Yields Mobilize Capital Allocation

Yields Mobilize Capital Allocation the way YMCA once mobilized a generation — they set the rhythm of power; if you want to know what’s next, follow the yield.

The Week That It Was…

In the third week of the second month, markets practiced selective productivity. Asia welcomed the Year of the Fire Horse with fireworks and closed exchanges—China shut for the week, while Hong Kong and Singapore observed shorter breaks. In the U.S., investors began with a long weekend for Washington’s Birthday, before turning their attention to the FOMC Minutes, Industrial Production, and the Trade Balance, alongside earnings releases from 53 S&P 500 companies. Rather than attempting to absorb everything, focussed on a select group—Devon, Palo Alto Networks, Occidental, Texas Pacific Land, Deere, and Walmart—where the signal proved stronger than the noise.

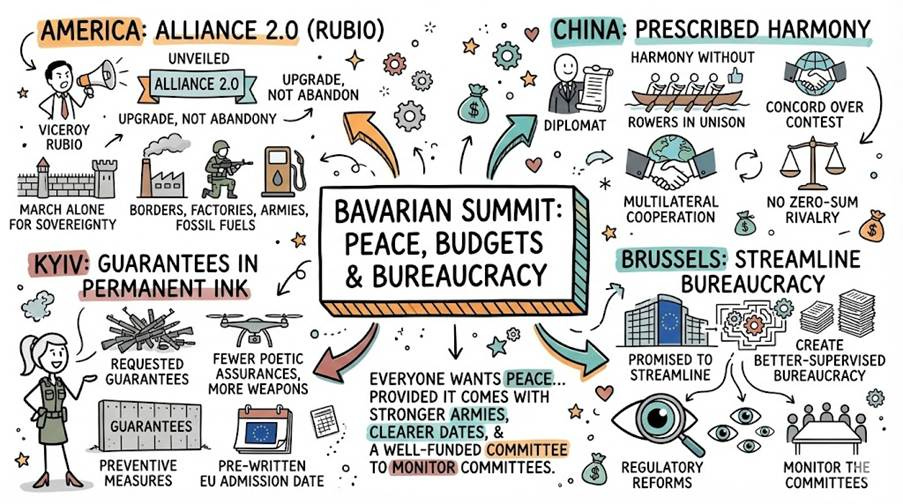

On the day celebrating love, high in the Bavarian mountains—where history once demonstrated how “civilizational renewal” can go spectacularly wrong—Viceroy Rubio assured Europe that Washington was not abandoning the transatlantic alliance of the North Atlantic Terror Organization alias NATO, merely upgrading it to Alliance 2.0: borders reinforced, factories relit, armies funded, and climate heresies gently corrected. The message was equal parts Valentine and warning—America prefers to march together but is fully prepared to march alone in the name of sovereignty, industrial resurrection, and strategic clarity. The post–Cold War dream of borderless harmony was reclassified as a “dangerous delusion,” free trade became a cautionary tale, and migration a test of civilizational resolve.

In the official script, this was not a retreat from globalism but a restoration of destiny: a reinvigorated West, proudly self-reliant, tightly bordered, energetically fossil-fuelled, and united—of course—by the shared understanding that history has not ended, it has simply been reassigned for corrective editing.

After Viceroy Rubio spoke of Western resolve, China’s chief diplomat responded in the measured cadence of Confucian thought. He reminded his audience that true strength lies not in superiority but in harmony without uniformity. Nations, he suggested, should honour sovereignty, cultivate multilateral cooperation, and seek concord over contest. Global challenges, like turbulent waters, require steady hands rowing in unison rather than vessels colliding in pride. Presenting China as a patient steward of dialogue and inclusive governance—particularly in partnership with Europe—he cautioned against the temptations of militarism and zero-sum rivalry in the Asia-Pacific.

In the Confucian view, lasting peace is not secured through dominance, but through balance, restraint, and the shared guardianship of a common future.

And to conclude a full day of love and hate speeches highlighting insecurity rather than security from impeccably educated European strategists explaining why peace requires just one more “temporary” emergency and a slightly larger line of credit, the high-heeled headliner from Kyiv took the stage. His message was simple: fewer poetic assurances, more actual weapons; fewer summit selfies, more security guarantees carved in stone. NATO, we were reminded, must grow stronger, Europe must spend closer to 5% of GDP on defence, and “preventive measures” should ideally occur before tanks cross borders—an innovative concept in hindsight diplomacy. The analogy was clear: if the roof is leaking, don’t just rearrange the furniture—fix the roof, preferably with reinforced concrete and a drone squadron. Intent matters, anchorage is missing, drones are the new cavalry, and GDP is apparently the moral yardstick of commitment.

And in a final flourish worthy of the Ministry of Inevitable Integration, he requested that Ukraine’s admission date into the Brussels-based Union be pre-written into history—because nothing says sovereign process like pencilling in destiny ahead of time.

On Day 2 of the Bavarian War & Wellness Summit, High Priestess Kalas of Eurostan took the podium to remind the continent that peace, like bureaucracy, requires structure. The central question: not whether Ukraine joins the EU—but precisely when destiny will be timestamped in triplicate. Panellists solemnly agreed that Europe must become a “credible negotiating partner,” which in official dialect means building a stronger committee to supervise the other committees. There were calls for a “coalition of the willing” (membership subject to moral enthusiasm), reflections on Europe’s strengths and weaknesses (mostly procedural), and renewed ambition to streamline decision-making—by possibly creating additional institutions to simplify the existing ones. The concept of a “two-speed Europe” was floated, reassuring everyone that integration will proceed efficiently—just at different velocities, depending on who’s pedalling.

In summary: unity through complexity, strength through structure, and progress through ever more impressive acronyms.

After High Priestess Kalas completed her daily briefing on the Ever-Expanding Russian Bogeyman, the Central Banker-in-Chief of Eurostan joined a panel to bravely confront Europe’s greatest enemy: its own paperwork. The experts agreed that innovation is being lovingly strangled by a regulatory jungle so dense even entrepreneurs need a permit to find the exit. The solution, naturally, is to streamline the rules by empowering more institutions to supervise fewer processes more efficiently and raise more taxes of course—while somehow discussing globalism, French cheese, and European onions as strategic assets. The conclusion? Innovation is like a garden: too much bureaucratic watering drowns it—but rest assured, a new task force will soon be formed to measure the humidity.

In a nutshell, at the Bavarian War & Wellness Summit, America promised to lead, China offered harmony, the Dancer on High Heels from Kyiv demanded weapons, and Europe formed a committee to discuss forming a committee — history, it seems, is being corrected one acronym at a time.

In the ever-innovative fiscal laboratory of the Netherlands, lawmakers have decided that if your investments think about making money, the taxman would like his 36% cut. Starting January 1, 2028, the new “Actual Return” regime won’t just tax income you’ve received — it’ll also tax the paper gains on your stocks, bonds, crypto, and presumably your tulip bulbs, whether you’ve sold them or not. Nothing says “cash flow management” like getting a bill for profits that exist only on a spreadsheet. So, if inflation pushes up the value of your house, congratulations — you’re richer! Please remit 36% of that theoretical windfall in actual cash. Don’t have the cash? Well, perhaps you didn’t need that house anyway. Sell first, live somewhere later.

The old system was ruled unconstitutional, so naturally the solution is something… bolder. With tax disparities widening across Europe, capital may start packing its bags faster than tourists fleeing bad weather. At this rate, “Sell in May and go away” could become “Sell in Europe and relocate.” Bold strategy — let’s see how it plays out.

On the other side of the pond, chatting with reporters aboard Air Force One after a well-earned Presidents’ Day weekend at his resort, The Manipulator-In-Chief casually revealed he’s discussing future arms sales to Taiwan with the Mandarin Xi—because nothing says light holiday banter like missile packages. He promised a decision “pretty soon,” just ahead of an April summit, while reports from the ‘Fake Times’ swirl of another multibillion-dollar defence deal on top of the existing $11 billion tab. Meanwhile, Washington and Taipei quietly sealed a new trade agreement, proving that in modern diplomacy, you can expand commerce, boost energy flows, and negotiate weapons—all in the same frequent-flyer cycle.

Based on a report from the Wall Street Journal — an outlet whose credibility varies depending on which administration is in power — Taiwan’s $11.1 billion arms package, featuring Patriot missile interceptors and other assorted tools of self-defence, is currently gathering dust in Washington’s in-tray. Apparently, Emperor Xi expressed his displeasure and someone in the Donald Copperfield’s administration quietly concluded that a presidential visit to Beijing was worth more than a formal security commitment to an inconvenient ally — and considerably less likely to ignite another banker-approved Forever War in the Pacific. The WSJ helpfully assures readers that ‘The Warmonger in Chief’ “wouldn’t be pushed around by China,” which is a remarkably creative way of describing an administration carefully timing an arms sale to avoid upsetting the very man it just promised not to upset. In exchange for this geopolitical agility, China is generously considering purchasing an additional 8 million metric tons of soybeans — because nothing captures the grandeur of great power diplomacy quite like trading missile defence systems for agricultural commodities.

Fresh from his signing ceremony in Davos — where the world’s most dedicated globalists gather annually to discuss the common people’s problems from the comfort of a Swiss ski resort — ‘The Manipulator In Chief’ convened the Board of Peace for its first board meeting in Washington, an institution whose relationship with actual peace is best described as complicated. As in Munich, the agenda conspicuously avoided the word “peace” in any operational sense, focusing instead on the more pressing question of precisely how many days remain before the Middle East is once again democratized at gunpoint. The answer, delivered with the casual confidence of a man who has done this before: 10 to 15 days. Because nothing says “spreading democracy” quite like another carefully orchestrated regime change, brought to you by the same Washington establishment that has been spreading democracy across the Middle East for the past three decades only to promote the Zionist American Imperialistic agenda.

While the Board of Peace convened to discuss its next democratic intervention, Persia has been quietly attending to its homework. The Islamic Republic now fields an arsenal of supersonic and reportedly hypersonic missiles — courtesy in part of Beijing’s characteristically subtle military technology transfers — and has made the USS Abraham Lincoln the star of its threat communications, vowing to “sink and humble” the carrier strike group currently deployed in the region. Whether Iran can actually sink a supercarrier is debatable; these vessels are engineered to absorb punishment that would obliterate lesser ships. However, that may be entirely beside the point. A single successful strike — not a sinking, merely a visible hit on the world’s most iconic symbol of American military supremacy — would deliver a psychological blow of historic proportions.

Washington, whose institutional memory rarely extends beyond the last news cycle, would do well to recall that when the Persians captured Emperor Valerian in 260 AD, it was not the capture itself that unravelled Rome — it was what it signalled to every barbarian watching from the periphery. The greatest danger here is not a sunken carrier. It is the irreversible erosion of the image of American invincibility — an asset that, once lost, does not appear on any defence budget.

https://greekreporter.com/2026/01/02/roman-emperor-valerian-captured-rome-greatest-humiliation/

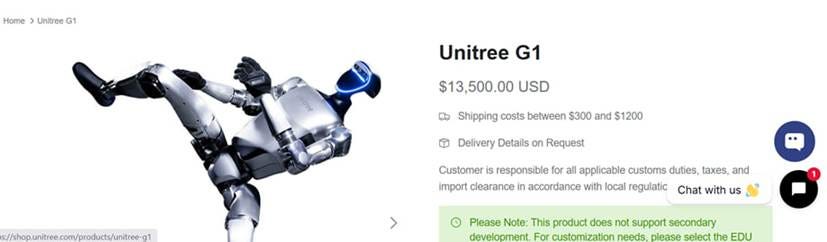

At China’s Lunar New Year Gala, while many admired the fireworks, the wise observed something deeper: robots performing kung fu with balance, rhythm, and discipline worthy of a Shaolin novice. Ancient tradition met algorithmic precision, and this year the machines did not wobble—they flowed. In the span of a single year, their movements grew smoother, their formations tighter, their balance almost graceful. Such is the way of compounding: when models learn, hardware steadies, and iteration quickens, progress arrives not step by step, but stride by stride.

Most curious of all, one may purchase such a mechanical disciple today for the price of a modest sedan,

https://shop.unitree.com/products/unitree-g1

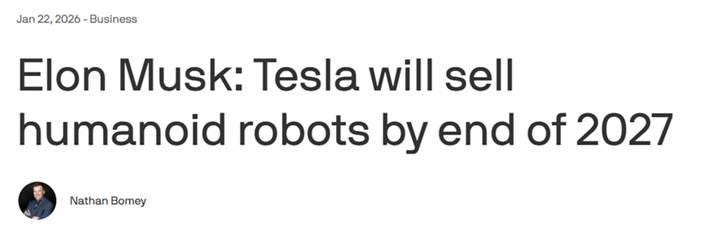

while, in America, others still promise enlightenment “in two more years.”

https://www.axios.com/2026/01/22/elon-musk-tesla-optimus-robots

In this arena, some build, others brand; some ship, others capitalize. As Confucius might gently note : it is better to perfect one’s stance than to perfect one’s valuation. The future, it seems, practices daily—and it practices very fast.

Having warmed the hearts of millions with their delightful Lunar New Year robot dance show — nothing says “family entertainment” quite like armed autonomous platforms — China’s People’s Liberation Army has wasted little time revealing what the real agenda was all along. The PLA has unveiled a motion-mimicking combat robot that replicates a soldier’s every move in real time, powered by AI and a motion-sensing suit, in what military strategists are calling “intelligent warfare” and what everyone else is calling “a Terminator” The system — affectionately compared to the robots in Real Steel, because nothing reassures foreign dignitaries quite like a Hollywood blockbuster reference — was demonstrated, presumably to ensure that the message was received loud and clear in every time zone. China’s “intelligent warfare” strategy is progressing smoothly: first, dazzle the public with dancing robots; then, show the generals the ones that don’t dance.

And lest anyone mistake the Lunar New Year performance for mere showmanship, the reality on the ground is rather more sobering. China has already deployed humanoid robots — specifically the Walker S2 by UBTech Robotics — along its border with Vietnam, where they autonomously patrol, conduct surveillance, and helpfully guide travellers who presumably had no say in the matter. Capable of autonomous navigation and self-sufficient enough to replace their own batteries — because even robots cannot rely on human punctuality — these mechanical border guards are part of a 264-million-yuan ($37 million) contract for border monitoring. In other words, while the world was busy debating whether AI would take white-collar jobs, China quietly handed the graveyard shift at the border to a robot that never sleeps, never complains, and never applies for a pay rise.

https://www.eldiario24.com/en/china-deploys-advanced-border-robots/26270/

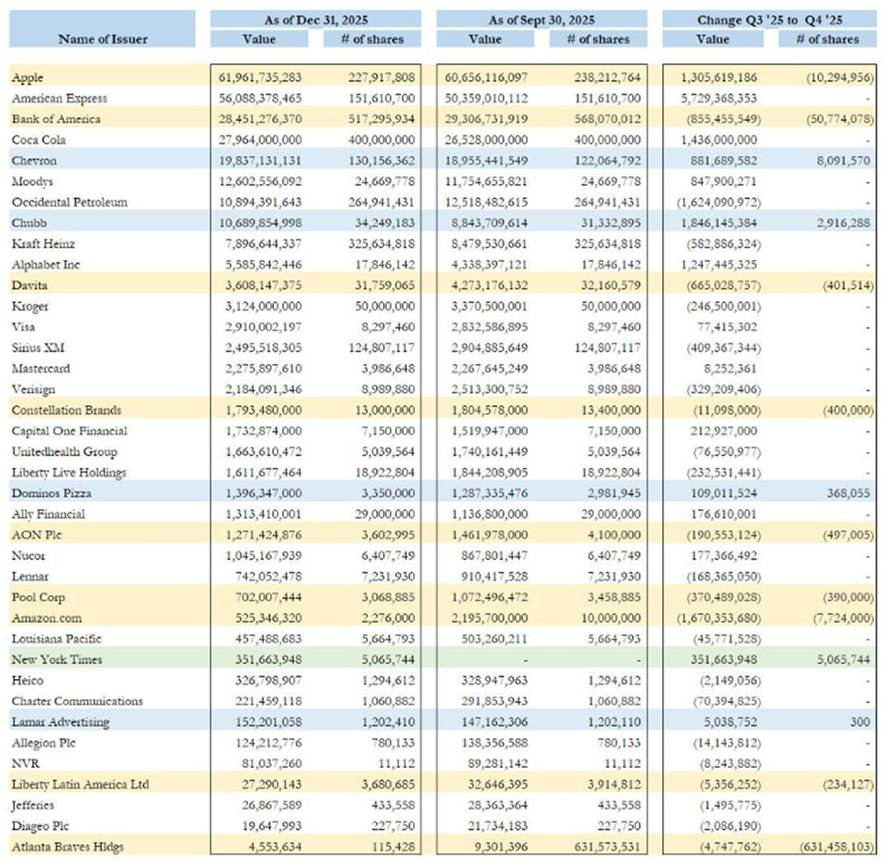

In what may be Warren Buffett’s final act as CEO of Berkshire Hathaway, the Oracle of Omaha — or whichever wise sage now holds the stock-picking brush — continued trimming the garden with purpose. Amazon was cut by a striking 77%, reduced from 10 million shares to a modest 2.28 million, suggesting that six years of wisdom eventually replaced six years of enthusiasm. Apple and Bank of America, long cherished like family heirlooms, were also quietly reduced by 4.3% and 8.9% respectively, continuing a pruning exercise begun in 2024. In their place, modest additions to Chevron and Chubb, and a small, almost philosophical new position in the New York Times — as if to ensure Berkshire remains informed of its own obituaries.

https://www.sec.gov/Archives/edgar/data/1067983/000119312526054580/xslForm13F_X02/50240.xml

As Confucius never quite said but surely meant: ‘The superior investor does not cling to yesterday’s wisdom, for even the finest tree must shed its leaves to survive the winter‘.

As financial history books may one day record, Blue Owl Capital is auditioning for the role that New Century Financial played in the subprime debacle — the canary in the private credit coal mine. Having previously allowed a generous 17% quarterly redemption rate — itself a flashing warning sign — the private credit giant has now done what all gated funds eventually do when the cockroaches multiply: slammed the door entirely. Investors in OBDC II will no longer be able to redeem shares quarterly; instead, they will receive their money back through “periodic distributions” — which is financial industry speak for “whenever we manage to sell something.” To demonstrate its portfolio’s magnificent quality, Blue Owl sold $1.4 billion in loans at 99.7 cents on the dollar — a transaction co-founder Craig Packer heroically described as “putting our money where our mouth is,” apparently unaware that selling assets under duress at a haircut is traditionally not considered a flex. The buyers, reassuringly, included North American pension funds and insurance companies — meaning that retail investors fleeing a sinking ship have successfully passed the lifejacket to retirees. The canary, it appears, is not singing.

In a ruling that Confucius would have appreciated for its elegant confirmation of the obvious, the American Supreme Court has determined that a law authorizing the president to “regulate, direct, and compel” importation does not — in fact — authorize him to impose tariffs, because nowhere in the text does the word “tariff” appear. The administration, which had collected nearly $99 billion in tariff revenue this fiscal year alone, argued that regulating imports during a national emergency implicitly includes taxing them — a creative interpretation that multiple courts found unconstitutional and the Supreme Court ultimately declined to rescue.

https://www.supremecourt.gov/DocketPDF/24/24-1287/363533/20250618160616885_24-1287response.pdf

As for ‘Tariff Man’ — the Master would remind us that the wise ruler does not mourn a door that closes, for other doors remain open: tariff authority under alternative statutes survives intact, and the great tariff framework shall endure, merely wearing different legal clothing. Donald Copperfield, never one to accept a legal setback gracefully, announced plans to impose a new 10% global tariff under alternative authority within approximately fifteen minutes of the ruling — suggesting the administration had packed a spare set of tariffs just in case.

https://truthsocial.com/@realDonaldTrump/posts/116104407604484915

The bond market received that ruling with all the enthusiasm of a surprise tax audit, the Supreme Court’s decision to strike down President’s sweeping tariffs sent 30-year Treasury yields up 6 basis points to 4.75% and the dollar promptly lower — because eliminating $1 trillion in projected revenue from an already $1.8 trillion deficit tends to concentrate minds. The irony, of course, is exquisite: the tariffs that were supposedly strangling the economy were also quietly keeping the deficit from becoming even more catastrophic. ‘Uncle Scrooge Bessent’ assured markets that revenue would remain “virtually unchanged,” while analysts quietly noted that $170 billion in collected tariffs may need to be refunded and short-term T-bill issuance will likely surge to plug the gap. As Confucius might observe: “The ruler who loses one tariff simply finds another — but the bond market, unlike the Supreme Court, keeps score.”

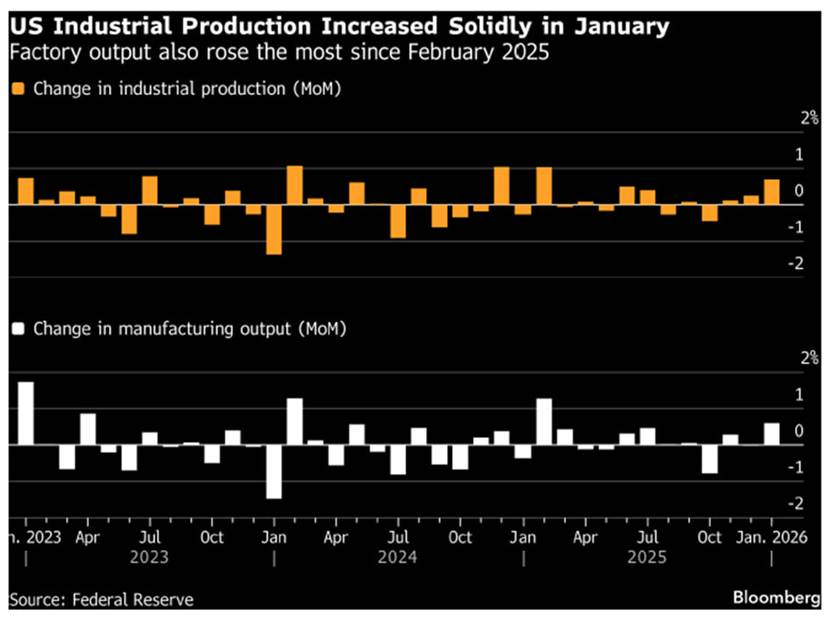

In what may be the first tangible evidence that “Make America Industrial Again“ is more than a bumper sticker, US industrial production surged 0.7% in January — the biggest monthly gain in nearly a year. Manufacturing, which accounts for three-quarters of total industrial production, led the charge with a 0.6% advance, driven by broad-based gains in business equipment, consumer goods, computers, machinery, and motor vehicles. Even the durable goods order book joined the party, with December bookings surprising to the upside across communications equipment, metals, and electrical machinery. Factory employment rose in January for the first time since late 2024, ISM manufacturing hit its strongest reading since 2022, and capacity utilization climbed to 75.6% — the highest since September. Utilities added 2.1% courtesy of Arctic air masses that apparently forgot the Deep South was not prepared.

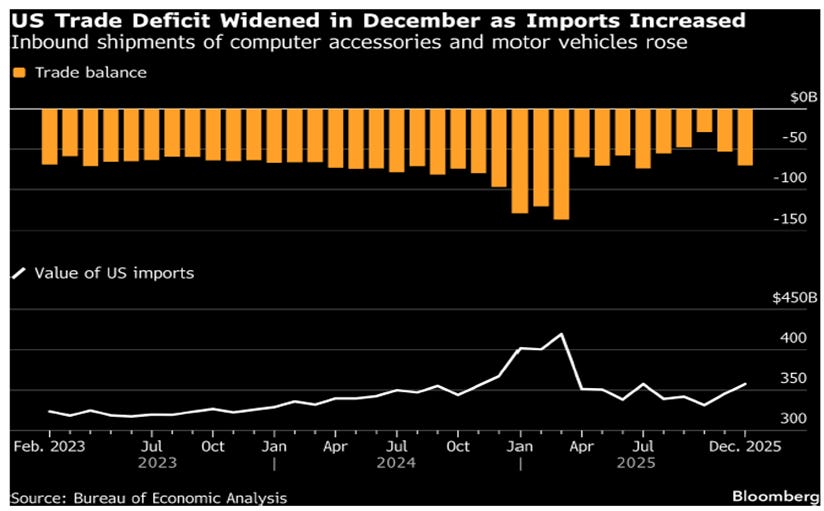

After a year of breathless tariff announcements, emergency declarations, and policy pivots, the US trade deficit for 2025 clocked in at a record $901.5 billion — virtually unchanged from before the entire circus began. December alone contributed a $70.3 billion shortfall, wider than almost every economist predicted, as imports rose and exports fell. In summary: maximum disruption, minimum results. The tariff strategy designed to resurrect American manufacturing has so far succeeded mainly in making trade data more volatile and economists more employed. The Supreme Court may yet rule on whether any of this was even legal — a detail the administration apparently considered optional.

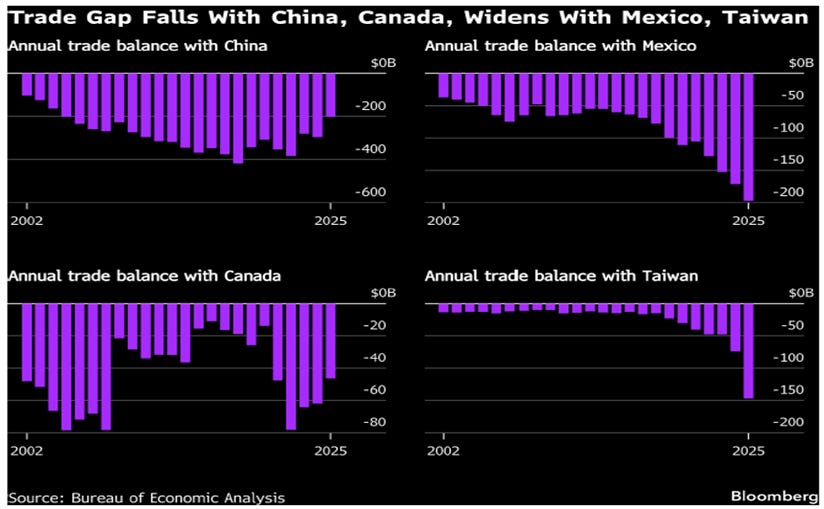

In what can only be described as the world’s most expensive game of trade Whac-A-Mole, the US deficit with China did indeed narrow to $202 billion — the smallest in over two decades — as tariffs successfully redirected Chinese exports through Mexico and Vietnam, where deficits promptly swelled to record highs. Taiwan, meanwhile, nearly doubled its surplus with the US to a record $146.8 billion, cheerfully exempt from tariffs while flooding America with the semiconductors needed to power the AI boom.

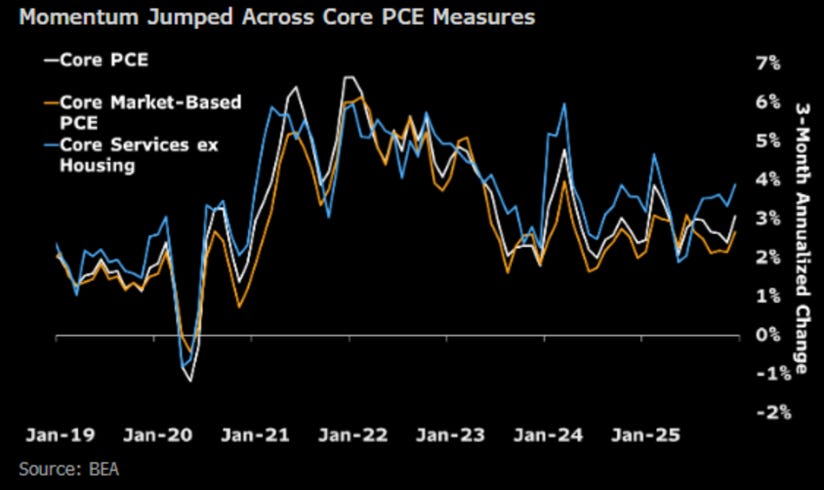

Like a Swiss clock that has quietly lost its mind, the Fed’s favourite inflation gauge refused to cooperate in December. Core PCE rose 0.4% MoM — hotter than the expected 0.3% — pushing the YoY reading to 3.0%, the highest since April 2025 and comfortably above the Fed’s 2% target, which at this point is less a policy objective and more a fond memory. Headline PCE matched the heat at 0.4% MoM, lifting the annual reading to 2.9% — the highest since March 2024. SuperCore PCE, that most stubborn of inflation measures, printed +3.3% YoY, having barely moved in a year, suggesting that services inflation has no intention of going anywhere.

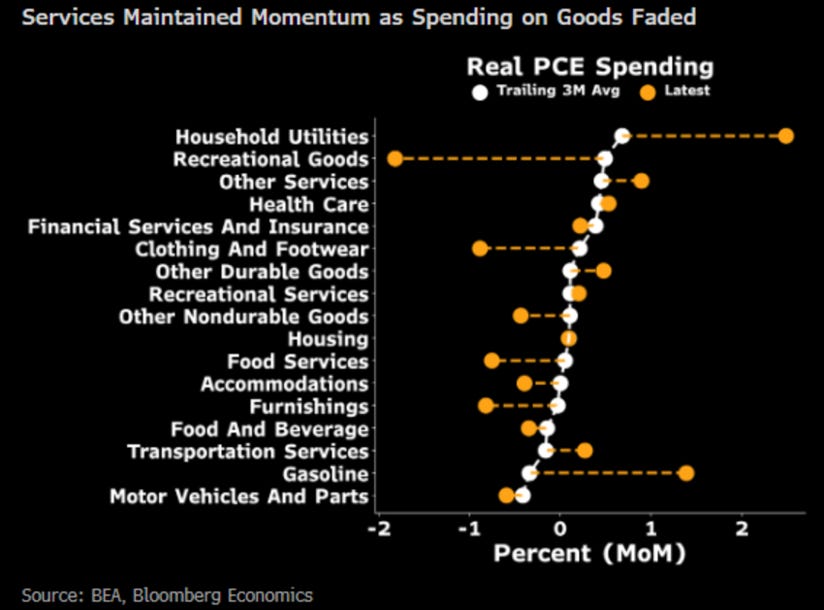

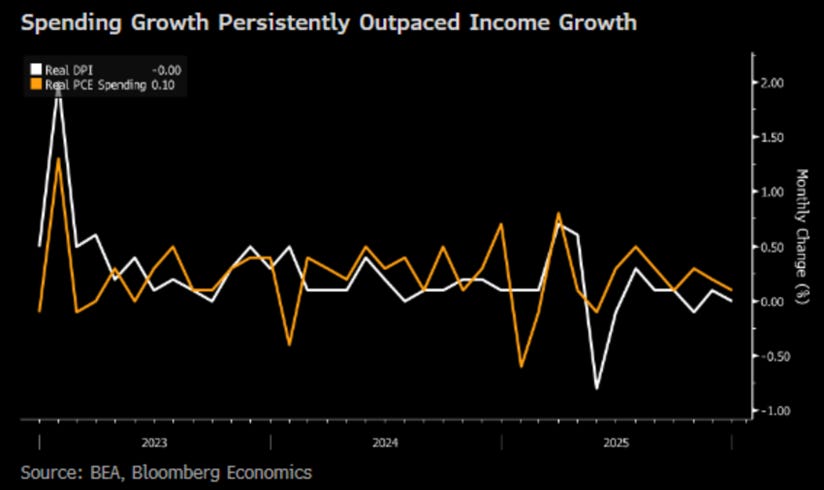

Beneath the headline surprise, the consumer is quietly reshaping spending habits in ways that tell a more nuanced story. Real goods spending contracted 0.5%, with tariff-exposed categories leading the retreat — recreational goods down 1.8%, clothing off 0.9%, and furnishings declining 0.8%, suggesting that consumers are already voting with their wallets against imported discretionary items. Services picked up the slack, accelerating to 0.3% from November’s tepid 0.1%, driven by healthcare and a remarkable 2.5% jump in household utilities — apparently Americans are prioritising staying warm over staying fashionable. The soft spot was food services and accommodations, which contracted 0.7%, hinting that even the dinner-out habit is beginning to fray.

The income picture is less encouraging than the headline suggests. Personal income grew 0.3% in December, but nearly half of that increase came from transfer payments rather than earned wages — with employee compensation accounting for only a third of aggregate income growth. More troubling is the savings rate, which fell to 3.6% — the lowest since late 2022 — as spending persistently outpaced income throughout the second half of 2025. Unlike the post-pandemic period, consumers can no longer draw on excess savings to bridge the gap, and with labour demand softening, the spending outlook is increasingly dependent on an improvement in the jobs market that is far from guaranteed.

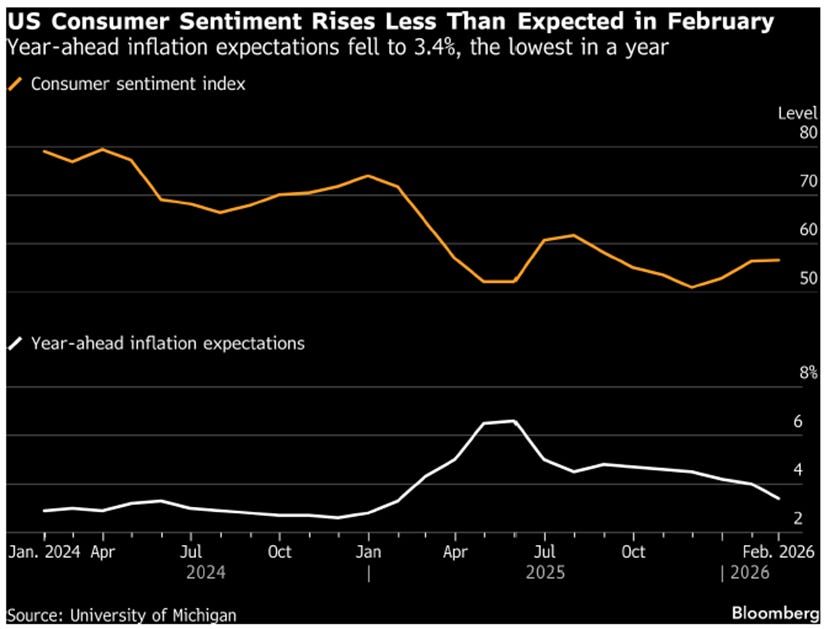

While ‘Tariff Man’ raided the constitutional lost-and-found for a replacement trade weapon, American consumers delivered a sentiment reading so underwhelming it barely registered a pulse — 56.6 in February, up from 56.4 in January, missing even the modest estimate of 57.3. The K-shaped economy remains on full display: wealthier Americans cheered their stock portfolios while the 46% who told surveyors that high prices are actively destroying their finances remained decidedly less festive. One-year inflation expectations fell to 3.4% — encouraging, until one remembers that ‘Tariff Man’ announced a replacement tariff approximately fifteen minutes after the Supreme Court struck down the last ones.

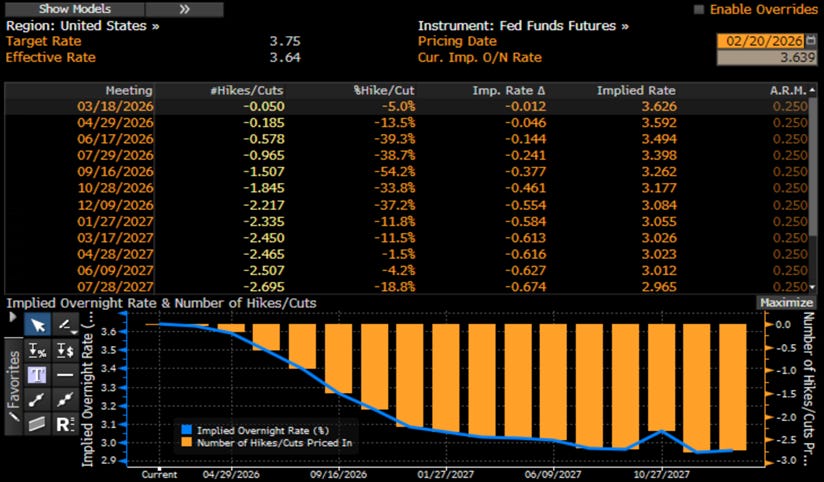

In the ancient ritual of reading the Federal Reserve’s tea leaves, the January FOMC minutes revealed what the wise man already suspected: the committee is in no hurry to do anything. The decision to hold rates was nearly unanimous, with only Governors Miran and Waller — the committee’s two impatient disciples — still clamouring for cuts. More striking was the revelation that “several” participants would have welcomed two-sided language, leaving open the possibility of rate hikes should inflation refuse to behave — a subtle reminder that the door to tightening has not been entirely forgotten. The inflation optimists pointed to productivity and deregulation as disinflationary forces, while the cautious majority warned that progress would be slow and uneven, and that tariffs may yet add to the price of things. As for the labour market, the “vast majority” declared it stable, though “most” still worried it could deteriorate — a distinction that would impress even Confucius in its carefully crafted ambiguity.

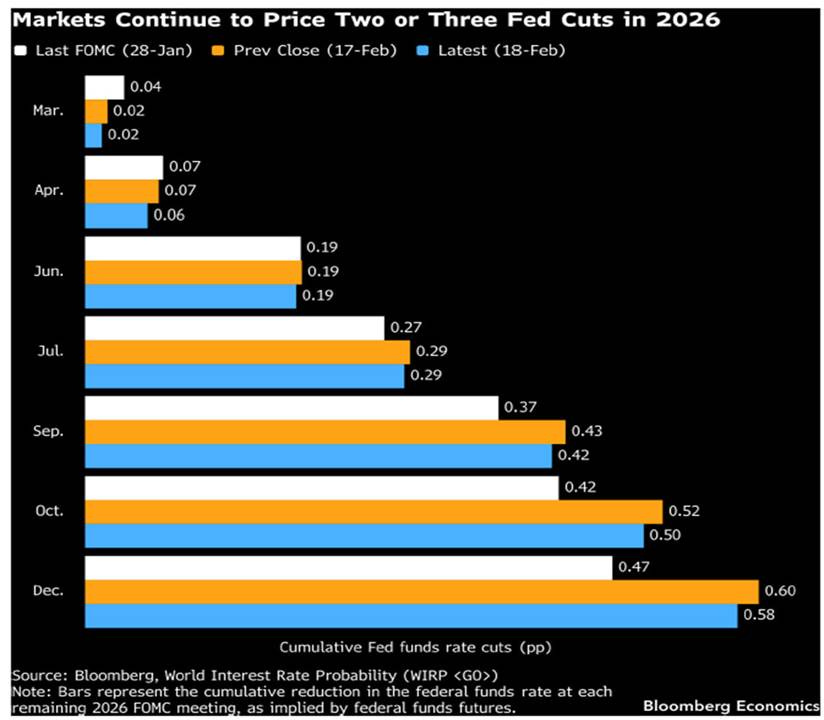

As the Manipulator-in-Chief dusts off the usual foreign bogeymen and tariffs as weapons of mass distraction from the investable reality that the US economy is drifting toward its next inflationary hangover — soon to be neatly rebranded by headline artists as “Trump Stagflation,” as if business cycles were a campaign slogan — Wall Street’s finest are still lining up at the “independent-in-name-only” Fed’s drive-through window, still confidently pricing in at least two rate cuts before year-end. Reality, however, isn’t playing along. It’s the same old screenplay: inflate the boom, stumble into the bust. Buckle up — the Fed seems to have misplaced the controls, the bond market has commandeered the cockpit, and credibility was last seen parachuting somewhere over the Persian Gulf.

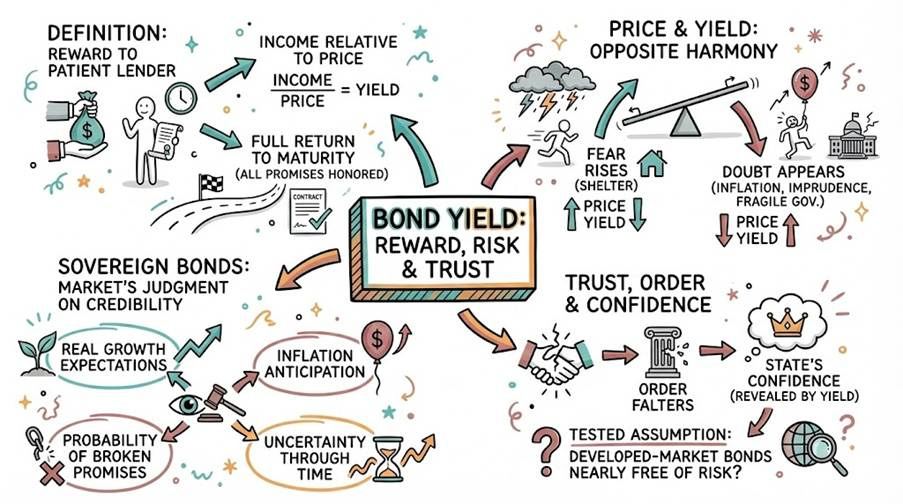

There was a time when bond yields were regarded as modest and unremarkable — like a quiet scholar in the corner of the court, speaking little and disturbing no one. They moved with patience, observed by pension funds and insurance stewards, rarely stirring passion or alarm. Today, that same quiet scholar has been summoned to the centre of the kingdom. Bond yields now reflect the ambitions of empires, the excess of treasuries, the tremors of war, and the fading confidence in sovereign virtue. What once seemed technical has become profoundly political. To understand the movement of capital, the fluctuations of currencies, and the wisdom of portfolio construction, one must first contemplate bond yields. They are not mere numbers assigned to debt. They measure the value of time, the discipline of rulers, the expectations of inflation, and the credibility of governance. As Confucius taught, when trust is lost, the state cannot stand. Bond yields are simply the market’s way of asking whether trust still remains.

A bond yield is the reward granted to the patient lender who entrusts his capital to another. In simple appearance, it is the income received relative to the price paid; yet in truth, it is better understood as the full return earned if the bond is held faithfully to its maturity and all promises are honoured. Price and yield move in opposite harmony: when fear rises and investors seek shelter, bond prices ascend and yields bow; when doubt appears — whether from inflation, imprudence, or fragile governance — prices retreat and yields rise in quiet protest. Thus, yield is not merely arithmetic; it is the market’s judgment on credibility. In the case of sovereign bonds, it reflects expectations of real growth, the anticipation of inflation, the uncertainty carried through time, and the probability that promises may not be fully kept. As the Master taught, when trust weakens, order falters; bond yields simply reveal whether the state still commands confidence.

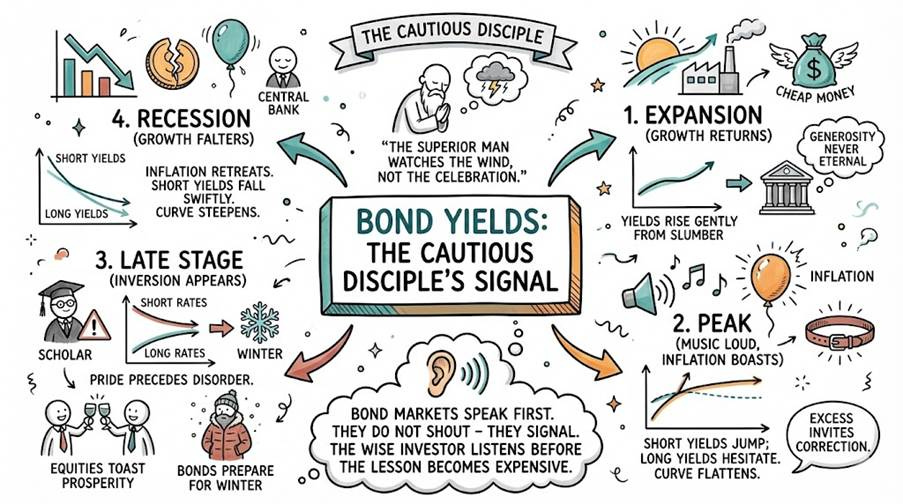

Bond yields are like the cautious disciple in the village — the one who bows politely, observes quietly, and then announces the storm before the sky darkens. As Confucius might say, the superior man watches the wind, not the celebration.

In Expansion, growth returns and money remains cheap. Yields rise gently from their slumber, reminding everyone that generosity from central banks is never eternal. In Peak, the music grows loud, inflation boasts, and policymakers tighten with sudden virtue. Short-term yields jump; long-term yields hesitate. The curve flattens, whispering that excess invites correction.

At the late stage, inversion appears — short rates above long rates — like a scholar warning that pride precedes disorder. Equities toast prosperity; bonds quietly prepare for winter. Then comes Recession: growth falters, inflation retreats, and central banks rediscover humility. Short yields fall swiftly, long yields follow with measured caution, and the curve steepens once more.

Thus, through all seasons, bond markets speak first. They do not shout — they signal. The wise investor listens before the lesson becomes expensive.

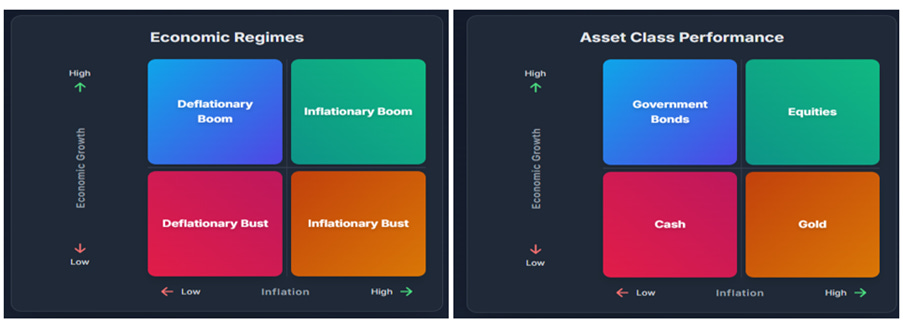

In the great wheel of the Joseph Schumpeter cycle, the four assets of the Permanent Portfolio behave like disciplined students responding to the seasons of excess and regret. During the inflationary boom, when optimism grows louder than wisdom, equities feast and gold smiles knowingly, while bonds begin to sweat and cash waits patiently at the door. In the inflationary bust, when prices still rise but growth falters, gold stands tall like the cautious elder, bonds complain about lost purchasing power, and equities discover humility. In the deflationary bust, when credit contracts and ambition dissolves, bonds regain honour as yields fall, cash becomes unexpectedly powerful, and equities seek forgiveness. Finally, in the quiet deflationary recovery, cash deploys, equities rebuild, bonds stabilize, and gold rests — neither triumphant nor ashamed. As the Master might observe: when the cycle turns, each asset has its moment of virtue; the wise investor does not ask which one is best, but which season is approaching.

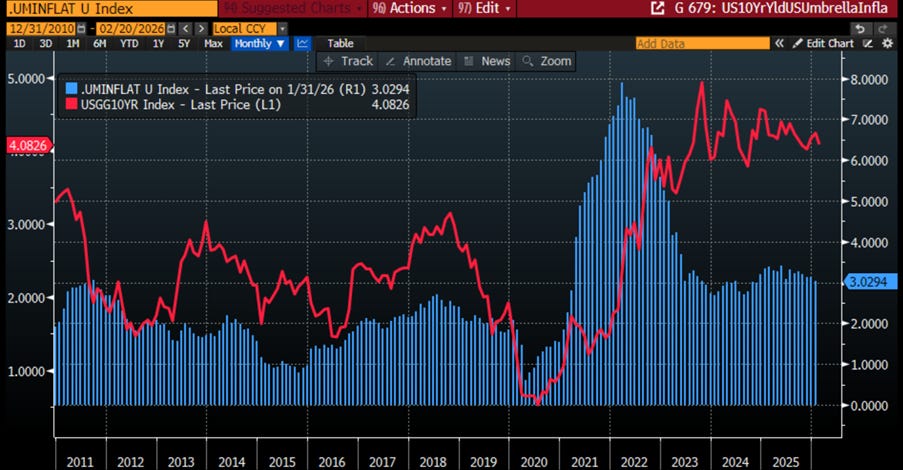

A bond is basically a polite contract that says, “I promise to pay you the same amount no matter what happens.” Inflation hears that and laughs. When CPI starts climbing unexpectedly, the fixed payments of a bond suddenly feel like being paid in shrinking coins. Naturally, bond yields respond by stretching upward — like an investor saying, “If my money is losing weight, I demand heavier compensation.” CPI and bond yields are therefore reluctant dance partners. When CPI twirls higher, yields follow, sometimes gracefully, sometimes stomping across the floor. Markets bake inflation expectations into yields through breakevens, real yields, and that mysterious creature called the term premium — which is just a fancy way of charging extra when the future looks messy. As long as inflation behaves and policymakers look responsible, yields stay calm. But when CPI becomes dramatic and deficits resemble a buffet with no closing time, yields don’t whisper — they spike. Bonds may be fixed income, but their patience with inflation is anything but fixed.

US Umbrella Inflation Index (histogram); US 10-Year Yield (red line).

The term premium is the bond market’s way of saying, “I’ll lend to you for ten years… but I’ll need a little something extra for the emotional stress.” It’s the bonus investors demand for locking up money in a future that may include surprise inflation, ambitious politicians, or creative accounting. When CPI behaves nicely and inflation stays predictable, the term premium relaxes — the future looks boring, and boring is beautiful. But when CPI starts jumping around like it had too much espresso, investors widen their eyes and their required compensation.

US CPI YoY Change (blue line); US 10-Year Yield (red line); US Term Premium on a 10-Year Zero Coupon Bond (green line).