tariffs have to be paid by someone, consumers, producers, or intermediaries. If companies bear the cost, operating margins will suffer, potentially weakening equity prices, as seen in 2018 when Trump's tariffs triggered margin declines and a double-digit drop in global stocks. This time, broader and more extreme tariffs could hit fundamentals even harder. From the first 2018 tariffs on washing machines and solar panels to the removal of some on Canadian and Mexican metals, 12-month forward operating margin estimates fell 70 bps for the S&P 500 index ex energy.

S&P 500 ex Energy Index Operating Margin.

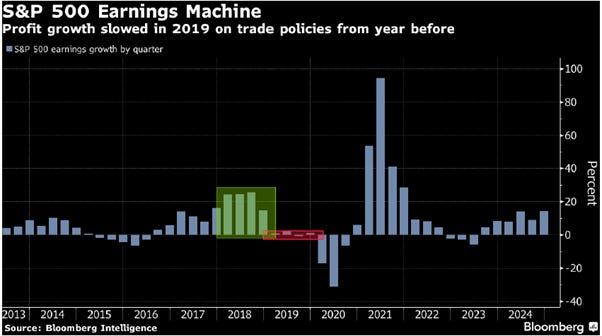

While Bessent and others who support tariff myths argue that tariffs lead to a one-time price adjustment, the reality is more damaging. Tariffs raise costs across the supply chain, starting with direct goods and cascading through industries that rely on those goods, like cars and construction materials. These cost increases continue as businesses pass them down to consumers, creating a wage-price spiral as workers demand higher wages to cope with rising costs. In this context, it should not be a surprise that Wall Street’s confidence in corporate profits is waning. Analysts have downgraded profit forecasts for S&P 500 companies for 22 of the last 23 weeks, marking the longest stretch since early 2023. As a result, concerns about the economic impact of Trump’s tariffs are weighing on stock prices, with the S&P 500 down ..% since its all-time high. This erosion of earnings expectations could further depress sentiment, as analysts lower their outlooks.

As the first-quarter earnings season begins on April 11 with reports from JPMorgan Chase & Co. and other banks, some US companies are already signaling trouble. Following Delta Air Lines Inc.'s drastic cut to its profit outlook due to weakening air travel demand, retailers like Kohl’s Corp., Abercrombie & Fitch Co., and Walmart Inc. have also raised concerns. While analysts project a 10% advance in S&P 500 earnings for 2025, down from 13% in early January, there may be further downside..

Despite resilient corporate results in recent years amid inflation and high interest rates, investors hope Trump will either soften or remove tariffs before they impact profits. It may take months for analysts and companies to adjust forecasts lower, as seen during Trump’s first term, when the trade war with China hurt profits about a year later. The economy had a tailwind from corporate tax cuts then, and pressure is mounting on Trump to push through a tax bill in his second term.

The only U.S. president who truly understood that free trade and mercantilism, combined with access to cheap and abundant energy, are the foundations of long-term prosperity was Ronald Reagan. In a 1987 radio address, he stated: ‘The way to prosperity for all nations is rejecting protectionist legislation and promoting fair and free competition. Now, there are sound historical reasons for this, but for those of us who lived through the Great Depression, the memory of the suffering it caused is deep and searing.’ As Reagan rightly pointed out, tariffs may seem patriotic at first, protecting American jobs and industries. But over time, domestic companies grow complacent, relying on protection instead of innovation. Worse, tariffs trigger retaliation, escalating into trade wars with rising costs and shrinking markets. Eventually, inefficiency and high prices drive consumers away, leading to business failures and job losses.

In a nutshell, investors are about to realize that when 'Trump Trades' meet 'Trump Tariffs,' 'Trumped Trades' fuel the shift of the US economy from Boom to Bust. As the ‘Trump Re-flation’ morphs into ‘Trump Stagflation, investors must focus on safeguarding their wealth by owning real assets like physical gold and silver, the only antifragile assets with no counterparty risk. Investors must also focus on Return OF Capital rather than Return on Capital, holding other commodities to weather the storm unleashed by the ‘Commodity Leviathan.’ Additionally, investors will actively manage their cash allocation using a portfolio of short-dated, investment-grade (IG) USD bonds with maturities under 12 months and Treasury bills (T-bills) with maturities not exceeding 3 months. These income-generating assets will provide stability. Among equities, investors should continue favoring low-leverage companies with strong EPS and FCF growth, prioritizing energy and commodity producers over consumers. By doing so, investors will ensure both peace of mind and wealth preservation.

WHAT’S ON THE AGENDA NEXT WEEK?

The last full week of the first quarter of the jubilee year will be a very quiet one for investors, who will only need to focus on the flash estimate of the US manufacturing and services indices, the release of the Core PCE index, and another set of consumer sentiment and inflation expectations from the University of Michigan. The week will also feature the final 18 S&P 500 companies releasing their earnings, with no major companies among them.

KEY TAKEWAYS.

As the first quarter of the Jubilee year comes to an end, the key takeaways are:

China's economy showed strong early growth in 2025, but weak consumption signals the need for sustained government action to Make China Great Again in a polarized global landscape.

The BOJ's reluctance to hike rates amid rising inflation and wages risks trapping Japan in a stagflationary doom loop.

US Retail sales showed a weak rebound in February, but slowing income growth, job insecurity, and looming tariff shocks signal deeper economic trouble ahead.

The FED held rates steady but confirmed that it is once again lost in the ‘Transitory, Tariff-Stoked Stagflation’.

In the 61 days since the 47th U.S. president took office, tariffs and DOGE have dominated financial headlines.

Tariffs create policy uncertainty, which reduce global trade and industrial production, while squeezing margins and weakening equity prices, as seen in 2018.

Trump's tariffs are pushing global trade away from the U.S while increasing FX volatility amidst geopolitical and economic uncertainty.

Trump's tariffs and financial sanctions fuel de-dollarization, disrupt global trade, and bolster gold reserves, all while undermining the dollar's reserve status by neglecting America's true economic strength, its innovation and productivity.

Trump's outdated economic strategies will ultimately shrink the U.S. economy, spark a global recession, and trigger what will be remembered as the ‘Trump Stagflation’.

Tariffs are eroding corporate profit forecasts and weakening investor confidence.

Gold and silver, the only antifragile assets without counterparty risk, have shown a strong historical correlation, making them equally vital shields against government overreach.

In such environment, investors will once again need to focus on the Return OF Capital rather than the Return ON Capital, as stagflation spreads.

Physical gold and silver remain THE ONLY reliable hedges against reckless and untrustworthy governments and bankers.

Gold and silver are eternal hedge against "collective stupidity" and government hegemony, both of which are abundant worldwide.

With continued decline in trust in public institutions, particularly in the Western world, investors are expected to move even more into assets with no counterparty risk which are non-confiscable, like physical Gold and Silver.

Long dated US Treasuries and Bonds are an ‘un-investable return-less' asset class which have also lost their rationale for being part of a diversified portfolio.

Unequivocally, the risky part of the portfolio has moved to fixed income and therefore rather than chasing long-dated government bonds, fixed income investors should focus on USD investment-grade US corporate bonds with a duration not longer than 12 months to manage their cash.

In this context, investors should also be prepared for much higher volatility as well as dull inflation-adjusted returns in the foreseeable future.

HOW TO TRADE IT?

The week of the Spring Equinox will be remembered as the first relief rally, as all major U.S. equity indices posted their first positive weekly performance after four consecutive weeks of declines. From a macroeconomic perspective, it marked the first time the economically and financially impotent Fed began to acknowledge that the U.S. is heading, slowly but surely, into an inflationary bust. The Magnificent 7 outperformed the Dow Jones, S&P 500, and Nasdaq 100. Despite the rebound, equity indices failed to close above their respective 200-day moving averages, which now serve as key resistance levels that must be broken to confirm that the recent market turmoil was merely a correction rather than the start of a bear market. Meanwhile, the 50% Fibonacci retracement levels on a one-year chart have provided support but will likely be retested in the next leg down. While stochastics and momentum indicators remain oversold on a one-year horizon, all four equity indices are still in a daily bearish reversal pattern. Greater stability in the coming days and weeks will be necessary to confirm a tradable bottom. As of March 21, all major U.S. indices remain in both daily and weekly bearish reversals, though stochastics indicate early signs of a bottoming process.

In this context, Energy and Financials outperformed, while Materials and Consumer Staples underperformed.

As of March 21st , 2025, the US remains in an inflationary boom, but with the S&P 500 to Gold ratio now below its year below its 7-year moving average for more than 2 months, an inflationary bust will materialize much sooner than Wall Street pundits and their parrots are eager to tell their clients. In this context, investors should stay calm, disciplined, and use market data tools to anticipate changes in the business cycle, rather than fall into the forward confusion and illusion spread by Wall Street.

When the 47th U.S. president was sworn in on January 20th, 2025, Wall Street and its media pundits encouraged YOLO investors to embark on supposed ‘Trump Trades,’ which involved buying the Nasdaq, Bitcoin, and the Magnificent 7, while ditching the Dow Jones, Gold, and the Energy sector. Two months later, the now misleadingly called ‘Trump Trades’ have turned into ‘Trumped Trades,’ as the assets that were supposed to make investors wealthy under the new era of Trumperialism have become losing bets.

Relative Performance of Nasdaq Index to Dow Jones Index (blue line); Bitcoin to Gold (red line); Magnificent 7 to S&P 500 Energy Index (green line) since January 20th, 2025.

Savvy investors who use past history and market data as a guide for anticipating the evolution of the business cycle know that tariffs are stagflationary, and that when 'Trump Trades' meet 'Trump Tariffs,' 'Trumped Trades' will accelerate the transition of the U.S. economy from the current inflationary boom into an inflationary bust, which will ultimately be remembered in the history books as ‘Trump Stagflation.’

Those same investors know that as the transition from an inflationary boom to a bust accelerates and monetary illusion deepens, the strategy remains to sell equity rallies, buy physical gold and silver on dips, and rotate within equities, reducing exposure to energy-consuming sectors (e.g., IT) while adding to energy-producing sectors (e.g., Oil & Gas) on pullbacks, as was the case in 2022 during the last inflationary bust of the U.S. economy. In this environment, investors must be increasingly selective, disciplined in taking profits, and diligent in setting stop losses around key technical levels as volatility rises.

Upper Panel: S&P 500 to Oil Ratio (blue line); 84-Months Moving Average of S&P 500 to Oil Ratio (red line); Second Panel: Gold to Bond Ratio (green light); 84-Months Moving Average of Gold to Bond Ratio (red line); Third Panel: 12-Months Rate of Return of S&P 500 Index (Orange Histogram); Lower Panel: 12-Months Rate of Return of Gold Price in USD (Yellow Histogram).

The impact of the Department of Government Efficiency (DOGE) on the U.S. economy will likely be positive in the long term, but in the short term, investors will remember that government spending, whether reckless or not, generates revenue for someone. As a result, investors will be cautious about holding the top 20 companies with the highest exposure to U.S. government revenue, as this income source could dwindle if additional austerity measures are implemented by the DOGE in chief.

If this research has inspired you to invest in gold and silver, consider GoldSilver.com to buy your physical gold:

https://goldsilver.com/?aff=TMB

Disclaimer

The content provided in this newsletter is for general information purposes only. No information, materials, services, and other content provided in this post constitute solicitation, recommendation, endorsement or any financial, investment, or other advice.

Seek independent professional consultation in the form of legal, financial, and fiscal advice before making any investment decisions.

Always perform your own due diligence.

Bravo!